Medical Gloves Market Summary

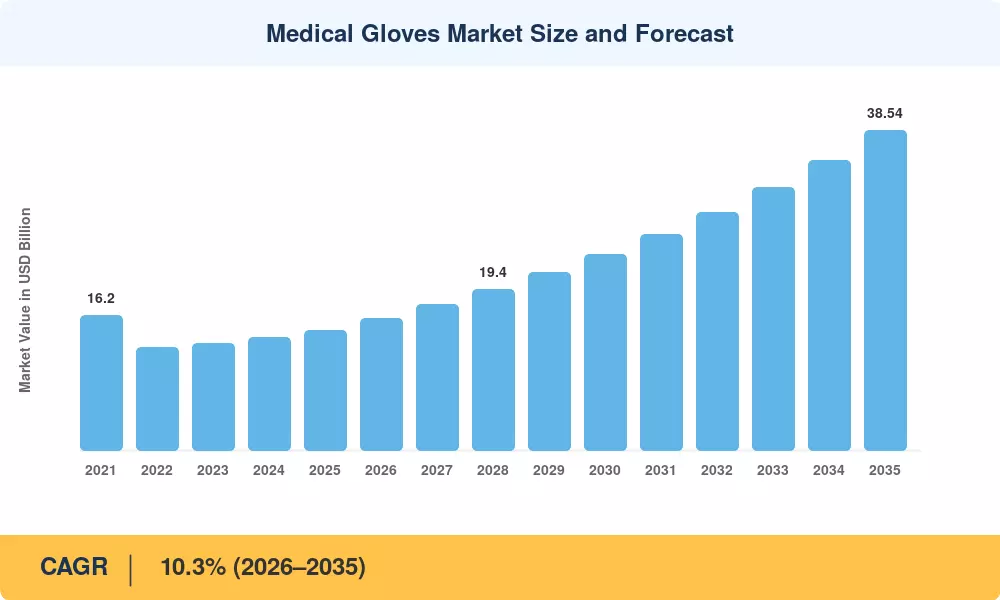

The Global Medical Gloves Market size was valued at USD 14.46 Billion in 2025, and the market is projected to grow from USD 15.95 Billion in 2026 to USD 38.54 Billion by 2035, registering a CAGR of 10.3% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the World Health Organization's updated hand hygiene guidelines, which now mandate single-use glove changes between every patient touchpoint, and hospital procurement budgets that have nearly doubled their personal protective equipment line items since 2020 [1]. Together, these structural forces convert what was once a commoditized consumable into a strategic supply-chain priority for health systems worldwide.

The market for medical gloves is fundamentally changing due to material science. Modern nitrile and neoprene compounds, which reduce the danger of latex-protein allergies and increase puncture resistance, are gradually displacing legacy natural-rubber formulas that dominated procurement lists for decades. In an effort to lessen reliance on imports from Southeast Asia, European Union governments funded an estimated USD 340 million in domestic glove manufacturing incentives between 2023 and 2025 [2]. Even as material criteria become more stringent, automated high-speed dipping lines can now make up to 45,000 gloves per hour, reducing unit costs.

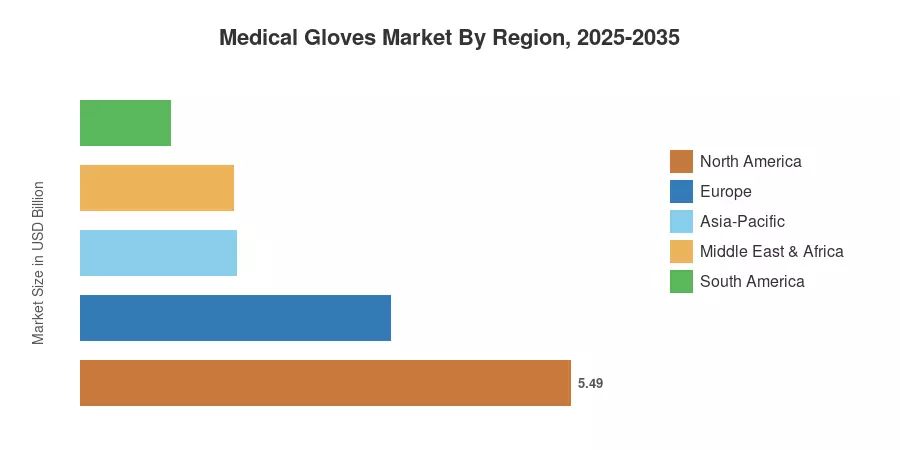

Due to strict FDA device-listing regulations and high per-capita healthcare spending, North America holds around 38% of the medical gloves market. The fastest-growing region is Asia-Pacific, which is expected to increase at a 12.1% CAGR through 2035 thanks to the implementation of universal health care in Indonesia and India. Due to EU Medical Device Regulation compliance deadlines, Europe has the second-largest stake, at roughly 24%. Manufacturers who can increase capacity while adhering to stricter environmental and quality standards will be rewarded in the upcoming 10 years.

Key Report Takeaways

• By Type

- Non-powdered gloves captured the leading revenue share of the Medical Gloves Market in 2025, reflecting global regulatory bans on powdered variants.

- Powdered gloves are projected to grow at a modest 6.8% CAGR through 2035 as demand persists in select price-sensitive emerging markets.

• By Material

- Nitrile gloves accounted for approximately 51.4% of the Medical Gloves Market in 2025, driven by allergy-free performance and chemical resistance.

- Neoprene gloves represent the fastest-growing material segment, forecast to register a CAGR of 13.1% through 2035.

• By Region

- North America retained the dominant position in the Medical Gloves Market with a 38% share in 2025.

- Asia-Pacific is set to expand at the highest regional CAGR of 12.1%, supported by rising surgical volumes and healthcare infrastructure investments.

Medical Gloves Market Size and Forecast (2021–2035)

Market sizing combines bottom-up manufacturer revenue analysis with top-down demand modeling across hospital networks, outpatient clinics, diagnostic laboratories, and pharmaceutical cleanrooms. Historical figures (2021–2024) are derived from audited annual reports and customs trade data; forecast values (2026–2035) employ a regression-adjusted compound growth model validated against procurement volume trends.