Medium Voltage Drives Market Summary

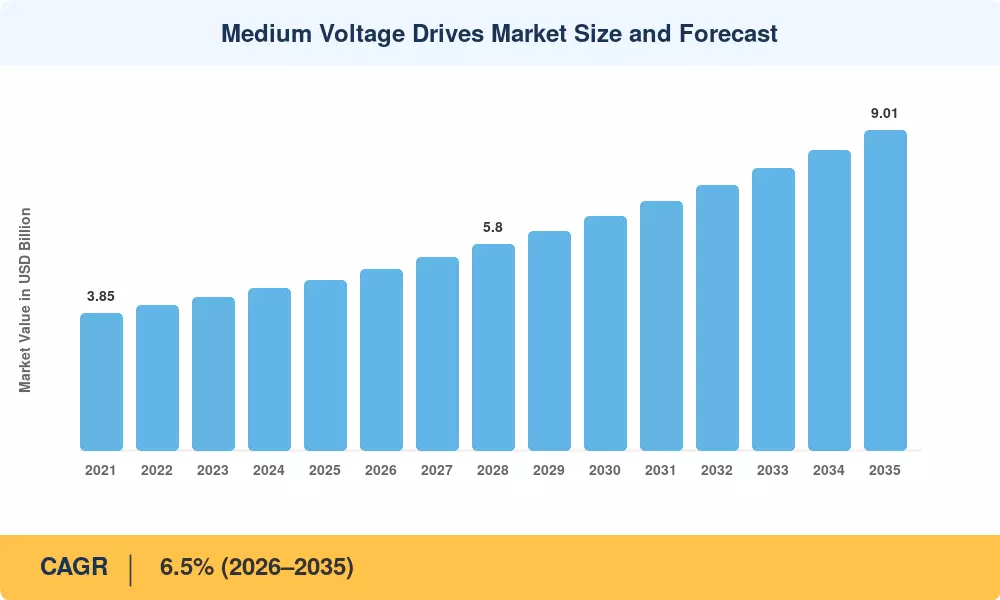

The Medium Voltage Drives Market reached an estimated USD 4.80 billion in 2025 and is projected to grow from USD 5.11 billion in 2026 to USD 9.01 billion by 2035, registering a CAGR of 6.5% during the 2026–2035 forecast period. Two forces are converging to fuel this expansion: tightening global efficiency mandates — the EU's revised Ecodesign Regulation (EU 2019/1781) now requires IE4 motor efficiency across a broader power range — and accelerating capital spending on industrial electrification, which the IEA pegged at over USD 135 billion globally in 2024 alone [1]. Together, these catalysts are making medium voltage drives a non-negotiable component of modern heavy-industry infrastructure.

Legacy fixed-speed motor systems, which still account for roughly 60% of installed medium voltage motor capacity worldwide, are being displaced by variable frequency drive technology that cuts energy consumption by 20–40% in centrifugal-load applications [2]. The U.S. Department of Energy estimates that motors above 375 kW represent nearly 30% of total industrial electricity demand, positioning the Medium Voltage Drives Market at the center of the industrial decarbonization conversation [3].

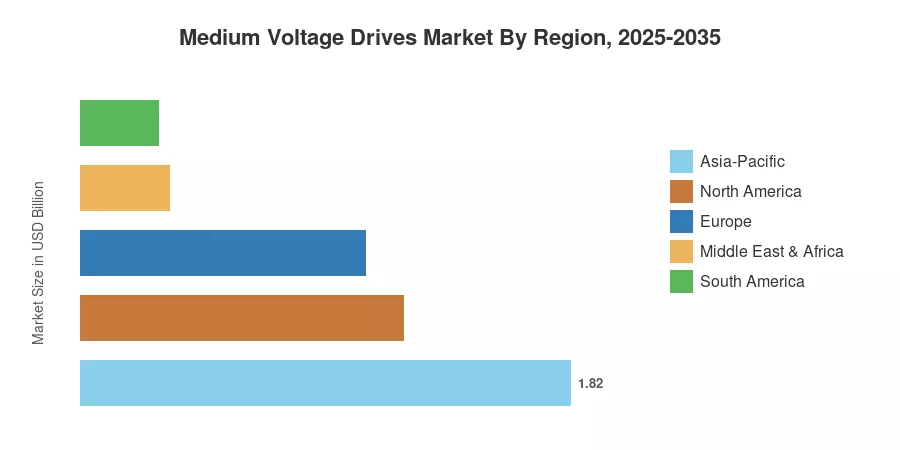

Asia-Pacific commands the largest share of the Medium Voltage Drives Market at approximately 38% of global revenue, driven by China's aggressive infrastructure and mining modernization programs. The region also registers the fastest CAGR at roughly 7.4%. Europe holds the second-largest share, near 22%, supported by stringent efficiency directives, while North America accounts for about 25% of the total. The next decade will see retrofit demand and digitalization of legacy plants open new growth corridors across every region.

Key Report Takeaways

• By Voltage Rating

- The 3.3 kV segment dominates the Medium Voltage Drives Market with approximately 42% revenue share in 2025, owing to its prevalence in water and wastewater pumping and general industrial processes.

- The 6.6 kV segment is forecast to grow at a CAGR of 7.1% through 2035, propelled by large-scale mining conveyor and compressor installations.

- The 11 kV-and-above category is gaining traction in power generation and petrochemical applications, contributing an estimated USD 0.58 billion in 2025.

• By Application

- Pumps represent the single largest application within the Medium Voltage Drives Market, commanding roughly 34% of revenue.

- Fans and blowers rank second, generating an estimated USD 1.20 billion in 2025.

- Compressor applications are expanding at a CAGR of 7.3%, the fastest among application segments, driven by LNG and petrochemical expansion.

• By Region

- Asia-Pacific leads with a 38% share of the Medium Voltage Drives Market in 2025.

- North America contributes approximately USD 1.20 billion and benefits from aging plant retrofit cycles.

- The Middle East & Africa region is forecast to grow at a CAGR of 6.9%, anchored by oil and gas capital expenditure.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up equipment shipment data from leading OEMs, top-down industrial motor electricity consumption models derived from IEA and EIA databases, and validated demand-side interviews across 12 end-use verticals. Historical figures (2021–2024) reflect confirmed shipment revenues; the base year (2025) is a composite estimate; and forecast values (2026–2035) apply a modeled 6.5% CAGR adjusted for cyclical capital expenditure patterns [4].