Melamine Formaldehyde Market Summary

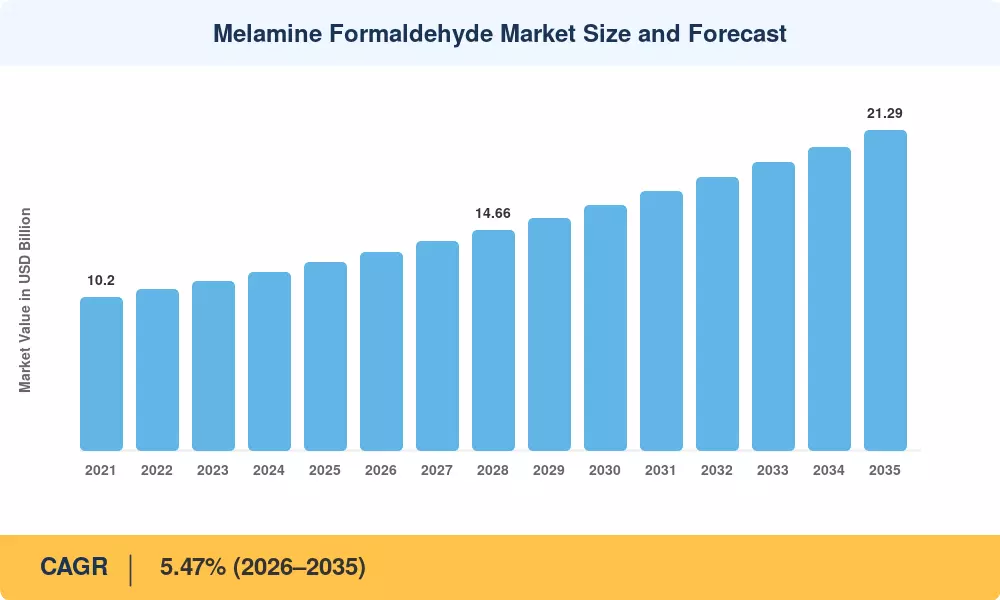

The global Melamine Formaldehyde Market was valued at USD 12.50 Billion in 2025 and is projected to grow from USD 13.18 Billion in 2026 to USD 21.29 Billion by 2035, registering a CAGR of 5.47% during the forecast period (2026–2035). Accelerating construction activity across Asia-Pacific economies — where China's residential renovation sector alone surpassed USD 430 billion in annual spending in 2024 — and tightening VOC-emission standards in the European Union and North America have created a durable demand runway for high-performance melamine-based resins. Government mandates such as the EPA's Formaldehyde Standards for Composite Wood Products Act continue to push manufacturers toward lower-emission resin chemistries, benefiting producers who have already invested in next-generation formulations [2].

The Melamine Formaldehyde Market is undergoing a technology shift as legacy urea-formaldehyde binders are increasingly replaced by melamine-fortified and fully melamine-based alternatives that offer superior moisture resistance, thermal stability, and surface hardness. Major resin producers committed more than USD 1.8 billion collectively to capacity expansions and R&D between 2022 and 2024, targeting ultra-low-emission grades suitable for indoor applications where regulatory limits on formaldehyde off-gassing have dropped below 0.05 ppm in several jurisdictions [3]. Automated dosing and curing systems are also lowering per-unit production costs by an estimated 8–12%, making melamine formaldehyde resins increasingly competitive against phenolic alternatives .

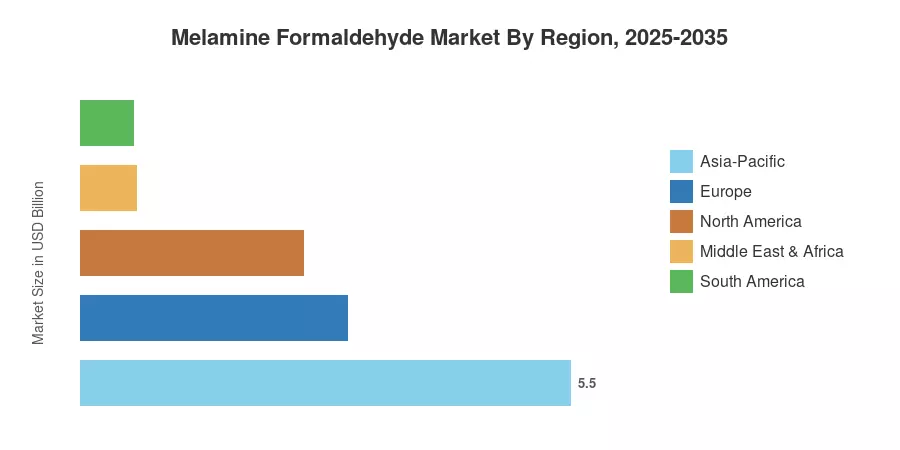

Asia-Pacific commands roughly 44% of the Melamine Formaldehyde Market by revenue, underpinned by China's dominant position in engineered-panel manufacturing and India's rapidly expanding furniture sector. The region also registers the fastest CAGR at 6.14% through 2035. Europe holds the second-largest share at approximately 24%, driven by stringent EN 717-series emission standards and strong demand for high-pressure laminates in kitchen and bathroom applications. North America accounts for about 20% of global revenue, with growth anchored to housing-start recovery and green-building certification programs. The outlook across all regions points to sustained volume gains as downstream industries continue specifying melamine-based products over less durable alternatives.

Key Report Takeaways

• By Type

- Iso-butylated melamine formaldehyde resin holds the largest type share at approximately 42% of global revenue, driven by broad adoption in automotive and industrial coatings.

- n-Butylated melamine formaldehyde resin is forecast to register the fastest segment CAGR of 6.08%, reflecting growing uptake in high-performance surface finishes.

• By Application

- The laminates application segment accounts for the highest revenue share within the Melamine Formaldehyde Market, capturing roughly 36% of 2025 demand.

- Paints and coatings application is projected to grow at a CAGR of 5.92% through 2035, supported by stricter environmental regulations favoring low-emission binders.

• By Region

- Asia-Pacific leads the Melamine Formaldehyde Market with a 44% share and a CAGR of 6.14%.

- North America is valued at approximately USD 2.50 Billion in 2025, buoyed by housing-sector recovery and composite-wood manufacturing expansion.

- Europe's Melamine Formaldehyde Market is shaped by the EU's Chemicals Strategy for Sustainability, which favors low-formaldehyde resin adoption.

Melamine Formaldehyde Market Size and Forecast (2021–2035)

Market Research Future developed size estimates using a combination of bottom-up revenue modeling from resin production volumes, top-down validation against downstream consumption in laminates, adhesives, and coatings, and triangulation with publicly available trade-flow and customs data from UN Comtrade and national chemical-industry associations [5].