Methionine Market Summary

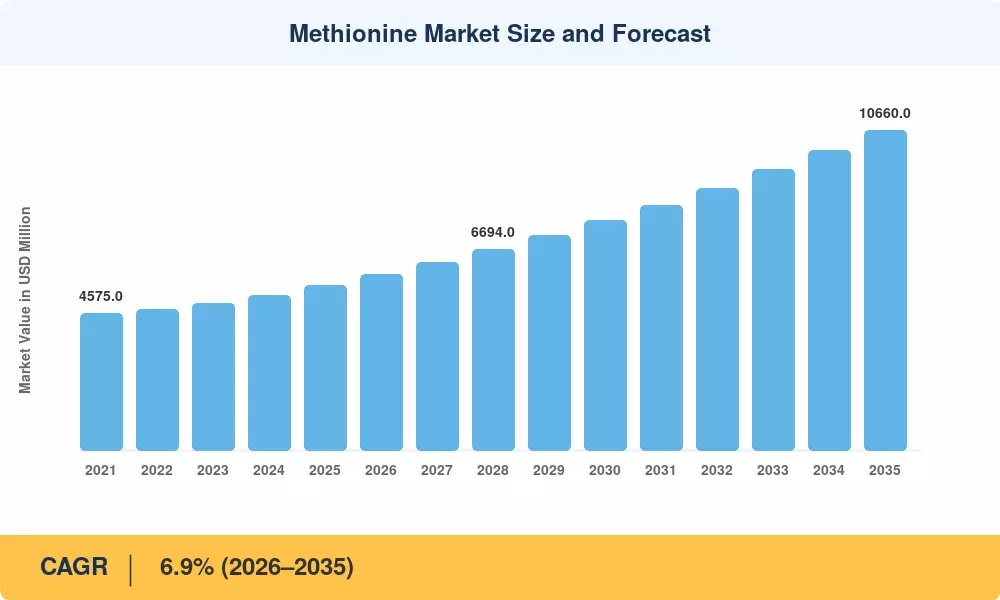

The global Methionine Market reached USD 5,480 million in 2025 and is projected to climb from USD 5,858 million in 2026 to USD 10,660 million by 2035, expanding at a 6.9% CAGR during the forecast period. Rising global meat consumption—particularly poultry and aquaculture—continues to underpin demand, while tightening EU feed-additive regulations and China's 14th Five-Year Plan mandates on green chemical production are injecting fresh capital into capacity expansion and process decarbonization [1][2].

A significant production-technology shift is underway within the Methionine Market. Legacy petrochemical synthesis routes, which still dominate capacity, face cost and carbon pressures from next-generation bio-based fermentation platforms. Evonik's completion of a green-hydrogen integration facility in Singapore in 2024 signaled an industry inflection point, attracting over USD 320 million in combined investments toward enzymatic and fermentation-based methionine pathways globally [3][4].

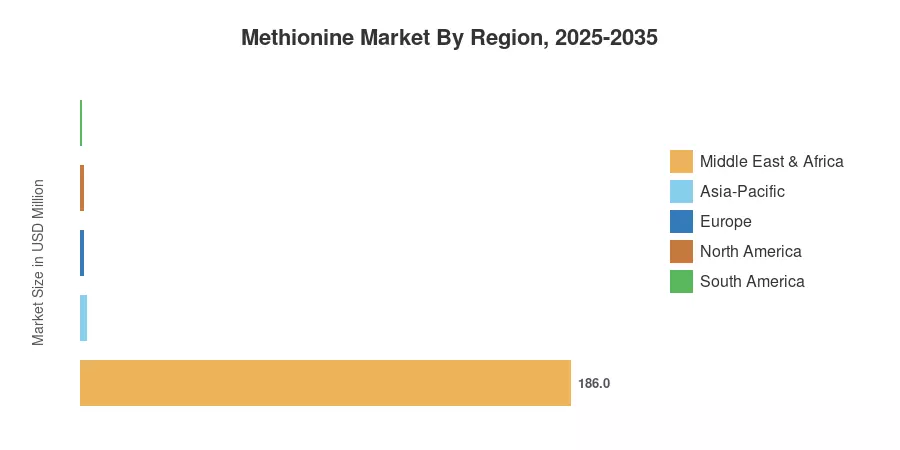

Asia-Pacific commands approximately 48.2% of the Methionine Market, driven by integrated poultry operations across China, Vietnam, and Indonesia. North America accounts for roughly 22.5%, anchored by advanced feed-formulation practices. Europe holds around a 20.8% share, with sustainability mandates accelerating adoption of lower-carbon production methods. As precision nutrition and aquaculture intensification reshape amino acid demand profiles, the Methionine Market trajectory through 2035 remains firmly upward.

Key Report Takeaways

• By Type

- Powder methionine held 63.1% of the Methionine Market in 2025, reflecting established handling and storage infrastructure across commercial feed mills.

- Liquid methionine is forecast to expand at an 8.9% CAGR through 2035, driven by compatibility with automated dosing systems.

• By Grade

- Feed-grade products captured 83.7% of 2025 volume, underscoring animal nutrition as the primary consumption channel.

- Pharmaceutical-grade methionine is projected to grow at a 9.3% CAGR to 2035.

• By Production Technology

- Petrochemical-based synthesis accounted for 79.3% of 2025 capacity.

- Bio-based fermentation is advancing at a 9.7% CAGR through 2035.

• By End-User Industry

- Animal feed represented 90.1% of Methionine Market consumption in 2025.

• By Region

- Asia-Pacific led with 48.2% volume share in 2025 and is poised for 8.1% CAGR growth through 2035.

- North America contributed 22.5% of the Methionine Market in 2025.

Methionine Market Size and Forecast (2021–2035)

Market sizing relies on a hybrid top-down and bottom-up approach, triangulating production capacity data, trade flow statistics, and downstream consumption patterns across animal feed, food-grade, and pharmaceutical applications. Historical figures (2021–2024) draw on confirmed shipment records and customs data; forecast projections (2026–2035) use econometric models calibrated to feed-demand growth, aquaculture expansion trajectories, and technology-adoption curves [5][6].

.webp?v=1784028609)