Microscopy Devices Market Summary

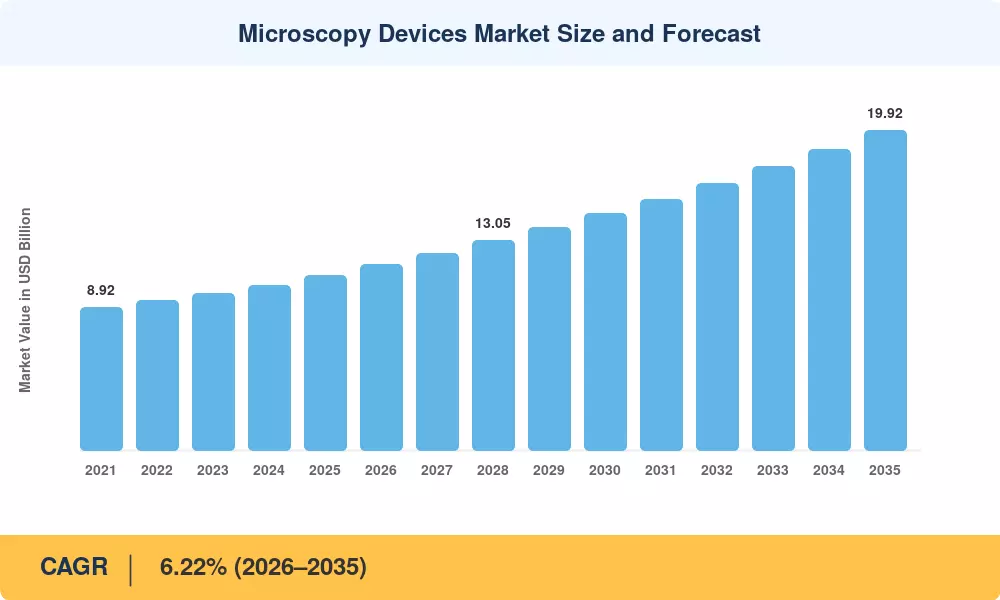

The Microscopy Devices Market size was valued at USD 10.89 Billion in 2025, and the market is projected to grow from USD 11.57 Billion in 2026 to USD 19.92 Billion by 2035, registering a CAGR of 6.22% during the forecast period 2026–2035. Two structural forces are shaping this trajectory: semiconductor fabrication roadmaps that require sub-nanometer metrology for gate-all-around transistor architectures, and the accelerating shift toward AI-driven pathology workflows in hospital and reference laboratory settings [1][2]. Rising government allocations for life-science infrastructure across the United States, China, and the European Union have reinforced demand for advanced imaging platforms at academic and clinical institutions alike.

A technology generational change is underway across the Microscopy Devices Market. Conventional benchtop optical systems — still the largest installed base — are being augmented by desktop cryogenic electron microscopy platforms priced for mid-tier research institutions, bringing structure-based drug discovery capabilities that were once confined to a handful of national laboratories [3]. The U.S. National Institutes of Health allocated over USD 1.2 billion toward biomedical imaging infrastructure between 2022 and 2024, and the EU Horizon Europe programme committed EUR 950 million to nanoscale research instrumentation through 2027 [4][5].

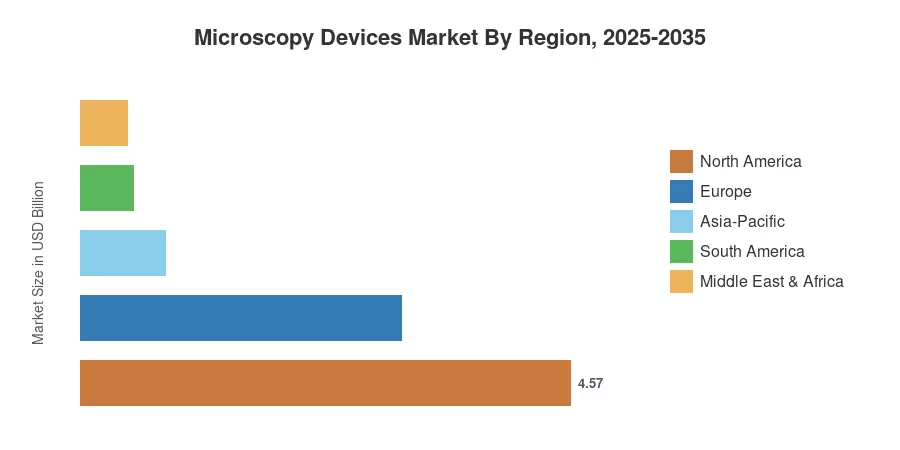

North America held approximately 42.0% of Microscopy Devices Market revenue in 2025, anchored by federal research funding and a dense network of pharmaceutical R&D centres. Asia-Pacific is the fastest-growing region, forecast to register a CAGR of 7.21% through 2035, propelled by semiconductor fab expansion in South Korea, Japan, and China. Europe accounted for the second-largest share at roughly 27.5%, driven by strong academic research traditions in Germany, the UK, and France. As AI-augmented imaging software matures and instrument price points continue to decline, the Microscopy Devices Market is positioned for broad-based geographic expansion over the coming decade.

Key Report Takeaways

• By Microscopy Type

- Optical microscopy accounted for an estimated 44.7% revenue share of the Microscopy Devices Market in 2025, sustained by clinical diagnostics and educational laboratory demand.

- Scanning probe microscopy is projected to grow at a CAGR of 6.48% through 2035, driven by nanoscale materials characterization requirements.

• By Application

- Life science applications represented approximately 36.5% of Microscopy Devices Market revenue in 2025.

- Nanotechnology research is forecast to register a 7.05% CAGR during the study period, reflecting increased government funding for nanomaterials development.

• By End User

- Academic and research institutes captured around 41.1% of Microscopy Devices Market revenue in 2025.

- Hospitals, clinics, and diagnostic laboratories are expected to post a CAGR of 7.06% through 2035, the fastest among end-user segments.

• By Region

- North America led the Microscopy Devices Market with a 42.0% share in 2025.

- Asia-Pacific is projected to expand at a 7.21% CAGR through 2035, fuelled by semiconductor industry growth and rising research budgets.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining vendor revenue disclosures, end-user procurement data, import–export databases, and primary interviews with laboratory directors, procurement officers, and OEM sales executives across 28 countries. Historical figures are validated against published annual reports and customs data; forecast values are modelled using bottom-up segment build-ups cross-checked with top-down macroeconomic indicators.