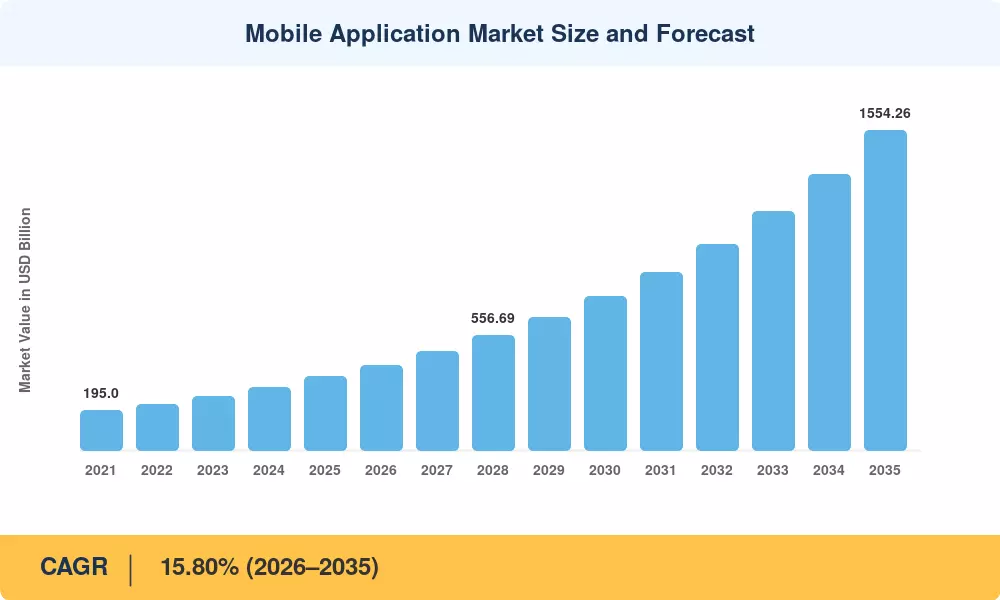

Mobile Application Market Summary

The Mobile Application Market was valued at USD 358.50 billion in 2025 and is projected to reach USD 415.14 billion by 2026 before climbing to USD 1,554.26 billion by 2035, expanding at a CAGR of 15.80% during the forecast period. A surge in global smartphone adoption—estimated at over 6.9 billion connected devices by 2025 [1]—continues to underwrite app-store economics, while government digital-identity programs in India, Brazil, and the EU are channeling hundreds of millions of first-time users into mobile-first ecosystems. Combined consumer and enterprise spending on mobile software crossed a trillion-dollar annual run rate for the first time in late 2024, signaling that the Mobile Application Market is transitioning from a growth story to a foundational pillar of the global digital economy [2].

Technologically, the Mobile Application Market is in the middle of a generational shift. Monolithic native codebases are giving way to cross-platform frameworks such as Flutter and Kotlin Multiplatform, while generative-AI development kits from Google and OpenAI now allow small studios to ship personalization features that previously required dedicated machine-learning teams. Commercial 5G networks—covering roughly 45% of the global population by mid-2025 [3]—are unlocking low-latency gaming, real-time AR commerce, and edge-computing workloads that simply could not run on prior networks.

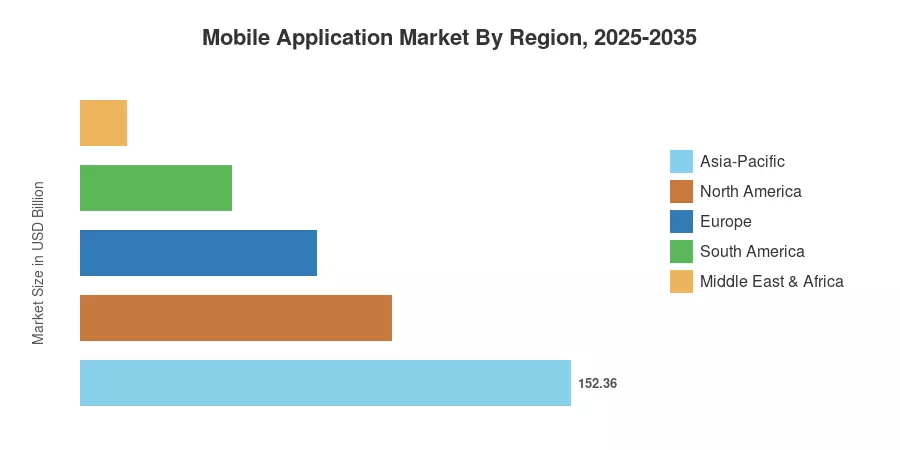

Asia-Pacific commands the largest share of the Mobile Application Market at roughly 42.5% of global revenue, driven by super-app ecosystems in China and Southeast Asia. South America is the fastest-growing region, posting a projected CAGR of 13.10% through 2035, as digital financial-inclusion initiatives in Brazil and Colombia onboard previously unbanked populations. North America retains the second-largest share at approximately 27.0%, anchored by premium consumer spending and a mature enterprise-SaaS installed base. As AI-powered functionality moves from a differentiator to a baseline expectation, the next decade promises to reshape every layer of this value chain.

Key Report Takeaways

• By Store Type

- Apple App Store captured an estimated 57.5% of Mobile Application Market revenue share in 2025, buoyed by premium user spending in North America and Western Europe.

- Third-party Android stores are forecast to expand at a 13.20% CAGR between 2026 and 2035, as OEM-specific storefronts gain traction in China and emerging markets.

• By Application Category

- Gaming retained approximately 46.1% of Mobile Application Market revenue in 2025, remaining the single largest category by a wide margin.

- Health and fitness applications are projected to grow at a 16.30% CAGR through 2035, accelerated by wearable integration and chronic-disease management platforms.

• By Operating System

- iOS held roughly 57.0% of Mobile Application Market spending in 2025, reflecting the platform's outsized monetization efficiency.

- HarmonyOS is set to grow at a 15.60% CAGR, fueled by Huawei's expanding device ecosystem in China and parts of the Middle East.

• By Monetization Model

- In-app purchases accounted for an estimated 52.5% of Mobile Application Market revenue in 2025.

- Subscription-based models show the fastest growth at a projected 14.90% CAGR to 2035, as developers pivot toward recurring-revenue economics.

• By Region

- Asia-Pacific captured approximately 42.5% of the mobile application market share in 2025.

- South America is the quickest-expanding geography at a 13.10% CAGR, propelled by Pix-enabled mobile payments in Brazil and rising smartphone penetration.

Market Size and Forecast (2021–2035)

Market Research Future's estimates integrate primary interviews with app-store executives, SDK analytics from leading attribution platforms, and secondary data from the ITU and GSMA. Historical figures (2021–2024) reflect reported industry revenues; the 2025 base year combines preliminary full-year data with Q4 extrapolations. Forecast values (2026–2035) apply a calibrated compound growth model with annual adjustments for regulatory shifts, device-cycle timing, and macroeconomic sensitivity.