Nano-Based Water Filtration Market Summary

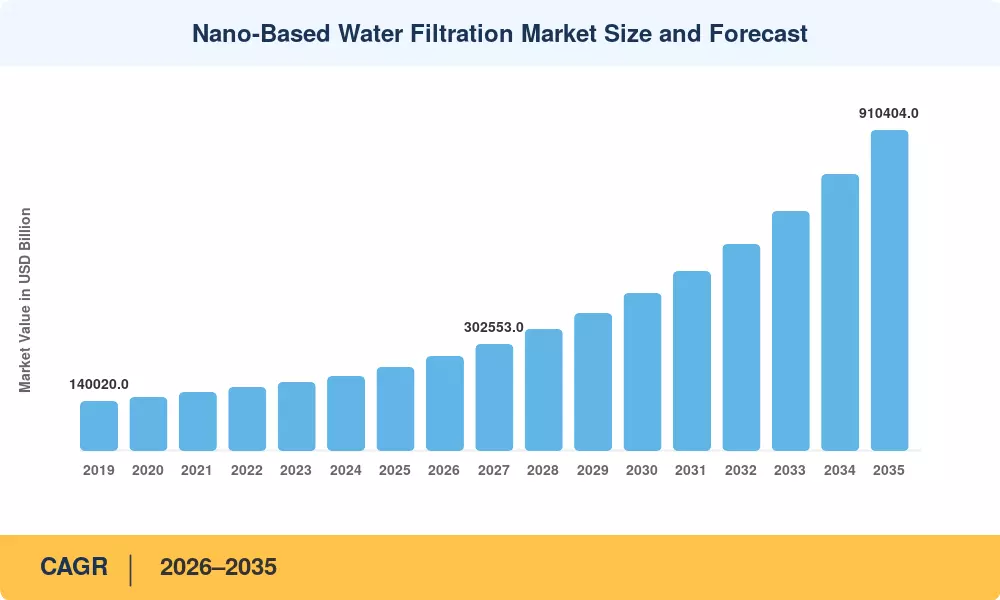

The global nano-based water filtration market was valued at USD 237.454 billion in 2025 and is projected to reach USD 267.622 billion by 2026, ultimately growing to USD 910.404 billion by 2035, registering a CAGR of 14.57% during the forecast period (2026–2035). The market's expansion is being driven primarily by rising global water scarcity and escalating demand for clean, potable water across both developed and emerging economies. According to the United Nations World Water Development Report, over 2 billion people worldwide lack access to safely managed drinking water, creating sustained demand for advanced filtration solutions [1]. Concurrently, government investments in water infrastructure — including multi-billion-dollar national clean water programs in the United States, China, and India — are channeling significant capital into next-generation purification technologies, of which nanofiltration is a central pillar [2].

Due to their demonstrated effectiveness in large-scale municipal and industrial water treatment, nanomembrane filters are the market's leading product segment, accounting for an expected USD 90,233 million in 2025 revenues. Carbon nanotube (CNT) filters, on the other hand, are expected to rise at a compound annual growth rate (CAGR) of roughly 17.8% through 2035 due to advancements in the scalability of graphene nanotube manufacture. OCSiAl made a historic announcement in November 2025 about the opening of its flagship graphene nanotube production plant in Differdange, Luxembourg. This facility will be the largest in the world, drastically lowering unit prices and hastening commercial adoption [3]. The supply chain for multi-walled carbon nanotubes has expanded as a result of Birla Carbon's October 2023 acquisition of Nanocyl SA, strengthening its use in cutting-edge conductivity and filtering applications [4].

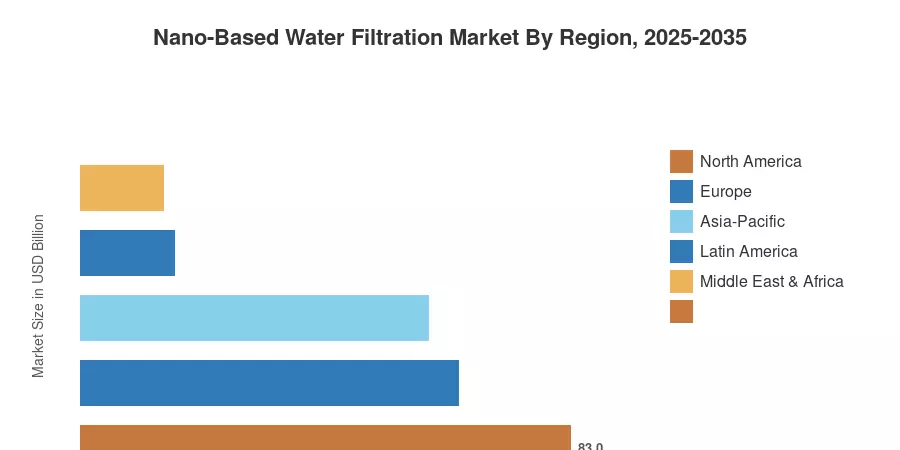

North America continues to be the leading region, accounting for over 35% of worldwide income in 2025 (about USD 83,109 million), thanks to strict EPA water quality regulations, significant municipal investment, and an established industrial base. The fastest-growing region is Asia-Pacific, which is expected to develop at a compound annual growth rate (CAGR) of more than 17% between 2026 and 2035 due to increased industrial wastewater creation, extensive government water initiatives in China and India, and rapid urbanization. Underpinned by EU regulatory mandates on water reuse and circular economy aims, Europe is the second-largest market, contributing around 27% of global revenue. In the future, double-digit growth is anticipated to be sustained through the end of the forecast period due to the convergence of falling nanomaterial manufacturing costs, growing municipal adoption in developing economies, and stricter worldwide water quality laws.

Key Report Takeaways

| Segment Dimension | Key Metric | Notes |

| Product Type — Dominant | Nanomembrane Filters: ~USD 90,233 Mn (2025) | Largest share due to municipal and industrial-scale deployment |

| Product Type — Fastest Growing | Carbon Nanotube Filters: ~17.8% CAGR | Driven by scalable graphene nanotube production breakthroughs |

| Application — Dominant | Municipal Water Treatment: ~USD 75,985 Mn (2025) | Underpinned by government clean water mandates globally |

| Application — Fastest Growing | Industrial Wastewater Treatment: ~16.9% CAGR | Rapid industrial expansion in APAC and stricter discharge norms |

| End User — Dominant | Municipal & Government Bodies: ~USD 83,109 Mn (2025) | Sustained by federal and state-level water infrastructure spending |

| End User — Fastest Growing | Residential: ~16.2% CAGR | Growing consumer awareness and point-of-use nano filter adoption |

| Region — Dominant | North America: ~USD 83,109 Mn (2025) | Mature infrastructure, stringent regulatory standards |

| Region — Fastest Growing | Asia-Pacific: ~17.5% CAGR | Urbanization, massive government investment and industrial growth |

| Market Concentration | Tier 1 players hold ~43.2% share | Moderately consolidated; top firms invest heavily in R&D |

| Overall Market | USD 237.454 Bn (2025) → USD 910.404 Bn (2035) | 14.57% CAGR across the forecast horizon |

Market Size and Forecast (2019–2035)

Market Research Future (MRFR) derives market sizing using a rigorous bottom-up and top-down approach, triangulating primary interviews with industry executives, publicly filed financial data, regulatory databases, and proprietary demand models. Historical values (2019–2024) are based on verified revenue data, the base year (2025) reflects the most current validated estimates, and the forecast period (2026–2035) applies segment-level growth modeling calibrated against macroeconomic indicators, policy pipelines, and technology adoption curves.