Naphtha Market Summary

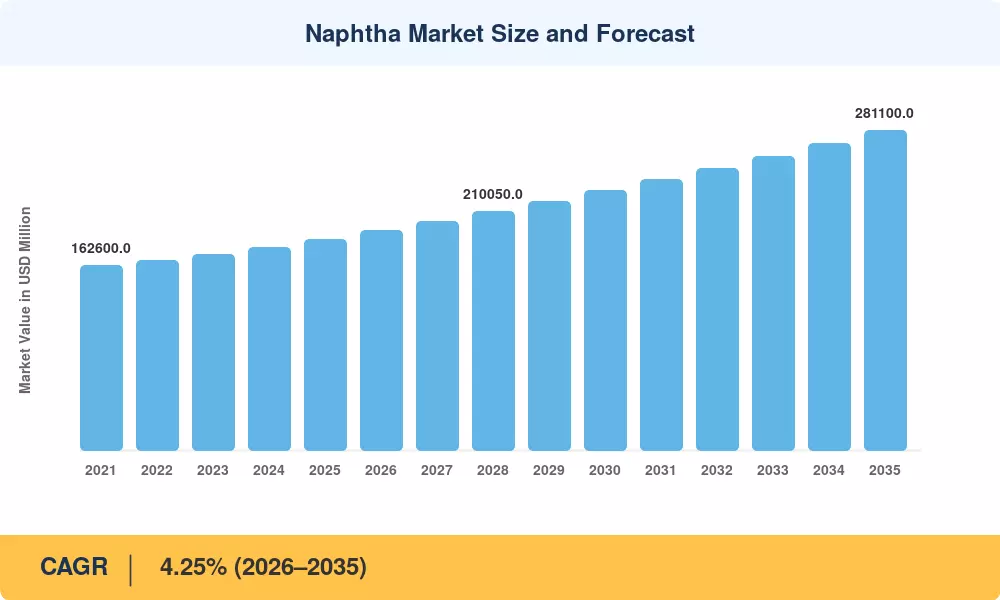

The global Naphtha Market reached an estimated USD 185,400 Million in 2025 and is projected to grow from USD 193,280 Million in 2026 to USD 281,100 Million by 2035, registering a CAGR of 4.25% during the forecast period. This expansion is anchored in sustained petrochemical feedstock demand from integrated olefin complexes across East and Southeast Asia, where governments have approved over USD 48 billion in new cracker investments since 2022 [2]. Policy catalysts such as China's 14th Five-Year Plan petrochemical capacity targets and India's Petroleum, Chemicals and Petrochemicals Investment Region (PCPIR) framework continue to underpin long-term volume commitments in the Naphtha Market.

A structural transformation is reshaping how refiners and traders value light hydrocarbon mixtures. Legacy straight-run processing routes are gradually giving way to advanced catalytic reforming units and modular steam cracking feedstock configurations designed to extract higher-value aromatics and olefins from the same barrel. The European Union's Renewable Energy Directive III (RED III) mandates a minimum 5.5% advanced-biofuel share in transport fuels by 2030, driving investment in bio-naphtha production that exceeded EUR 2.1 billion in announced capacity between 2023 and 2025 [3].

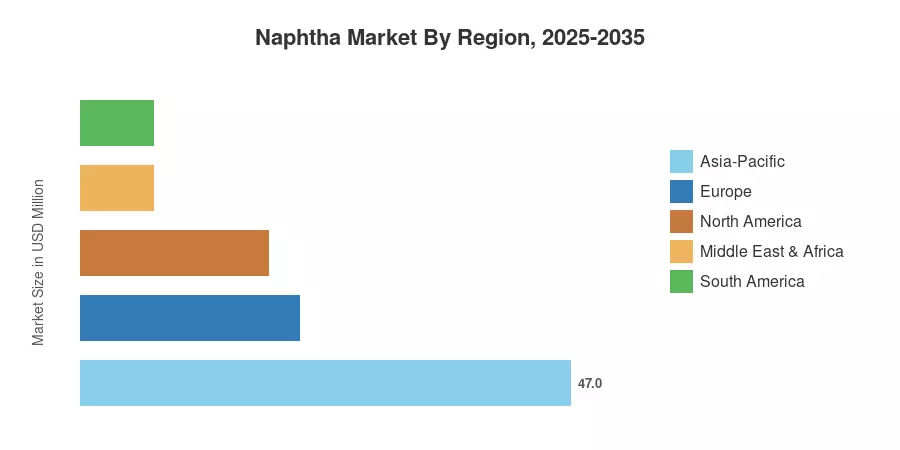

Asia-Pacific dominates the Naphtha Market with approximately 47% of global demand, supported by China, India, Japan, and South Korea's combined refinery products output. Europe holds the second-largest share at roughly 21%, while North America accounts for 18%. The fastest regional growth belongs to Asia-Pacific, expanding at a 5.05% CAGR as new mega-crackers in Zhejiang, Gujarat, and Rayong come online before 2030. As circular-feedstock substitution accelerates in developed regions and greenfield capacity rises in emerging economies, the Naphtha Market is set for a decade of compositional change alongside steady volume growth.

Key Report Takeaways — Naphtha Market

By Type

- Light naphtha commanded 61.5% of the naphtha market volume in 2025, driven by catalytic reformer demand for low-boiling-point hydrocarbon solvents and aromatic chemical feedstock

- Heavy naphtha is forecast to grow at a 3.48% CAGR through 2035, supported by residue-upgrading programs in Middle Eastern refineries

By Source

- Refinery-based grades retained roughly 74% of the Naphtha Market in 2025, reflecting the dominance of integrated refining-petrochemical complexes

- Bio-naphtha is advancing at a 5.90% CAGR to 2035, the fastest among all source segments, propelled by EU RED III mandates and California LCFS credits

By End-User

- Petrochemicals consumed 64% of global naphtha volume, as steam cracking feedstock requirements from ethylene producers remain the primary consumption driver

- Paints and coatings end-users are expanding at a 4.10% CAGR, underpinned by construction activity in Southeast Asia

By Region

- Asia-Pacific held 47% of the Naphtha Market demand in 2025, with new cracker capacity in China and India absorbing incremental supply

- North America is experiencing a refinery products surplus from condensate splitter expansions along the Gulf Coast

Naphtha Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework integrates refinery throughput data from the IEA, trade-flow statistics from UN Comtrade, and company-level production disclosures to construct both historical and forward-looking Naphtha Market valuations. Forecast assumptions incorporate planned capacity additions, announced plant closures, and policy-driven demand shifts across chemical processing fuels and fuel blending components.