Nuclear Decommissioning Market Summary

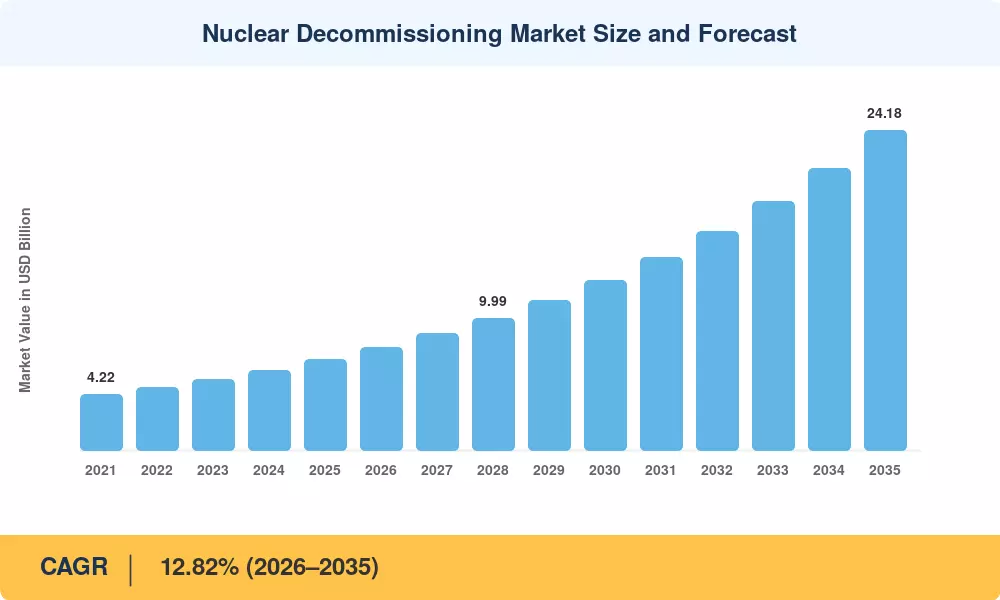

The Nuclear Decommissioning Market reached an estimated USD 6.84 billion in 2025 and is projected to grow from USD 7.72 billion in 2026 to USD 24.18 billion by 2035, registering a CAGR of 12.82% during the forecast period (2026–2035). This expansion is anchored in the permanent shutdown of aging reactor fleets across Europe and North America, coupled with binding government mandates — such as Germany's complete nuclear phase-out and the UK's Nuclear Decommissioning Authority budget exceeding GBP 3.2 billion annually — that compel operators to initiate reactor vessel decommissioning programs on accelerated timelines [2][3].

A technology transformation is reshaping how the Nuclear Decommissioning Market operates. Legacy manual dismantlement methods, which once stretched projects across 40–60 years under SAFSTOR DECON nuclear decommissioning approaches, are giving way to robotic nuclear decommissioning systems that cut project timelines by 30–40%. The U.S. Department of Energy allocated over USD 7.5 billion toward nuclear site remediation and cleanup activities in its 2024 Environmental Management program, reflecting the scale of investment flowing into advanced decontamination and nuclear waste segmentation decommission technologies [4][5].

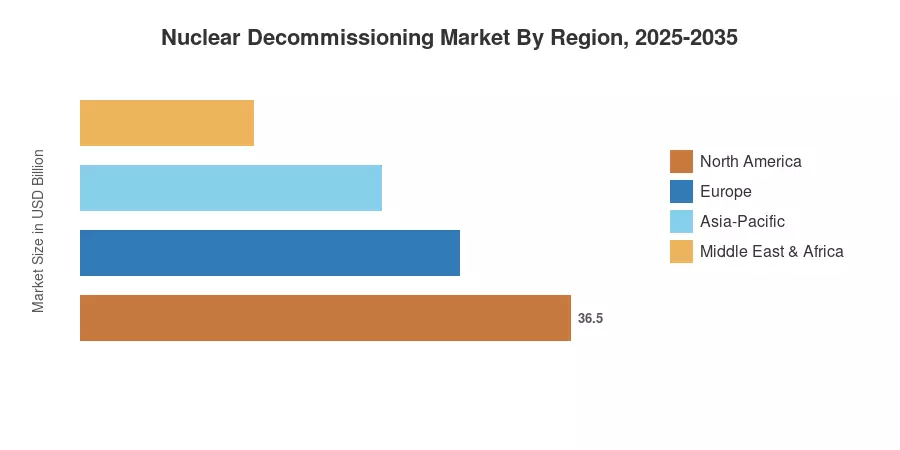

Europe commands the largest share of the Nuclear Decommissioning Market at approximately 38.5%, driven by the continent's extensive fleet of permanently shut-down reactors. North America is the fastest-growing region with a CAGR of 14.6%, fueled by decommissioning fund nuclear utility requirements and an accelerating wave of commercial reactor retirements in the United States. Asia-Pacific holds the second-largest share at roughly 26%, as Japan's post-Fukushima decommissioning agenda and South Korea's energy transition policies generate sustained demand through 2035 [6][7].

Key Report Takeaways

• By Reactor Type

- Pressurized Water Reactors (PWR) account for approximately 44% of the Nuclear Decommissioning Market, reflecting the global dominance of this reactor design in commercial fleets undergoing permanent shutdown

- Boiling Water Reactors (BWR) are growing at a CAGR of 13.1%, as several U.S. and Japanese BWR units enter active reactor vessel decommissioning phases

- Pressurized Heavy Water Reactors (PHWR) represent an estimated USD 1.12 billion in 2025 value, concentrated in Canadian CANDU fleet retirements

• By Application

- Commercial Power Reactors dominate the Nuclear Decommissioning Market with over 72% share, driven by accelerated SAFSTOR DECON nuclear decommissioning timelines

- Prototype Power Reactors are expanding at a CAGR of 11.8%, as legacy research and demonstration units reach end-of-life across Europe

• By Region

- Europe leads at 38.5% share due to aggressive nuclear phase-out programs in Germany, the UK, and France

- North America is growing fastest at 14.6% CAGR, propelled by decommissioning fund nuclear utility mandates and NRC regulatory deadlines

- Asia-Pacific holds roughly USD 1.78 billion in 2025 value, anchored by Japan's Fukushima reactor vessel decommissioning program

Market Size and Forecast (2021–2035)

The market sizing methodology combines bottom-up project cost analysis across 210+ permanently shut-down reactors worldwide with top-down validation using government decommissioning budgets, regulatory filings, and operator annual reports. Historical data (2021–2024) draws on NRC, IAEA, and NDA financial disclosures, while forecast estimates (2026–2035) incorporate announced shutdown schedules, decommissioning fund nuclear utility reserve balances, and policy-driven timeline accelerations[8].

.webp?v=1784551655)