Open Source Intelligence (OSINT) Market Summary

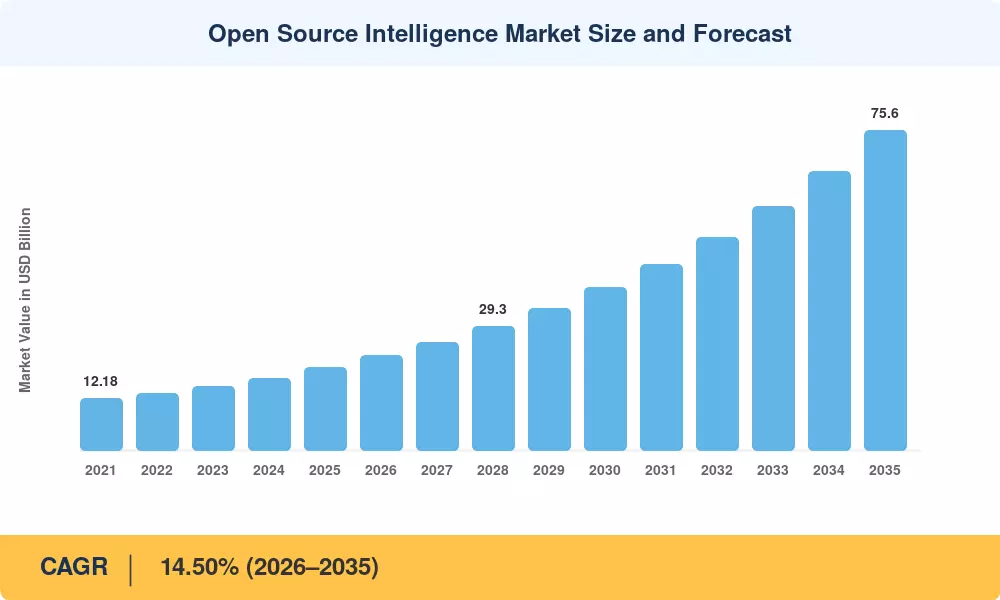

The Open Source Intelligence Market stood at USD 19.50 billion in 2025 and is projected to reach USD 22.35 billion in 2026, climbing to USD 75.60 billion by 2035 at a compound annual growth rate of 14.50% during the 2026–2035 forecast window. This expansion tracks directly to escalating geopolitical instability and the growing recognition among national security agencies that publicly accessible data — when properly aggregated and analyzed — delivers actionable insights at a fraction of the cost of classified collection programs. The U.S. Intelligence Community's 2024 budget authorization alone earmarked over USD 2.1 billion for open-source exploitation capabilities, signaling institutional commitment that reverberates across allied nations [1].

We are in a profound technological change. Legacy keyword-based monitoring tools are giving way to AI-native designs that ingest multilingual text, picture, and geographic sources simultaneously. Vendors are incorporating big language models directly into collection pipelines, allowing analysts to shift from descriptive reporting to predictive threat assessment in near real time. Between 2024 and 2027, the European Commission’s Horizon Europe program has committed EUR 1.3 billion to dual-use AI research, with OSINT automation being a priority application area [2].

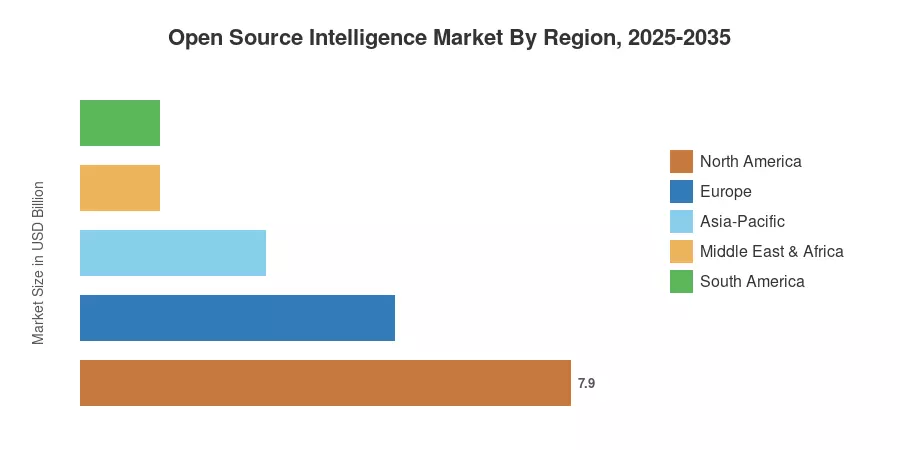

North America holds a share of around 40.5% in the Open Source Intelligence Market, owing to defense and homeland security procurement cycles. Asia-Pacific is the fastest-growing region with a CAGR of 15.30% due to the rising digital surveillance infrastructure in India and cybersecurity legislation in Japan post 2024. Europe has the second-highest share, at over 26.0%, supported by NATO interoperability requirements and the EU’s Digital Operational Resilience Act. As commercial adoption is gaining momentum, especially in financial institutions and multinational enterprises, the Open Source Intelligence Market is set to transform the way organizations throughout the globe perceive risk.

Key Report Takeaways

• By Analysis Type

- Data analytics accounted for approximately 36.3% of the Open Source Intelligence Market in 2025, reflecting heavy investment in structured data correlation engines.

- AI-driven security analysis is forecast to expand at a 19.10% CAGR through 2035, outpacing every other analysis category as threat detection automates.

• By Data Source

- Social media data streams represented 49.3% of input volume across the Open Source Intelligence Market in 2025.

- Cloud-based deployment captured a 61.2% share in 2025, as agencies and enterprises prioritize scalable, remotely accessible platforms.

• By Geography & End User

- North America maintained the largest regional footprint in the Open Source Intelligence Market, contributing 40.5% of global revenue.

- Asia-Pacific is advancing at a 15.30% CAGR, the highest among all regions.

- Government intelligence agencies led end-user spending with a 41.5% share in 2025.

Market Size and Forecast (2021–2035)

MRFR’s size technique is based on a triangulation of top-down government procurement data, bottom-up vendor revenue disclosures, and third-party technology adoption surveys. Historical values (2021-2024) represent confirmed spending. The 2025 base year is based on preliminary budgetary data. The Forecast (2026-2035) projections use a calibrated CAGR based on policy pipelines, technological readiness curves and regional defense budget trajectories.