Paints Coatings Market Summary

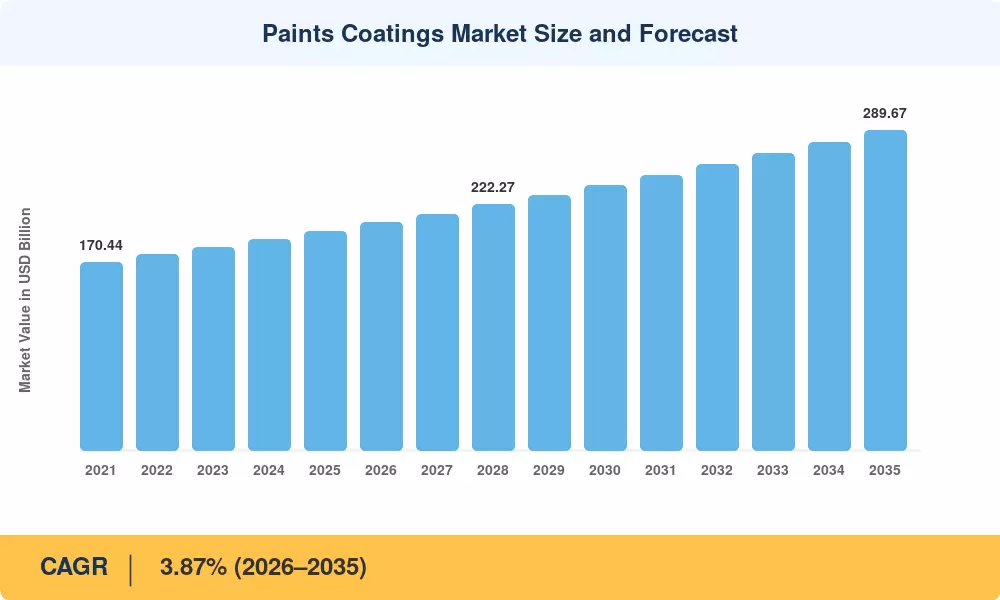

The Paints and Coatings Market reached an estimated USD 198.42 billion in 2025 and is projected to climb from USD 206.15 billion in 2026 to USD 289.67 billion by 2035, registering a CAGR of 3.87% during 2026–2035. Aggressive infrastructure spending — highlighted by India's INR 11.1 lakh crore capital expenditure allocation in FY 2024–25 [2] and the U.S. Infrastructure Investment and Jobs Act channeling USD 550 billion into bridges, roads, and water systems [3] — continues to anchor demand for protective coating materials and architectural paints across both emerging and developed economies.

A sweeping technology shift is reshaping how the Paints and Coatings Market operates. Legacy solvent-borne formulations are losing ground to waterborne coatings, which already represent the dominant technology platform. The European Union's Directive 2004/42/EC and subsequent Decopaint Directive amendments have progressively capped VOC limits, pushing manufacturers toward low-emission chemistries [4]. Concurrently, powder coatings are gaining traction in industrial applications where zero-VOC performance and recyclability command premium positioning. Global capital expenditure on waterborne and UV-cured production lines exceeded USD 4.2 billion in 2024 alone [5].

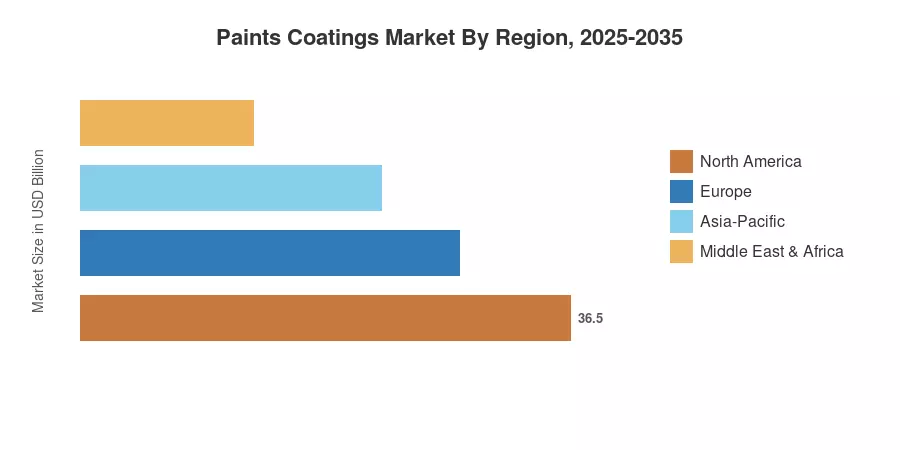

Asia-Pacific commands the largest revenue share in the Paints and Coatings Market at approximately 49.3%, driven by rapid urbanization in China, India, and Southeast Asia. The region is simultaneously the fastest-growing, posting a projected CAGR of 5.28% through 2035. Europe holds roughly 22.4% of global revenue, underpinned by stringent sustainability mandates that accelerate the shift toward specialty paint solutions and bio-based resins As digital color-matching tools and automated plant scheduling become standard, the next decade will reward producers who marry formulation innovation with supply-chain agility.

Key Report Takeaways

• By Resin

- Acrylics led the Paints and Coatings Market with a 38.2% share in 2025, driven by versatility across decorative paints and industrial coatings applications

- Polyurethane-based systems are projected to grow at a 4.45% CAGR through 2035, fueled by rising demand for corrosion-resistant coatings in heavy infrastructure

- Epoxy resins remain essential for protective coating materials in marine, oil-and-gas, and flooring end uses

• By Technology

- Waterborne coatings accounted for 54.1% of the Paints and Coatings Market in 2025, reflecting regulatory momentum and consumer preference for low-VOC products

- Powder coatings are expanding at a 4.68% CAGR, gaining share in automotive coatings and appliance finishing

• By End-User Industry

- Architectural paints commanded the largest end-user segment, contributing USD 103.24 billion in 2025 revenue across residential and commercial construction

- Automotive coatings represent the fastest-growing end-user vertical in the Paints and Coatings Market, driven by electric-vehicle production ramps and lightweighting trends

• By Region

- Asia-Pacific dominated the Paints and Coatings Market with a 49.3% revenue share in 2025

- North America is projected to reach USD 52.78 billion by 2035, supported by the reshoring of manufacturing and federal infrastructure programs

Market Size and Forecast (2021–2035)

MRFR's sizing model combines top-down trade-flow analysis with bottom-up manufacturer revenue aggregation, cross-referenced against customs data, industry association reporting, and proprietary channel checks across 42 countries. Historical values (2021–2024) reflect audited trade statistics; the base year (2025) integrates preliminary full-year shipment data; and the forecast period (2026–2035) applies a compound trajectory calibrated to macroeconomic indicators, raw-material price indices, and regulatory phase-in schedules.

.webp?v=1783672212)