Particle Therapy Market Summary

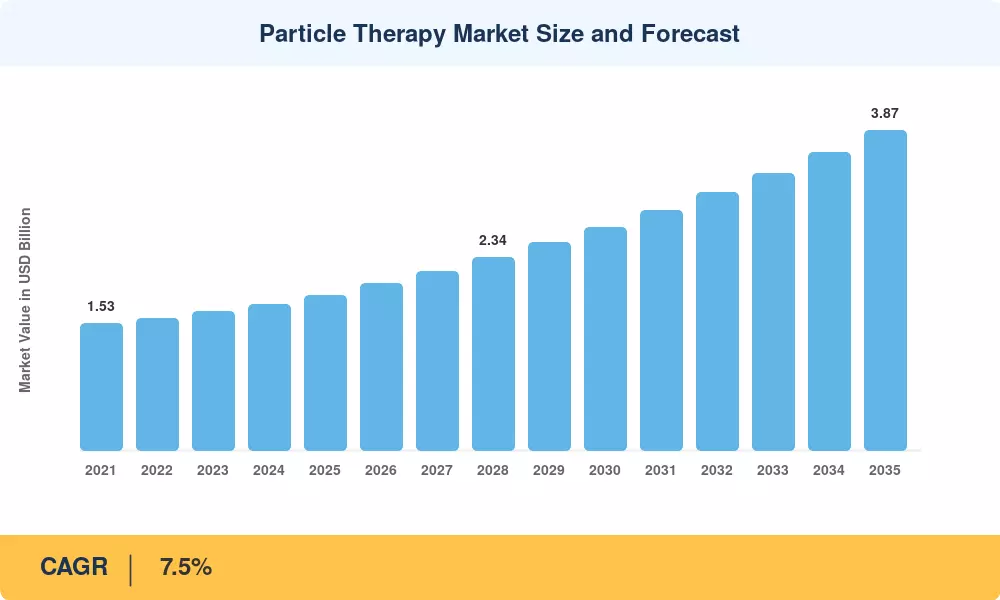

The Particle Therapy Market stood at USD 1.88 billion in the 2025 base year, with the forecast period opening at USD 2.02 billion in 2026 and climbing to USD 3.87 billion by 2035 at a compound annual growth rate of 7.5%. Two policy catalysts set the pace for this expansion: Medicare's 2024 local-coverage determinations, which broadened reimbursement eligibility for proton-based treatments across the United States, and Japan's decision to add carbon-ion procedures to its national health-insurance schedule [1][2]. Together, these moves injected near-term revenue visibility into a capital-intensive sector that had long depended on philanthropic or government-backed financing alone.

The technology landscape is pivoting away from legacy multi-room cyclotron bunkers toward compact single-room synchrocyclotron platforms that cut civil-works costs by as much as 55%. Vendors such as Mevion Medical Systems and IBA have commercialized units priced below USD 35 million—roughly half the installed cost of a traditional three-gantry suite—opening the door for mid-tier academic medical centers and private oncology networks [3]. FLASH-dose delivery research, which compresses radiation into millisecond bursts, is accelerating through Phase II trials and could redefine the total addressable patient pool within the next five years [4].

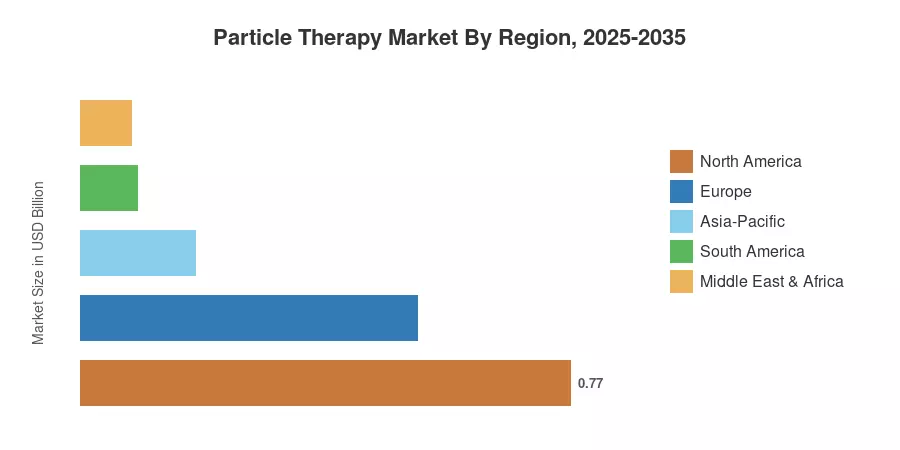

North America controlled approximately 41% of the Particle Therapy Market in 2025, anchored by more than 45 operational treatment rooms across the United States. Asia-Pacific is the fastest-growing geography, advancing at a 9.7% CAGR through 2035, fueled by China's provincial hospital build-outs and South Korea's National Cancer Center expansions. Europe, the second-largest region at roughly 28% share, continues to benefit from cross-border referral frameworks such as the European Reference Networks for rare pediatric tumors. Capital deployment into emerging markets is expected to accelerate as financing models mature and patient awareness deepens over the forecast decade.

Key Report Takeaways — Particle Therapy Market

By Type

- Proton therapy commanded 87% of the Particle Therapy Market in 2025, reflecting its established clinical evidence base and broader payer acceptance.

- Heavy-ion therapy is projected to grow at an 8.5% CAGR through 2035, driven by superior dose conformality for radioresistant tumors.

By System

- Multi-room configurations held 59% share of the Particle Therapy Market in 2025, benefiting from higher patient throughput per facility.

- Single-room systems are advancing at an 8.1% CAGR, reflecting compact footprints attractive to community hospital networks.

By Cancer Type

- Pediatric indications represented 46% of market revenue in 2025, given the clinical imperative to minimize late-effect toxicity in young patients.

- Breast cancer applications are recording a 7.8% CAGR between 2026 and 2035, supported by randomized trial data on cardiac-sparing benefits.

By Region

- North America retained 41% of the Particle Therapy Market share in 2025, led by U.S. Medicare coverage expansions.

- Asia-Pacific is on track for a 9.7% CAGR through 2035, underpinned by government-funded center construction in China, Japan, and South Korea.

Particle Therapy Market Size and Forecast (2021–2035)

Market Research Future's estimates are built on a triangulated methodology combining bottom-up facility-level revenue modeling, top-down insurance-claims analytics, and primary interviews with 120+ radiation oncology directors and procurement leads across 18 countries. Historical figures draw on audited annual reports from publicly listed equipment vendors supplemented by national cancer-registry throughput data.