Payment Gateway Market Summary

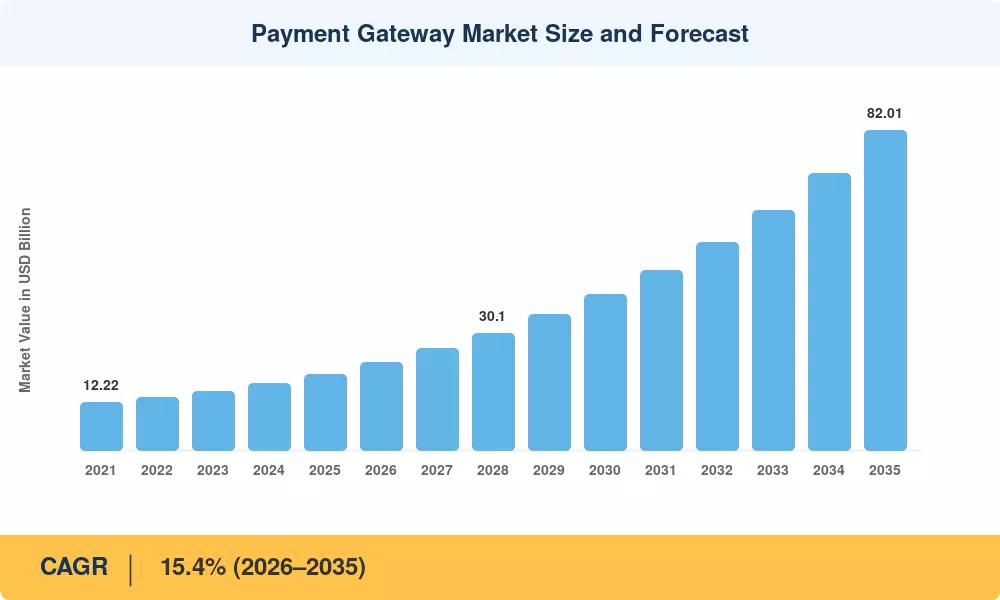

The Payment Gateway Market was valued at USD 19.58 billion in 2025 and is projected to reach USD 22.60 billion in 2026, climbing to USD 82.01 billion by 2035 at a compound annual growth rate of 15.4% during the 2026–2035 forecast window. This expansion is anchored in the global proliferation of real-time payment rails — India's UPI processed over 13 billion transactions in a single month during late 2024 [1] — and increasingly stringent strong-customer-authentication mandates rolling out across the EU and Southeast Asia [2]. Governments and central banks are actively incentivizing cashless commerce, and every incremental percentage point of card or wallet penetration translates directly into higher gateway transaction volumes.

Legacy batch-processing payment architectures are giving way to API-first, microservices-based gateway stacks capable of handling tokenized card-on-file flows, buy-now-pay-later decisioning, and multi-acquirer routing in a single call. Global venture investment in payment infrastructure exceeded USD 18 billion in 2024 alone [3], with significant capital flowing into orchestration layers that sit atop traditional gateways and add intelligent routing logic. The Payment Gateway Market stands at the centre of this transformation.

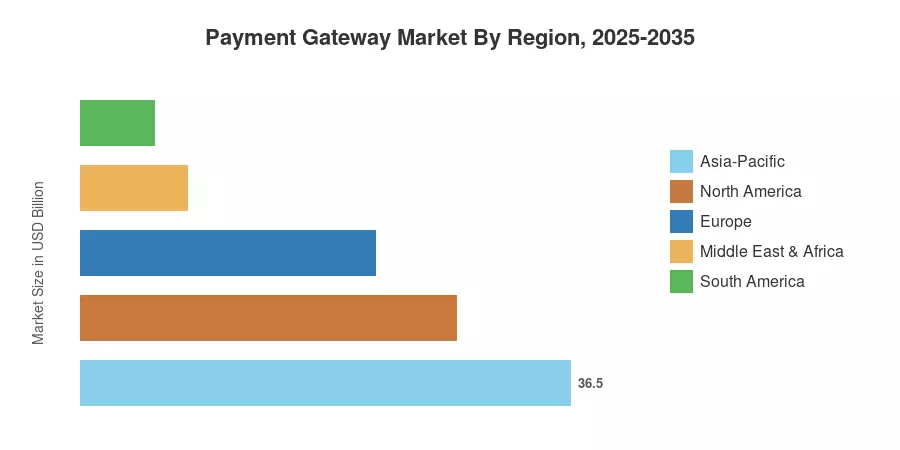

Asia-Pacific commands the largest share of the Payment Gateway Market at roughly 36.5% of 2025 revenue, powered by super-app ecosystems in China, India, and Southeast Asia. Middle East & Africa is positioned as the fastest-growing region with an anticipated 18.2% CAGR through 2035, driven by Saudi Arabia's Vision 2030 cashless targets and CBDC pilot programs. North America holds the second-largest position, contributing approximately 28% of global spending. The decade ahead promises accelerating consolidation, deeper AI-driven fraud screening, and a blurring line between gateways and full-stack payment platforms.

Key Report Takeaways

• By Type

- Hosted gateways accounted for approximately 52% of 2025 Payment Gateway Market revenue, reflecting merchant preference for quick integration and PCI compliance offloading.

- Self-hosted deployments are forecast to expand at a 15.2% CAGR through 2035 as enterprise merchants seek granular control over tokenization vaults and routing rules.

• By Enterprise Size & Channel

- Small and medium enterprises drove roughly 60% of the 2025 Payment Gateway Market transaction volume, aided by subscription-priced, low-code integrations.

- Mobile in-app payments are advancing at a 17.1% CAGR, fueled by super-app SDKs embedded in ride-hailing and food-delivery ecosystems.

• By End-User Industry & By Region

- Retail and e-commerce represented about 29% of 2025 demand across the Payment Gateway Market, while travel and hospitality is projected to record the fastest segment CAGR of 15.8%.

- Asia-Pacific retained 36.5% of global revenue in 2025, whereas the Middle East & Africa region is projected to post an 18.2% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimation framework synthesizes primary interviews with payment processors, gateway vendors, and acquiring banks alongside secondary data from central bank settlement reports, card-network disclosures, and app-store analytics. Historical figures (2021–2024) reflect verified transaction-value data; the base year 2025 is calibrated against the latest quarterly filings; and the forecast period (2026–2035) applies a 15.4% CAGR derived from regression modelling of gateway API call volumes, merchant onboarding rates, and real-time-payment adoption curves.

.webp?v=1782471417)