Photoresist Market Summary

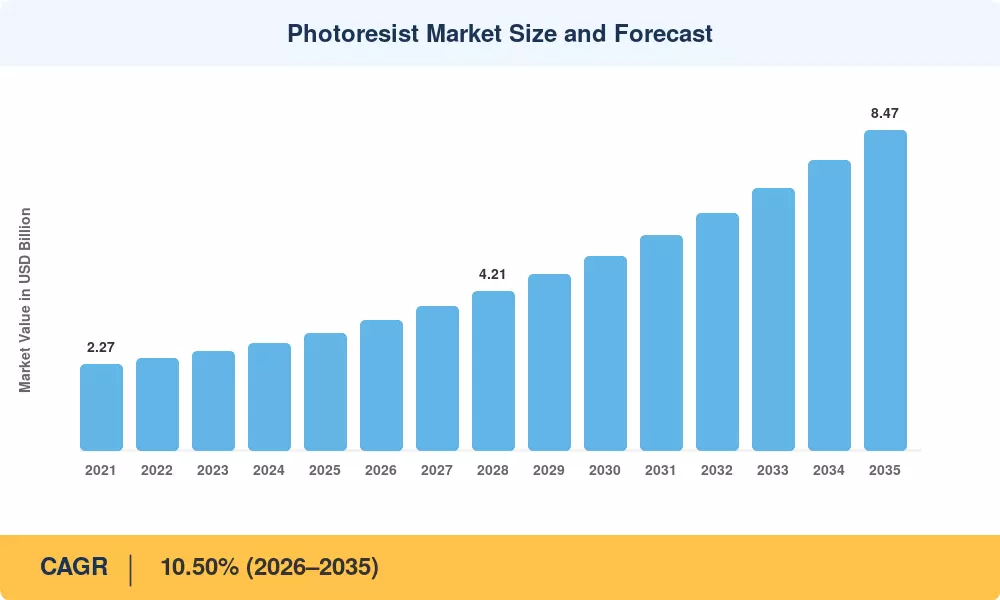

The global Photoresist Market reached an estimated USD 3.09 billion in 2025 and is projected to grow from USD 3.45 billion in 2026 to USD 8.47 billion by 2035, registering a CAGR of 10.50% during the forecast period. Government-backed semiconductor localization programs — including the U.S. CHIPS and Science Act allocating USD 52.7 billion and the EU Chips Act committing EUR 43 billion — are reshaping resist supply chains and compelling manufacturers to establish blending and quality-assurance operations closer to new fab clusters [2][3].

A technology inflection is well underway. Legacy KrF and g-line formulations still serve cost-optimized nodes for automotive microcontrollers and display panels, but EUV lithography has moved decisively from pilot lines into high-volume manufacturing at sub-5 nm logic nodes. Metal-oxide dry resists are now essential where chemically amplified platforms cannot manage photon shot noise and line-edge roughness at acceptable yields [4]. Capital expenditure across the top five foundries exceeded USD 130 billion in 2024 alone, pulling advanced resist consumption upward [5].

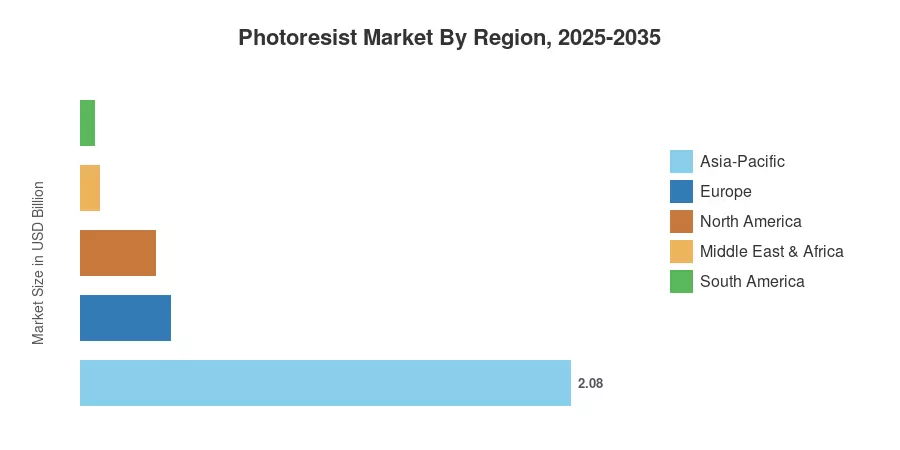

Asia-Pacific dominates the Photoresist Market with a 67.2% revenue share in 2025, anchored by fabrication clusters in Taiwan, South Korea, and Japan. North America is the fastest-growing region, expanding at a 10.50% CAGR through 2035 as greenfield fab projects in Arizona, Ohio, and Texas catalyze local resist demand. Europe holds the second-largest share outside Asia-Pacific, driven by automotive-grade semiconductor expansion in Germany and the Netherlands. The decade ahead will be defined by resist chemistry innovation tracking alongside continued node shrinkage and heterogeneous integration architectures.

Key Report Takeaways

• By Resist Type

- ArF immersion formulations commanded 34.1% of the Photoresist Market share in 2025, reflecting continued dominance at mature immersion nodes.

- EUV metal-oxide and dry resists are projected to expand at an 11.90% CAGR through 2035, driven by sub-3 nm logic ramps.

• By Tone

- Positive-tone resists captured 76.3% of the Photoresist Market revenue in 2025.

- Negative-tone resists post the fastest growth at a 10.40% CAGR to 2035, propelled by advanced packaging and 3D-NAND lithography layers.

• By Application

- Semiconductors and ICs accounted for 58.5% of Photoresist Market demand in 2025.

- Advanced packaging applications are set to grow at an 11.00% CAGR through 2035.

• By End-User Industry

- Electronics and electricals represented 65.4% of the Photoresist Market in 2025.

- Automotive and mobility end users are expanding at a 10.90% CAGR, the fastest among all verticals.

• By Region

- Asia-Pacific held a 67.2% share of the Photoresist Market in 2025.

- North America is forecast to grow at a 10.50% CAGR through 2035.

Photoresist Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework combines bottom-up semiconductor wafer-start models, resist consumption-per-layer coefficients, and fab-level capacity announcements across more than 200 fabrication facilities globally. Historical values (2021–2024) are derived from audited financial disclosures of leading resist suppliers and verified against trade data from SEMI and the Japan Electronics and Information Technology Industries Association (JEITA)[6].