Plant Asset Management Market Summary

The Plant Asset Management Market stood at USD 10.40 billion in 2025 and is projected to open the forecast window at USD 11.75 billion in 2026, climbing to USD 30.55 billion by 2035. Industrial operators are accelerating digitalization budgets to comply with tightening safety and emissions reporting mandates, and that regulatory pressure is doing as much to lift demand as any single technology rollout. Utilities and process manufacturers alike are treating asset visibility as a compliance line item now, not a discretionary upgrade.

Connected sensor networks and analytics layers are replacing legacy condition-monitoring technologies, such as manual rounds and isolated SCADA tags, that can identify bearing wear or corrosion weeks before breakdown. Utilities are using pilot programs that leverage private 5G and low-power wireless mesh networks to extend this visibility to substations and remote pump stations that were previously unmonitored. Several utility-led trials are reporting capital allocations in the tens of millions of dollars for plant-wide instrumentation refreshes. The Plant Asset Management Market is seeing a revolution in procurement cycles as the move from reactive to predictive maintenance models takes hold.

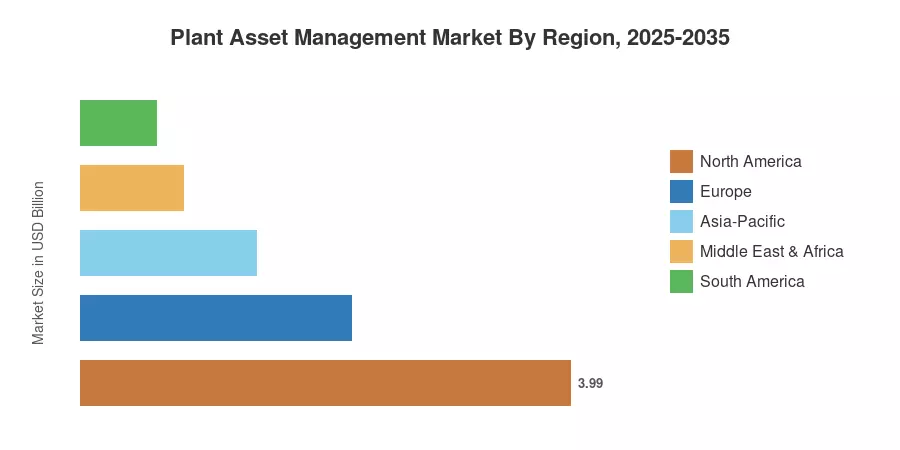

North America has the highest share of the Plant Asset Management Market at around 38.40%, owing to its established instrumentation infrastructure and strict environmental enforcement. The fastest growing region is Asia Pacific, which is rising at close to 13.78% CAGR as manufacturing expansion and government-backed digital factory efforts converge across China, India and South Korea. Europe ranks second, owing to industrial decarbonization requirements under the EU’s larger energy efficiency directives. Over the next 10 years, cloud-delivered platforms should begin to minimize these geographical differences by lowering the entrance barrier for mid-sized companies.

Key Report Takeaways

• By Technology

- Software solutions led the Plant Asset Management Market with a 47.20% revenue share in 2025.

- Cloud deployment models are expanding at a 14.09% CAGR through 2035, outpacing on-premise growth.

- Electrical assets accounted for 46.20% of total asset-type revenue in 2025.

• By Sector

- Oil and gas remained the leading end-user vertical in the Plant Asset Management Market with a 22.17% share in 2025.

- Mining and metals is the fastest-rising end-user segment, growing at a 13.08% CAGR.

- Large enterprises generated 68.21% of 2025 revenue, while smaller operators are catching up quickly.

• By Geography

- North America captured 38.40% of global revenue in 2025.

- Asia-Pacific is forecast to grow at 13.78% CAGR through 2035, the fastest of any region.

- Europe contributed an estimated USD 2.21 billion in 2025 revenue.

Market Size and Forecast (2021–2035)

Figures below represent a blend of primary interviews with plant reliability managers, secondary data from regulatory filings, and triangulation versus publicly announced vendor revenue. The historical years represent the actual reported spend, and the prospective years are modeled based on capital expenditure cycles and digitalization mandates tracked across the Plant Asset Management Market.