Polyvinyl Chloride Market Summary

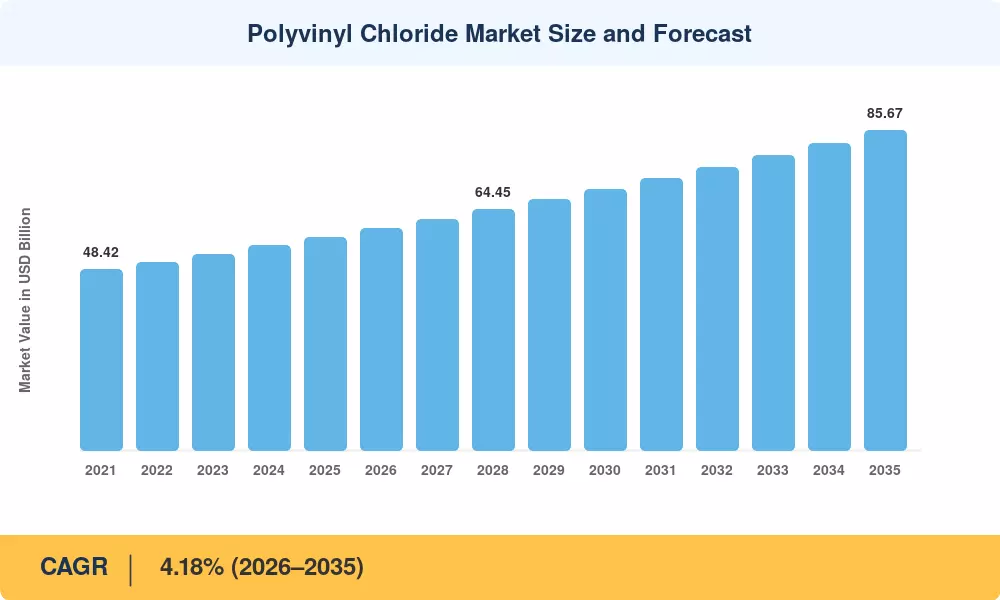

The Polyvinyl Chloride Market reached an estimated 57.05 million tons in 2025 and is projected to expand from 59.25 million tons in 2026 to 85.67 million tons by 2035, registering a CAGR of 4.18% across the forecast window. This trajectory reflects accelerating global investment in water infrastructure — the World Bank committed over USD 5.2 billion to water and sanitation projects in developing economies during 2024 alone [2] — alongside mounting demand for lightweight construction plastic products in green building initiatives. PVC resin materials remain the backbone of modern piping, cladding, and cable insulation supply chains, and their cost-to-performance ratio keeps vinyl polymer products ahead of most alternative thermoplastics in price-sensitive construction cycles.

A material transformation is underway within the Polyvinyl Chloride Market as legacy lead-based stabilizer systems phase out in favor of calcium-zinc and organotin formulations. The European Union's revised REACH Annex XVII restrictions, effective 2024, accelerated reformulation timelines across the bloc, while China's National Development and Reform Commission earmarked CNY 9.8 billion for chlor-alkali modernization under its 14th Five-Year Plan [3]. These shifts are pushing PVC manufacturing chemicals toward cleaner, more circular production pathways, including chemical recycling pilots that reclaim vinyl chloride monomer from post-consumer rigid PVC compounds.

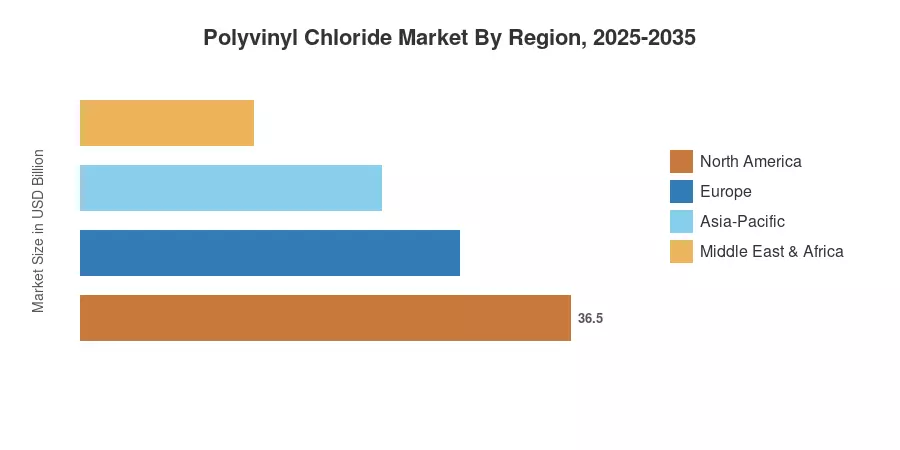

Asia-Pacific dominates the Polyvinyl Chloride Market with roughly 63.5% of 2025 consumption, propelled by India's Jal Jeevan Mission and Southeast Asia's urbanization wave. The region also posts the fastest CAGR at 4.53% through 2035. North America accounts for about 14.2% of global demand, anchored by U.S. residential construction and water-utility replacement cycles. Europe follows closely, driven by circular-economy regulations that favor thermoplastic polymer materials with established recycling infrastructure

Key Report Takeaways

• By Product Type

- Rigid PVC compounds commanded approximately 65.8% of the Polyvinyl Chloride Market share in 2025, driven by pipe and profile extrusion demand across emerging economies

- Chlorinated PVC is forecast to register the fastest segment CAGR of 4.90% to 2035, reflecting hot-water plumbing and industrial corrosion-resistance applications

• By Manufacturing Process

- Suspension PVC contributed roughly 79.5% of 2025 output volume in the Polyvinyl Chloride Market, owing to its versatility in both rigid and flexible formulations

- Emulsion PVC is poised to grow at a 4.72% CAGR through 2035 as paste-grade demand rises in automotive and textile coatings

• By Region

- Asia-Pacific accounted for 63.5% of the Polyvinyl Chloride Market in 2025, with China and India together consuming over 45% of global output

- North America's PVC resin materials demand is anchored by a 3.78% CAGR to 2035, supported by EPA lead-pipe replacement mandates worth USD 15 billion

Market Size and Forecast (2021–2035)

MRFR's market sizing combines top-down trade-flow analysis from UN Comtrade and ICIS with bottom-up capacity utilization data from over 120 PVC manufacturing facilities worldwide. Historical figures rely on audited production volumes; forecast values apply regression-adjusted demand elasticities calibrated to GDP growth, construction activity indices, and regulatory adoption curves.