Quartz Market Summary

The Quartz Market reached an estimated USD 9,850 million in 2025 and is projected to grow from USD 10,470 million in 2026 to approximately USD 18,150 million by 2035, registering a CAGR of 6.30% across the forecast period. Two forces are propelling this trajectory: semiconductor fabs pushing node geometries below 5 nm now demand crucible-grade feedstock with impurity thresholds measured in parts per billion, and global photovoltaic capacity additions—exceeding 350 GW annually since 2024—are consuming ever-larger volumes of solar-grade material [2][3].

A structural revolution is taking place in the way the mineral is moved from mine to finished product. Chlorination and plasma-assisted methods are replacing legacy acid-leach purification lines, and can attain 99.998% SiO 2 purity at commercial scale. In 2024, the U.S. Department of Energy granted USD 150 million to reduce the risk of domestic critical-mineral processing through the CHIPS and Science Act, while the European Critical Raw Materials Act declared silicon metal a strategic material, setting mandatory stockpiling targets across member states of the EU [4][5].

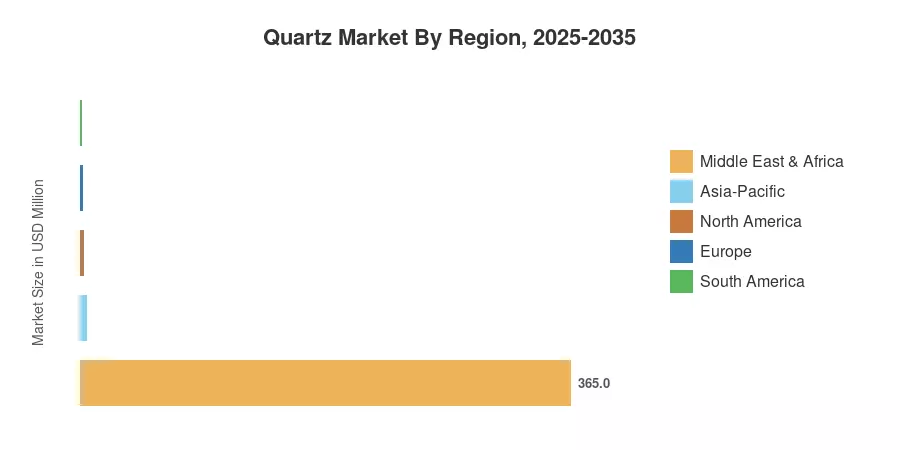

The Asia-Pacific region is estimated to account for 51% of the Quartz Market, with China dominating the silicon-metal smelting and Japan leading the semiconductor-grade fabrication segment. The region also has the fastest growth trajectory with a CAGR of 6.75% until 2035. North America is the No. 2 market at about 23%, aided by reshoring incentives and the concentration of sophisticated chip production in Arizona, Ohio and Texas. Europe is next with an 18% share, helped by the expansion of solar production and optical-fiber installations under EU broadband ambitions.

Key Quartz Market Report Takeaways

By Product Type

- Silicon metal accounted for approximately 91.0% of the global Quartz Market volume in 2025, reflecting its central role in metallurgical and chemical industries.

- The high-purity segment is advancing at a 7.75% CAGR through 2035, outpacing all other product categories as semiconductor and photovoltaic specifications tighten.

By End-User Industry

- Electronics and semiconductor end users represented roughly 37.2% of the Quartz Market value in 2025, driven by wafer-fabrication capacity build-outs across three continents.

- The solar segment is expanding at a 6.95% CAGR, supported by utility-scale installations and next-generation heterojunction cell production.

By Geography

- Asia-Pacific held approximately 51.2% of the global Quartz Market share in 2025, led by China, Japan, and South Korea.

- North America is the second-largest region, with USD 2,216 million in 2025 revenue and strong policy tailwinds from the CHIPS Act and Inflation Reduction Act.

Quartz Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a triangulating sizing technique that combines top-down revenue models with bottom-up consumption data from customs, trade groups, and corporate filings in 28 countries. Historical data are based on actual reported volumes; forecast estimates include demand side modeling for semiconductor, solar and construction verticals calibrated against announced capacity additions.