Railway Management System Market Summary

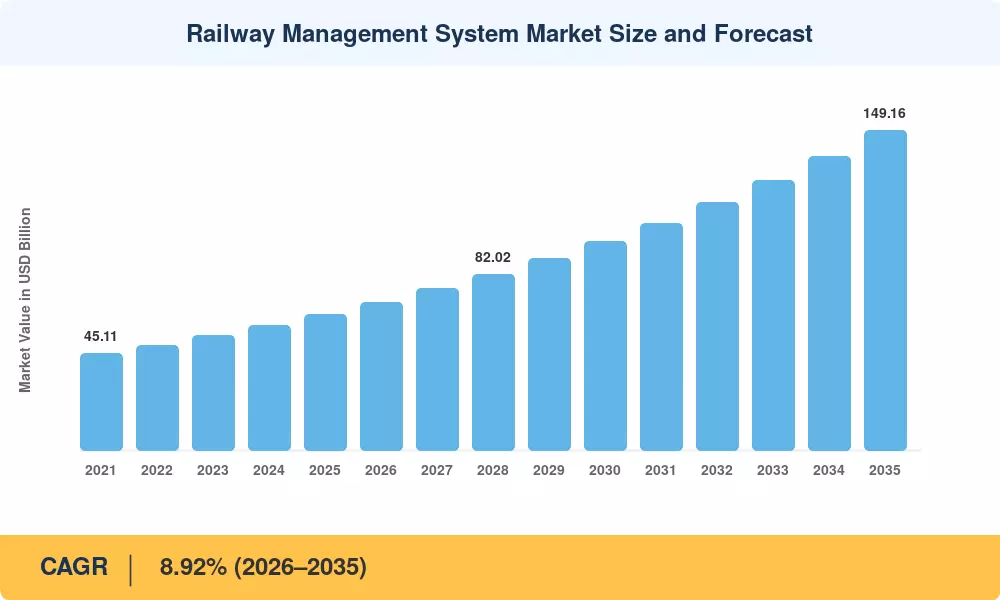

The Railway Management System Market reached an estimated USD 63.48 billion in 2025 and is projected to grow from USD 69.14 billion in 2026 to USD 149.16 billion by 2035, registering a CAGR of 8.92% during the forecast period. This trajectory is driven by sweeping government digitization mandates—most visibly the European Union's ERTMS Baseline 3 interoperability program—and sustained public-capital injections into rail network management infrastructure across North America and Asia [1]. Operators under pressure to cut lifecycle costs and meet decarbonization benchmarks are replacing siloed legacy architectures with integrated train operations software platforms that unify signaling, asset monitoring, and passenger information in a single control layer.

Cloud-native solutions for railway traffic control, AI-augmented predictive maintenance and real-time passenger rail management dashboards are replacing a generation of relay-based interlocking and paper-driven scheduling. The EU alone has committed more than EUR 26 billion for cross-border rail digitalization under the 2021–2027 Connecting Europe Facility, while India’s National Rail Plan aims for near-complete electrification by 2030—both enablers that expand the addressable envelope for train scheduling systems [2][3]. The momentum in the business sector is helping to strengthen these policy signals. Freight operators like Union Pacific are now opening up API ecosystems for third-party analytics, setting a precedent for outcome-based managed-service contracting across the Railway Management System Market.

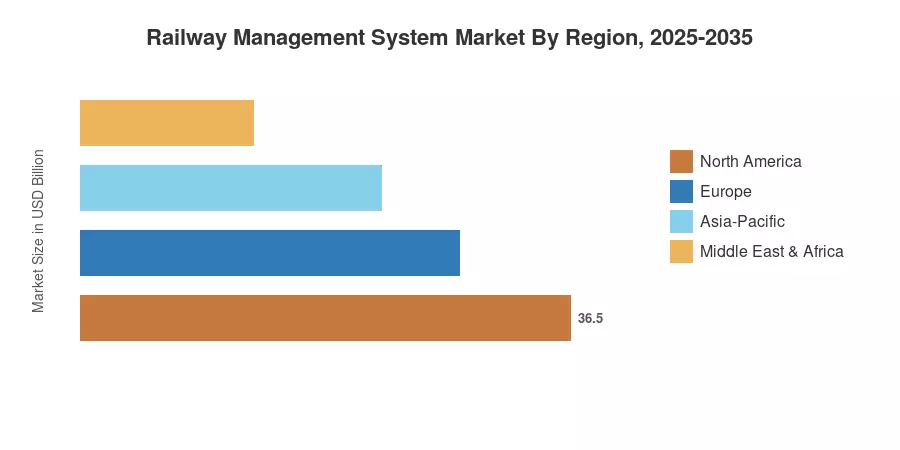

The Asia-Pacific area is expected to generate the highest revenue share in 2025, due to the implementation of high-speed rail in China, Japan and India, accounting for almost 42%. The region has the quickest anticipated CAGR above 10%. It is not only the volume leader but also the growth engine for the Railway Management System Market. Europe is the second largest market with approximately 22% market share, driven by ERTMS compliance expenditure. North America has approximately 26% market share, driven by US federal infrastructure financing. This will expand the value frontier significantly, as rail network management platforms will be moved into the space of adjacent workloads like energy optimization, cybersecurity orchestration and autonomous operations over the next decade.

Key Report Takeaways

• By Component

- Solutions held a 74.2% share of the Railway Management System Market in 2025, reflecting operators' preference for integrated train operations software suites over piecemeal point products.

- Managed services are on track for the fastest segment CAGR of approximately 10.6% through 2035, as rail authorities shift to outcome-based contracting for rail network management.

• By Rail Type

- Passenger rail captured a 58.1% revenue share in 2025, propelled by urbanization-driven mass transit expansions and government subsidies for passenger rail management modernization.

- Freight rail platforms are accelerating, with telematics-led visibility initiatives powering the Railway Management System Market expansion in intermodal logistics corridors.

• By Geography

- Asia-Pacific led the Railway Management System Market with the highest absolute revenue and fastest regional CAGR, driven by China's CRSC-led train scheduling systems deployments.

- North America recorded a 26% share in 2025, underpinned by the US Bipartisan Infrastructure Law's rail-safety allocations for railway traffic control upgrades.

- Europe's ERTMS rollouts and Green Deal freight mandates positioned the region as the second-largest market for rail network management solutions.

Market Size and Forecast (2021–2035)

Market Research Future forecasts are based on a combination of bottom-up revenue modeling, primary interviews with train operators and system integrators and cross-validated against public procurement databases, regulatory filings and industry organization statistics. Historical data are actual vendor revenues. Forecast values are derived using the calibrated compound annual growth rate applied to the base-year estimate.