Recombinant Vaccines Market Summary

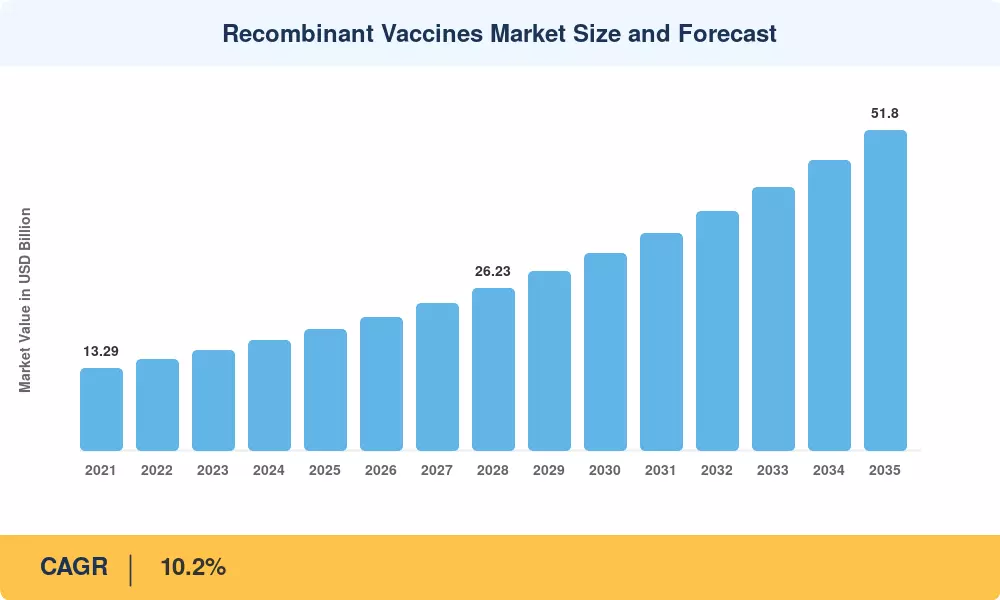

The Global Recombinant Vaccines Market size was valued at USD 19.6 Billion in 2025, and the market is projected to grow from USD 21.6 Billion in 2026 to USD 51.8 Billion by 2035, registering a CAGR of 10.2% during the forecast period 2026–2035. Two catalysts anchor that trajectory: mandatory HPV vaccination schedules now active in more than 130 countries, and sustained pandemic-preparedness allocations — including CEPI's USD 3.5 billion pledge for 100-day vaccine response capabilities — that keep manufacturing capacity utilization elevated across every major production platform [1][2].

A measurable shift away from legacy egg-based manufacturing continues to reshape the Recombinant Vaccines Market. Precision synthetic-biology workflows, single-use bioreactors, and AI-guided antigen design compress development timelines from years to months. Governments reinforced this transition with over USD 12 billion in combined Operation Warp Speed and EU HERA commitments between 2021 and 2024, catalyzing private-sector investment in mRNA, protein-subunit, and virus-like-particle platforms [3][4].

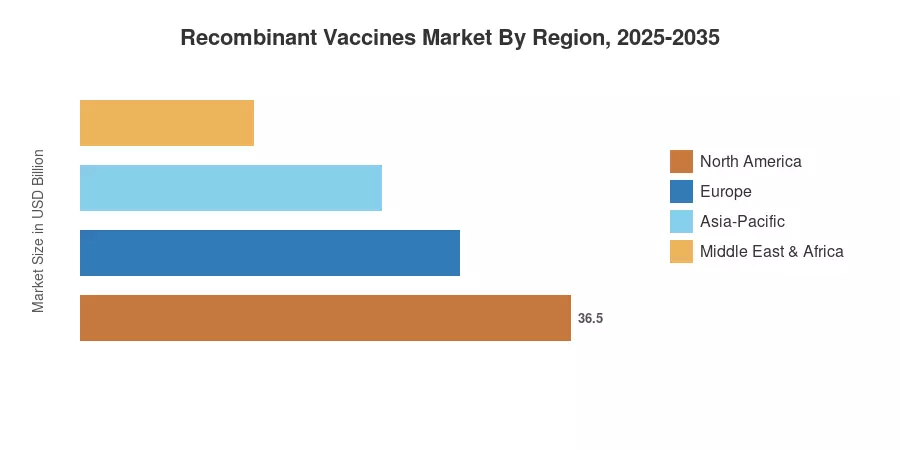

North America commanded roughly 33.2% of the Recombinant Vaccines Market in 2024, driven by deep reimbursement coverage and FDA fast-track pathways. Asia-Pacific is the fastest-growing region at a projected 10.3% CAGR through 2035, buoyed by India's and China's expanding domestic biomanufacturing capacity. Europe held the second-largest share at approximately 27%, supported by EMA harmonization of accelerated-assessment routes for novel biological products. The next decade will hinge on how quickly low- and middle-income nations scale adult catch-up programs and thermostable formulations that reduce cold-chain dependence.

Key Report Takeaways

• By Technology Type

- Protein-subunit products captured the leading revenue share in 2024, reflecting mature supply chains for hepatitis B and HPV antigens.

- mRNA platforms are forecast to register the fastest expansion through 2035, riding on rapid iteration advantages demonstrated during the COVID-19 pandemic.

• By Disease Indication

- HPV vaccines represented the dominant share of the Recombinant Vaccines Market in 2024, supported by school-based mandates across OECD nations.

- Dengue indications are accelerating at a double-digit CAGR, with Sanofi's Dengvaxia and Takeda's TAK-003 broadening endemic-market access.

• By Region

- North America led global sales, anchored by the US CDC immunization schedule and robust payer coverage.

- Asia-Pacific's growth outpaces all other regions in the Recombinant Vaccines Market, propelled by Gavi co-financing and local manufacturing scale-up in India, China, and Indonesia.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down revenue estimates from manufacturer disclosures, WHO procurement databases, and national immunization-program budgets against bottom-up per-dose pricing and volume models across 45 countries. Historical values (2021–2024) are validated against audited annual reports; forecast values (2026–2035) apply a calibrated 10.2% CAGR adjusted for anticipated regulatory approvals, pipeline readouts, and manufacturing capacity additions.