Recycled Plastic Granules Market Summary

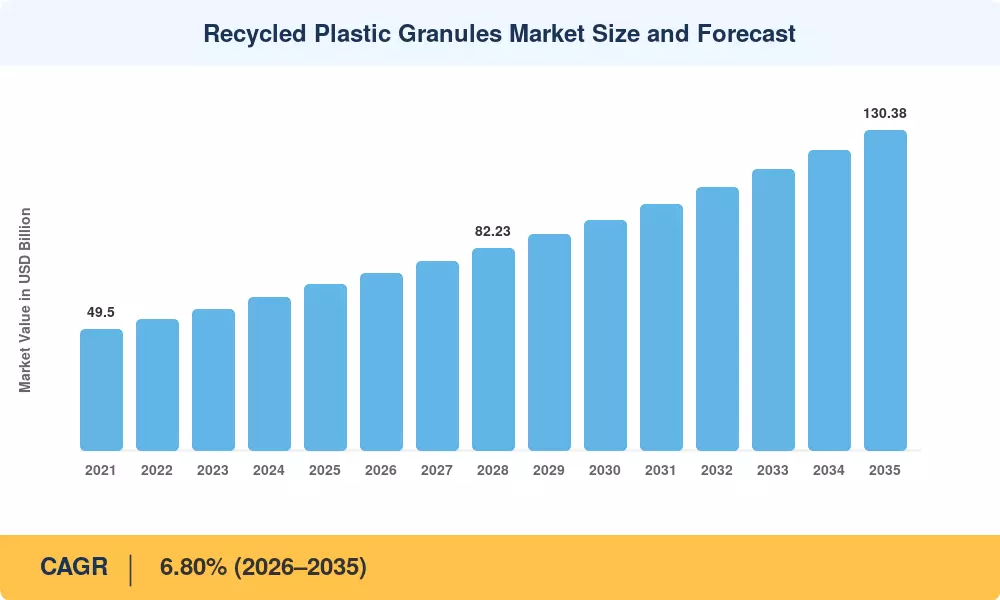

The recycled plastic granules market reached an estimated USD 67.50 billion in 2025, with the forecast period beginning at USD 72.09 billion in 2026 and climbing to USD 130.38 billion by 2035 at a compound annual growth rate (CAGR) of 6.80%. Two catalysts anchor this trajectory: the European Union's Packaging and Packaging Waste Regulation (PPWR), which enforces minimum recycled content thresholds across plastic packaging categories starting in 2026, and the rapid expansion of Extended Producer Responsibility (EPR) frameworks across Southeast Asia [2]. Brand owners across consumer goods, automotive, and electronics have moved from voluntary pledges to binding procurement commitments, creating a structural demand floor for recycled plastic granule market participants.

The technology revolution is changing the supply side of the recycled plastic granules industry. Near-infrared (NIR) and AI-driven sorting systems are being added to legacy mechanical sorting lines that have long been hampered by contamination and color limits, driving food-grade yield rates above 85% [3]. Commercial-timeline facilities for enzymatic PET depolymerization guarantee virgin-equivalent production from mixed color bales. Chemical recycling capital spending across stated projects exceeded USD 8.5 billion globally through 2024 [4], suggesting investor confidence in feedstock diversification beyond mechanical processing.

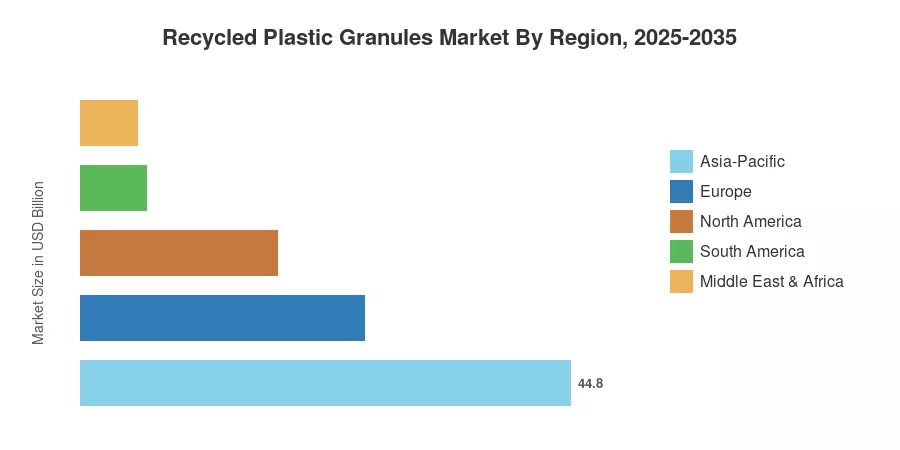

The Asia-Pacific region represents around 44.8% of the recycled plastic granules market, owing to the statewide garbage sorting laws in China and the growing collection infrastructure in India. Europe has the second-highest stake at around 26.0%, driven by PPWR mandates and deposit-return scheme expansions. The third largest region is North America at 18.0%, with U.S. EPA recycling infrastructure funds allowing expansion of processing capacity [5]. Circular economy legislation tightening across the globe during the projected window will see the recycled plastic granules market see amplified demand.

Key Report Takeaways

• By Polymer Type

- Polyethylene accounted for 31.5% of the recycled plastic granules market share in 2025, reflecting its dominance in flexible packaging and agricultural film recovery.

- The "Others" polymer segment (including polypropylene, polystyrene, and engineering resins) is projected to grow at an 8.4% CAGR through 2035, fueled by automotive lightweighting programs.

• By the Recycling Process

- Mechanical recycling held 76.2% of processing volume in 2025, remaining the cost-effective backbone of the recycled plastic granules market.

- Chemical and advanced recycling is projected to expand at a 9.4% CAGR through 2035 as pyrolysis and depolymerization plants scale.

• By Product Form

- Flakes captured 70.8% of market volume in 2025, serving as the primary intermediate feedstock.

- Pellets represent the fastest-growing product form at a 8.5% CAGR, driven by converter demand for drop-in replacements.

• By End-Use Application

- Packaging held 42.0% of the market share in 2025, anchored by mandatory content regulations.

- Automotive applications are projected to grow at 11.0% CAGR through 2035 as OEM circularity targets expand.

• By Geography

- Asia-Pacific commanded 44.8% of the recycled plastic granules market in 2025.

- Europe held approximately 26.0% share, led by regulatory mandates and mature collection systems.

Market Size and Forecast (2021–2035)

MRFR’s predictions are based on personal interviews with over 120 industry participants, trade association data, regulatory filings, and proprietary demand modeling calibrated against historical shipment volumes and capacity announcements.