Refrigeration Coolers Market Summary

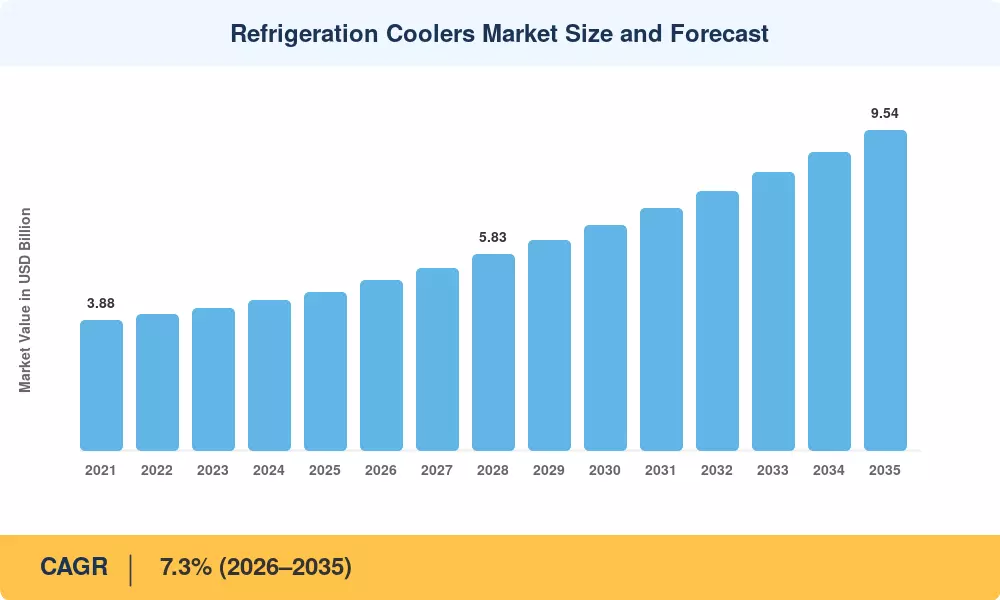

The Refrigeration Coolers Market reached an estimated USD 4.72 Billion in 2025 and is projected to grow from USD 5.06 Billion in 2026 to USD 9.54 Billion by 2035, registering a CAGR of 7.3% during the forecast period. This expansion is anchored in tightening HFC phase-down regulations under the Kigali Amendment and massive reinvestment cycles across commercial food retail and pharmaceutical cold chain infrastructure. Governments in over 140 signatory countries are enforcing accelerated timelines for high-GWP refrigerant elimination, compressing upgrade windows that once stretched over a decade into three-to-five-year replacement mandates [1][2].

A significant technology shift is reshaping the Refrigeration Coolers Market as legacy direct-expansion HFC systems give way to transcritical CO₂ racks, ammonia-based industrial platforms, and inverter-driven compressor architectures. The European Commission's revised F-gas Regulation, which entered force in 2024, imposes a 95% HFC quota reduction by 2030, channeling an estimated EUR 8.4 Billion in cumulative equipment spending toward compliant alternatives across EU-27 member states [3][4]. Parallel to policy pressure, connected IoT monitoring and AI-driven predictive maintenance are lowering lifecycle operating costs by 12–18%, making new system adoption economically attractive even absent regulatory mandates.

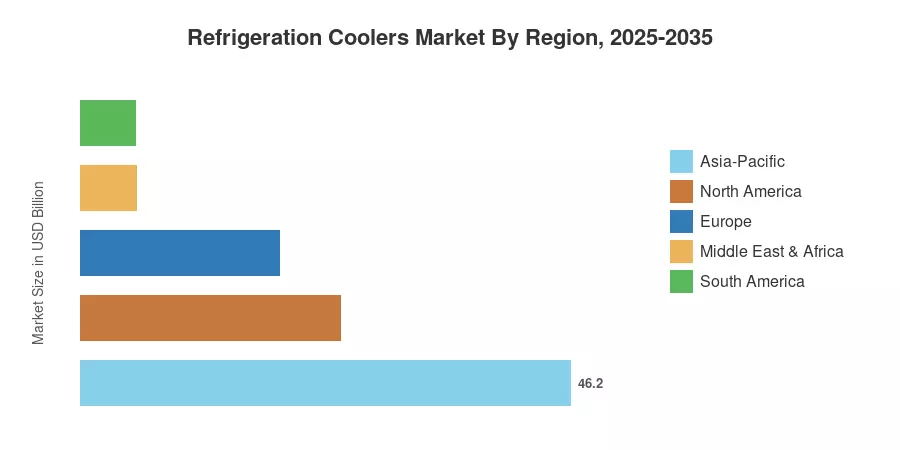

Asia-Pacific commands the largest share of the Refrigeration Coolers Market at approximately 46.2% of global revenue, driven by China's cold chain build-out and India's FSSAI-mandated perishable logistics upgrades. The region also represents the fastest-growing geography at an estimated 8.1% CAGR through 2035. North America holds the second-largest position with roughly a 24.5% share, buoyed by the AIM Act and EPA rulemakings accelerating HFC step-downs. Europe captures around 18.8% share as stringent F-gas timelines push adoption faster than any other developed market. The decade ahead will reward manufacturers who pair natural-refrigerant hardware with digital controls and service platforms.

Key Report Takeaways

• By Product Type

- Evaporators and air coolers held approximately a 38.7% share of the Refrigeration Coolers Market in 2025, reflecting their centrality in commercial display and walk-in applications.

- Magnetic cooling modules are forecast to expand at a 7.3% CAGR through 2035, positioning solid-state thermal management as the segment's highest-growth frontier.

• By Refrigerant Type

- Ammonia-based systems accounted for roughly 31.2% of the Refrigeration Coolers Market in 2025, remaining the industrial workhorse for large-scale cold storage and processing.

- Carbon dioxide (CO₂) refrigerant platforms are projected to grow at a 7.5% CAGR, driven by regulatory preference and falling component costs.

• By End-User Industry

- Cold-storage and logistics operators represented an estimated 35.9% of the Refrigeration Coolers Market in 2025, outpacing all other verticals.

- Data centers and electronics cooling are forecast to register a 7.6% CAGR through 2035 as chip thermal loads intensify.

• By System Type

- Centralized rack systems commanded roughly a 43.8% share in 2025 across the Refrigeration Coolers Market.

- Hybrid and transcritical CO₂ systems are projected to grow at a 7.3% CAGR as retailers migrate from HFC racks.

• By Region

- Asia-Pacific accounted for approximately 46.2% of the Refrigeration Coolers Market in 2025 and leads all regions in absolute capacity additions.

- North America held the second-largest share at 24.5%, with the U.S. AIM Act driving accelerated replacement cycles.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up equipment shipment tracking across 32 countries with top-down cross-validation against publicly reported refrigeration component revenues, trade data from UN Comtrade, and regulatory compliance filings. Historical figures (2021–2024) reflect actual shipments; the 2025 base year blends preliminary shipment data with manufacturer guidance; and the 2026–2035 forecast applies a calibrated 7.3% CAGR adjusted for policy-driven acceleration phases.