Robot-Assisted Surgical Systems Market Summary

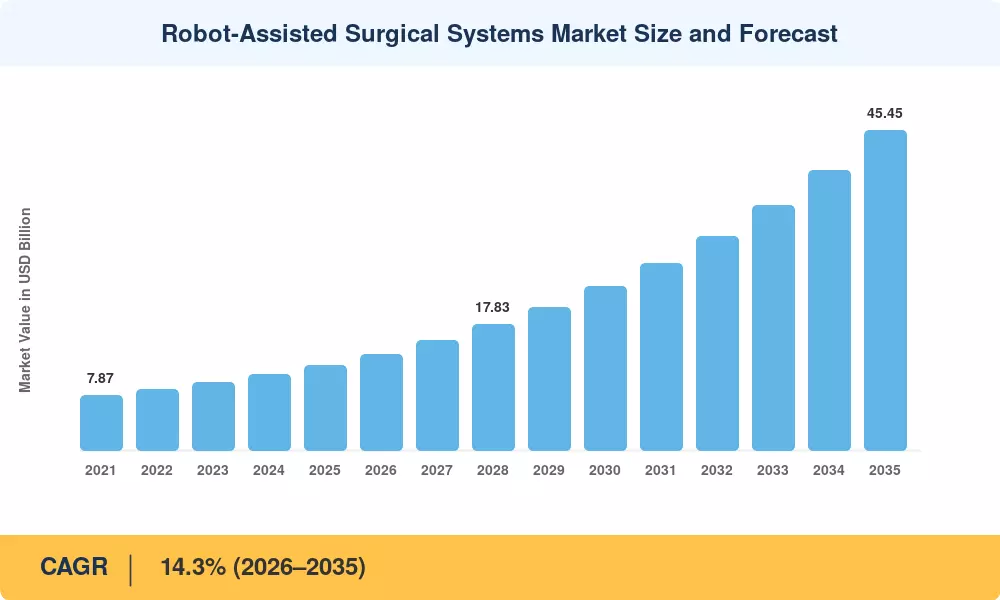

The Global Robot-Assisted Surgical Systems Market size was valued at USD 12.04 Billion in 2025, and the market is projected to grow from USD 13.65 Billion in 2026 to USD 45.45 Billion by 2035, registering a CAGR of 14.3% during the forecast period 2026–2035. Accelerating adoption of outpatient procedure mandates — including the U.S. Centers for Medicare & Medicaid Services (CMS) 2024 rule broadening ambulatory surgery reimbursement codes — has anchored institutional capital expenditure in robotic platforms [1]. Hospitals now justify seven-figure system acquisitions by demonstrating shorter average lengths of stay and measurable reductions in surgical-site infections, which third-party payers increasingly recognize in value-based contracts [2].

Robot-Assisted Surgical Systems: A Technological Revolution. The market focuses on the transition from independent electromechanical platforms to cloud-based, AI-enhanced ecosystems. Multi-port and single-port robotic consoles with real-time tissue analytics capabilities are replacing outdated open-surgery equipment. Within a year of its release, the top five vendors committed an estimated USD 1.2 billion in additional R&D thanks to a 2024 FDA three-tier autonomy framework that established the regulatory approach for AI-enabled decision support during procedures [3].

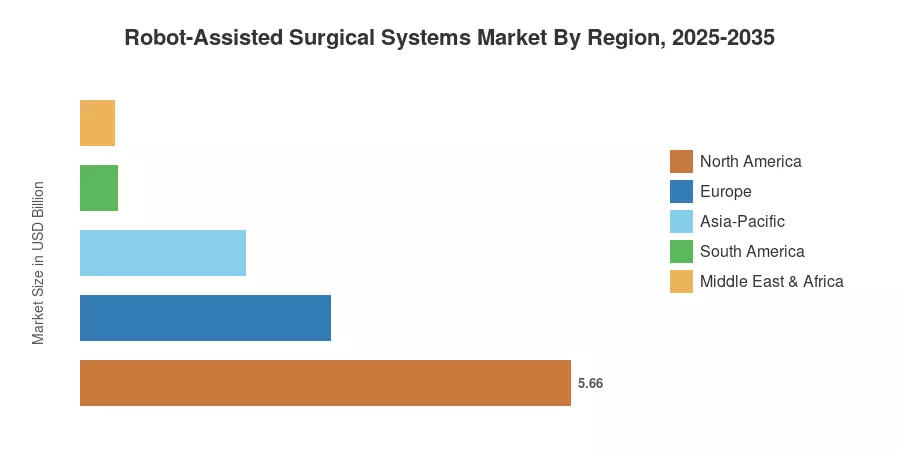

Due to favorable payer mixes and dense installed bases, North America accounted for about 47% of worldwide revenue in 2025. With a predicted 15.9% CAGR, Asia-Pacific is the fastest-growing area thanks to cost-competitive domestic manufacturers that undercut Western incumbent pricing by 30–40% [4]. Europe came in second, accounting for about 24% of the world's total value. The trajectory of the robot-assisted surgical systems market is expected to accelerate through the mid-2030s as digital surgery infrastructure develops and operation volumes rise in emerging economies.

Key Report Takeaways

• By Product Type

- Systems captured approximately 62% of the Robot-Assisted Surgical Systems Market in 2025, reflecting the capital-intensive nature of platform deployments across hospitals and specialty centers.

- Software & Services is forecast to grow at a 17.1% CAGR through 2035, signaling a decisive pivot toward subscription-based digital revenue models.

• By Application

- Gynecological surgery represented roughly 28% of the Robot-Assisted Surgical Systems Market share in 2025, driven by high procedural volumes and favorable clinical evidence.

- Neurosurgery is projected to register a 17.5% CAGR through 2035 as stereotactic integration and image-guided navigation expand clinical use cases.

• By End User

- Hospitals held an estimated 49% of the Robot-Assisted Surgical Systems Market in 2025, supported by centralized procurement budgets and multi-specialty case mixes.

- Ambulatory surgery centers are expected to advance at a 17.9% CAGR to 2035, catalyzed by payer incentives for outpatient migration.

• By Regional

- North America contributed about 47% of global revenue in 2025, underpinned by mature reimbursement frameworks and an installed base exceeding 5,400 systems.

- Asia-Pacific is set to grow at a 15.9% CAGR, with domestic manufacturers in China and India capturing share through aggressive pricing and localized service networks.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down revenue estimates from public filings, procedure-volume databases, and proprietary surveys of 320+ healthcare procurement officers across 18 countries. Historical figures (2021–2024) rely on audited company disclosures, while forward projections apply a weighted multi-factor model incorporating reimbursement trends, regulatory clearances, and capital-cycle replacement curves.