Satellite Antenna Market Summary

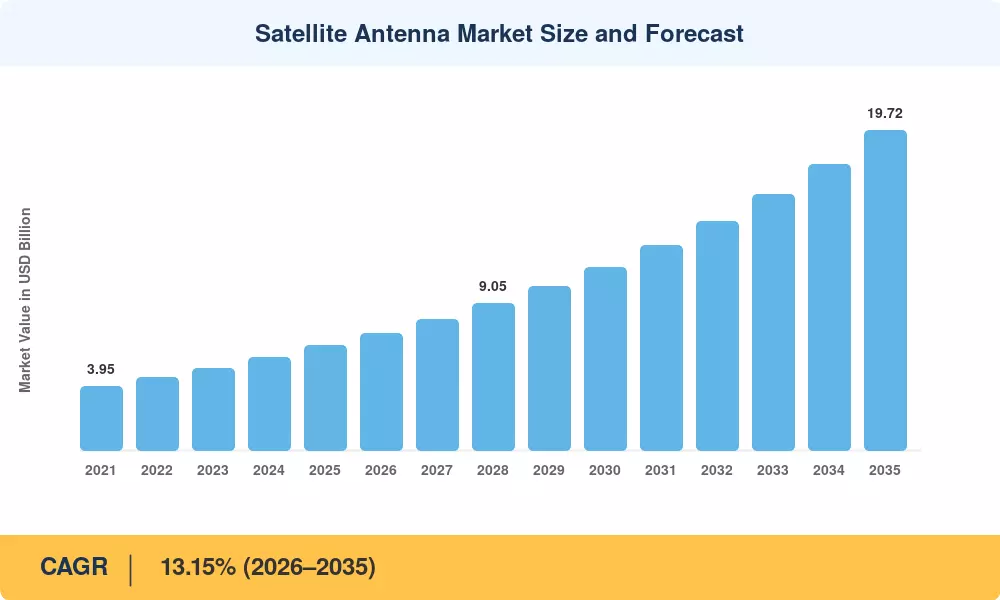

The Satellite Antenna Market was valued at USD 6.48 billion in 2025 and is projected to reach USD 7.50 billion in 2026 before climbing to USD 19.72 billion by 2035, registering a CAGR of 13.15% during 2026–2035. This acceleration is rooted in the rapid deployment of low-Earth-orbit broadband constellations — SpaceX alone has committed over USD 10 billion to Starlink infrastructure — and the parallel surge in defense procurement for multi-orbit terminal resilience[2]. The US Department of Defense's FY2025 space budget of USD 33.3 billion earmarks significant funding for protected tactical satellite terminals, reinforcing commercial and military demand simultaneously [3].

The satellite antenna market is undergoing a radical technology revolution. Legacy parabolic dish satellite terminals have traditionally chosen C-band and Ku-band reception. Still, they are being displaced by phased array flat panel satellite antenna systems using electronically steered arrays (ESAs). Automotive-scale manufacturing partnerships have driven flat-panel unit prices down by about 40% since 2021, making VSAT very small aperture terminal deployments commercially viable for maritime fleets, rural broadband and in-flight connectivity [4][5]. Another validation of this movement is the European Union’s IRIS² sovereign connectivity program, financed by EUR 6 billion in public-private funding [6], toward LEO satellite terminal antenna topologies.

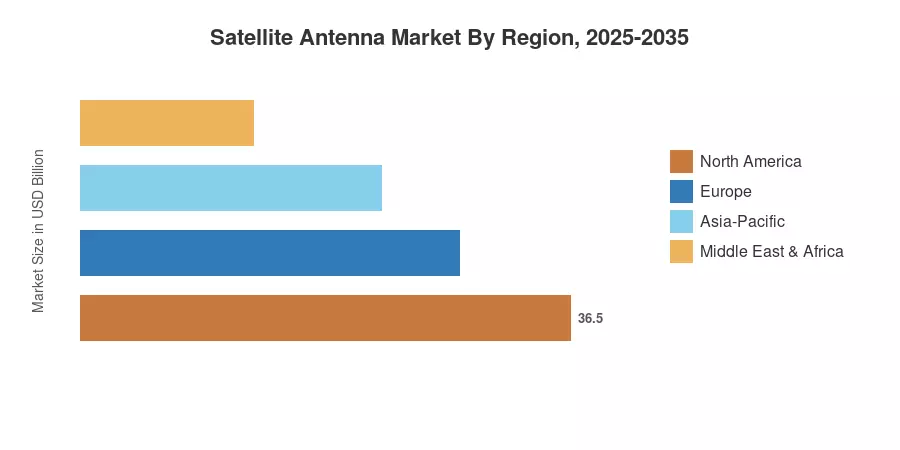

North America is expected to contribute around 44% to the revenue share of the 2025 Satellite Antenna Market, owing to the defense expenditure, adoption of Starlink dish flat antenna and enterprise VSAT infrastructure. Asia-Pacific is the fastest expanding area with a projected CAGR of 10.6%, supported by India’s satellite broadband licensing reforms and China’s Guowang mega-constellation plans. Europe is the second largest region with a share of about 26% supported by IRIS² procurement cycles and marine VSAT antenna steady demand from the North Sea shipping corridor [7][8]. The next decade will be a race to develop flat-panel ESA production fast enough to match LEO constellation capacity.

Key Report Takeaways

• By Frequency Band

- C Band accounted for approximately 41% of the Satellite Antenna Market in 2025, reflecting its dominance in broadcast and telemetry backhaul.

- Ka Band is emerging as the highest-growth segment

• By Antenna Type

- Flat-panel ESA/RSA designs are advancing at a 36.8% CAGR through 2035, displacing legacy parabolic reflector antennas in commercial aviation and maritime VSAT antenna stabilized platforms

- Parabolic dish satellite reflectors still represent USD 2.87 billion in 2025 revenue, sustained by ground station upgrades in the C and Ku band spectrum

• By Application

- Land-based platforms held 39% share of the Satellite Antenna Market in 2025, led by VSAT very small aperture terminal hubs and Starlink dish flat antenna consumer installations

- Airborne platforms are set to grow at a 13.7% CAGR to 2035, propelled by airline mandates for Ka-band in-flight connectivity

• By Geography

- North America retained the dominant position in the Satellite Antenna Market, representing approximately 44% of 2025 revenue

- Asia-Pacific is forecast to register a 10.6% CAGR through 2035, with India and China as primary growth engines

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)’s patented estimation framework integrates bottom-up revenue modeling from manufacturer shipment data, operator CapEx disclosures, and government procurement records with top-down validation through trade association statistics and spectrum auction databases. All values are in USD Billion at constant 2025 exchange rates.