Shampoo Market Summary

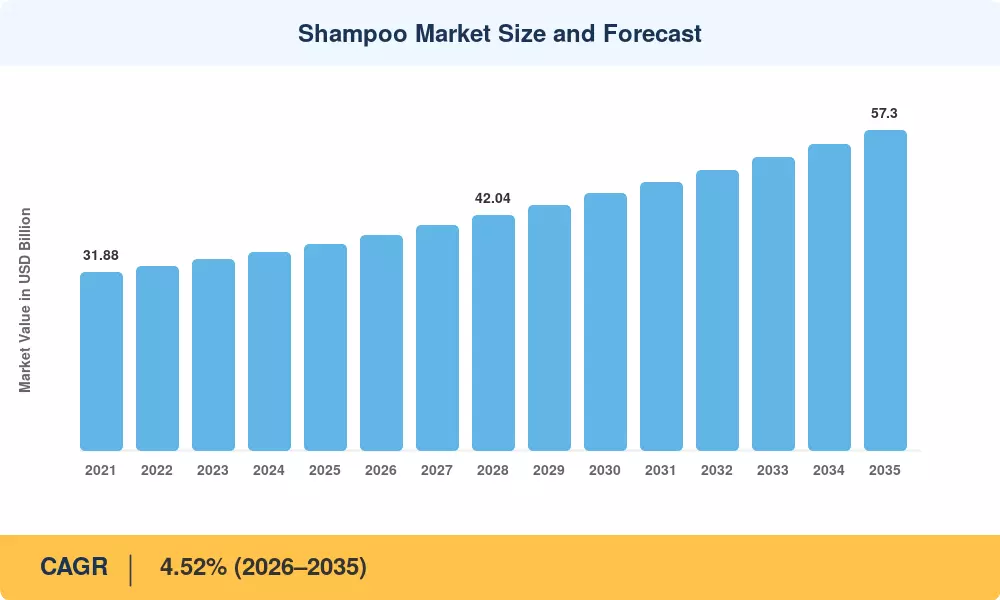

The global Shampoo Market reached an estimated USD 36.82 billion in 2025 and is projected to grow from USD 38.48 billion in 2026 to USD 57.30 billion by 2035, registering a CAGR of 4.52% during the forecast period (2026–2035). This expansion is anchored in two reinforcing catalysts: the premiumization wave sweeping personal care aisles worldwide and regulatory tightening around cosmetic ingredient transparency. The U.S. FDA's Modernization of Cosmetics Regulation Act (MoCRA), signed into law in December 2022, has compelled manufacturers to reformulate products and invest in safety substantiation — creating a compliance-driven upgrade cycle worth an estimated USD 2.4 billion in cumulative R&D redirects through 2030 [1].

A structural transformation is reshaping how consumers select and purchase shampoos. Legacy one-size-fits-all formulations are yielding to targeted, concern-specific products — anti-dandruff, volumizing, bond-repair, and scalp-health variants — powered by biotechnology-derived actives and clinical-grade ingredient transparency. Direct-to-consumer brands have captured roughly 12% of online hair-care sales in North America, forcing legacy FMCG companies to accelerate digital shelf investments [2]. The Shampoo Market is also witnessing a packaging revolution, with refill-station pilots from major brands reducing single-use plastic volumes by an estimated 30% per SKU rotation cycle [3].

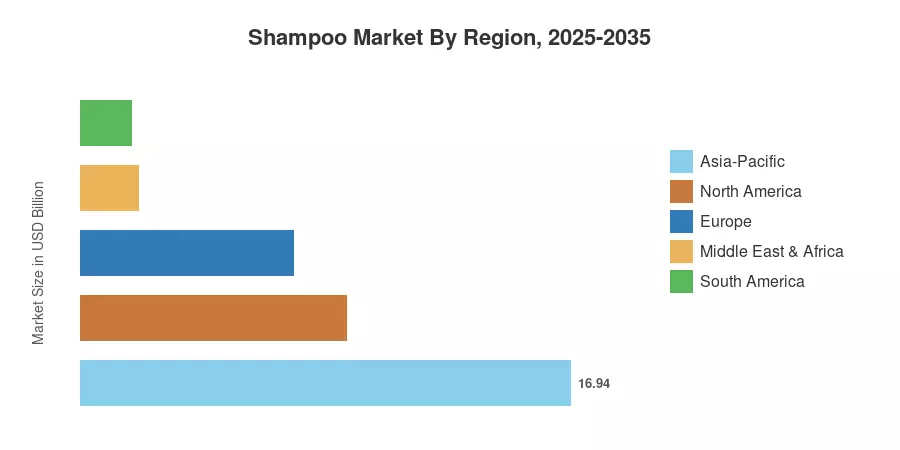

Asia-Pacific dominates the Shampoo Market with approximately 46% of global revenue in 2025, propelled by sachet-driven mass consumption across India and Southeast Asia alongside premiumization in China, Japan, and South Korea. The region also posts the fastest CAGR at roughly 5.1% through 2035, outpacing the global average. North America holds the second-largest share at about 25%, driven by clinical-performance positioning and salon-to-retail brand migration. Europe, contributing around 20%, remains the regulatory pacesetter — the EU Cosmetics Regulation (EC No 1223/2009) continues to set global ingredient-safety benchmarks that ripple through formulation strategies worldwide [4]. As scalp-health awareness deepens and water-conscious formats gain traction, the Shampoo Market is poised for sustained, innovation-led growth through the next decade.

Key Report Takeaways

• By Product Type

- Specific-purpose shampoos (anti-dandruff, volumizing, damage repair) hold a combined 54% share of the Shampoo Market in 2025, reflecting consumers' shift toward targeted hair-care solutions.

- Natural and organic formulations are expanding at the fastest CAGR of approximately 6.4% (2026–2035), driven by clean-beauty mandates and ingredient transparency.

- The 2-in-1 segment generated approximately USD 5.30 billion in 2025 as time-pressed consumers favor multifunctional products.

• By Distribution Channel

- Supermarkets and hypermarkets retain the dominant distribution share at roughly 35% of Shampoo Market revenue, leveraging in-store promotions and impulse purchasing.

- Online retail channels register a projected CAGR of 6.1% through 2035, accelerated by social commerce, subscription boxes, and virtual try-on tools.

• By Region

- Asia-Pacific commands approximately 46% of the global Shampoo Market, with China alone contributing roughly 33% of regional sales.

- Middle East & Africa, while small in absolute terms, posts a regional CAGR of approximately 5.4%, fueled by urbanization and a youthful demographic profile.

- North America accounts for about USD 9.20 billion in 2025 Shampoo Market revenue, anchored by clinical-performance brand positioning.

Shampoo Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining top-down revenue estimates from publicly reported FMCG earnings, bottom-up retail audit data across 45+ countries, and trade-flow analysis for cross-border e-commerce channels. Historical figures (2021–2024) reflect audited data; the 2025 base year incorporates preliminary earnings releases and channel-check estimates. Forecast projections apply a compound-growth model adjusted for macroeconomic elasticity, regulatory impact overlays, and category penetration curves.