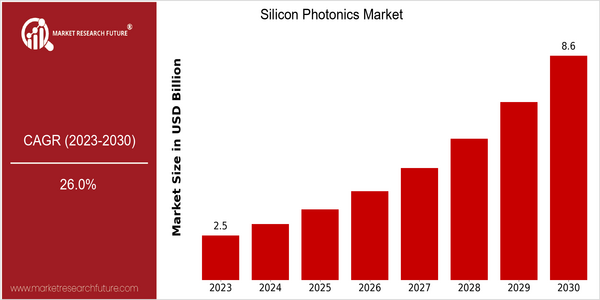

Silicon Photonics Size

Market Size Snapshot

| Year | Value |

|---|---|

| 2023 | USD 2.5 Billion |

| 2030 | USD 8.6 Billion |

| CAGR (2023-2030) | 26.0 % |

Note – Market size depicts the revenue generated over the financial year

The silicon photonics market is expected to grow rapidly in the future. The current market size is estimated to be $2.5 billion in 2023, and is projected to reach $86 billion by the year 2030. This significant growth shows a CAGR of 26%. The main driving force is the increasing demand for high-speed data transmission and the need for more energy-efficient data centers. The development of digital industries and the demand for high-speed data transmission are also becoming more and more important, and the industry is in urgent need of a new generation of silicon photonics. The advantages of silicon photonics, such as the integration of photonics and electronics, have become more and more obvious, and silicon photonics has become the first choice for the industry in telecommunications, data centers, and consumer electronics. , etc. The big companies in this field, such as Intel, Cisco, and IBM, are also investing in R & D, establishing strategic alliances, and launching new products to seize the market. These activities not only show the potential of silicon photonics, but also highlight the fierce competition in the industry.

Regional Market Size

Regional Deep Dive

The silicon photonics market is experiencing significant growth across the globe, driven by advancements in data communication, high-performance computing and the increasing demand for energy-efficient solutions. North America is currently the world’s leading innovation and investment hub, with strong representation from leading companies and research institutions. Europe is focusing on regulatory issues and on issues of sustainability, while Asia-Pacific is deploying silicon photonics technology in telecommunications and in the consumer electronics sector. The Middle East and Africa are gradually developing as potential markets with growing interest in adopting the technology. Latin America is still in its infancy, but its tech hubs are developing.

Europe

- The European Union has launched initiatives like the Horizon Europe program, which funds research in silicon photonics, emphasizing sustainability and energy efficiency in technology.

- Companies like STMicroelectronics are advancing silicon photonics integration in consumer electronics, which is expected to enhance product performance and reduce costs.

Asia Pacific

- China is rapidly expanding its silicon photonics capabilities, with government support for research and development, particularly in telecommunications and data centers.

- Japanese firms, such as Fujitsu, are innovating in silicon photonics for high-speed optical communication, which is crucial for the country's advanced telecommunications infrastructure.

Latin America

- Brazil is beginning to see investments in silicon photonics research, particularly in academic institutions, which could lead to future commercialization of technologies.

- Emerging tech hubs in countries like Chile and Argentina are starting to explore silicon photonics applications, driven by a growing interest in telecommunications and data processing.

North America

- The United States is home to major companies like Intel and Cisco, which are heavily investing in silicon photonics research and development, leading to breakthroughs in data center technologies.

- Recent collaborations between universities and tech firms, such as the partnership between MIT and various startups, are fostering innovation in silicon photonics applications, particularly in AI and machine learning.

Middle East And Africa

- The UAE is investing in smart city initiatives that incorporate silicon photonics technologies, aiming to enhance communication infrastructure and data management.

- Israel's tech ecosystem is fostering startups focused on silicon photonics, with government support for innovation and technology transfer, which is expected to boost local market growth.

Did You Know?

“Silicon photonics can potentially reduce the energy consumption of data centers by up to 90% compared to traditional electronic interconnects.” — International Energy Agency (IEA)

Segmental Market Size

The silicon photonics market is experiencing rapid growth, driven by the need for fast data transmission and energy-efficient solutions in data centers and telecommunications. The growth in data traffic, the rise of the cloud, the development of the Internet of Things and the improvement in silicon photonics technology are the main driving forces for the growth of this market. Intel and Cisco are at the forefront in implementing silicon photonics in their products to meet these demands. The current deployment of silicon photonics is in the process of taking off, with the main projects in North America and Europe where the technology giants are implementing these solutions. In addition to data center interconnection, the main applications are optical communications and sensors. The main products are 100G optical transceivers from Intel. The momentum of this market is further enhanced by macro trends such as the drive for sustainable development and government initiatives to promote green technology. The further development of manufacturing processes and integration technology will also shape the future development of this market.

Future Outlook

The silicon photonics market will experience a substantial growth from 2023 to 2030. The market value is expected to increase from $2.5 billion to $8.5 billion, resulting in a CAGR of 26%. The market is driven by the growing demand for high-speed data transmission and the need for energy-efficient solutions in data centers and telecommunications. The digitalization of industry will continue to accelerate, and the penetration of silicon photonics in various sectors such as telecommunications, data centers, and consumer electronics will increase to more than 30% in these areas by 2030. Several technological advances, such as the integration of silicon photonics with existing semiconductor technology, are expected to increase the performance and reduce the cost of the product, thus accelerating the market penetration. Also, government support for innovation in photonics and increased R&D spending will play a significant role in the market. The growth of artificial intelligence and machine learning, which requires high speed and low latency, will also boost the market.

Leave a Comment