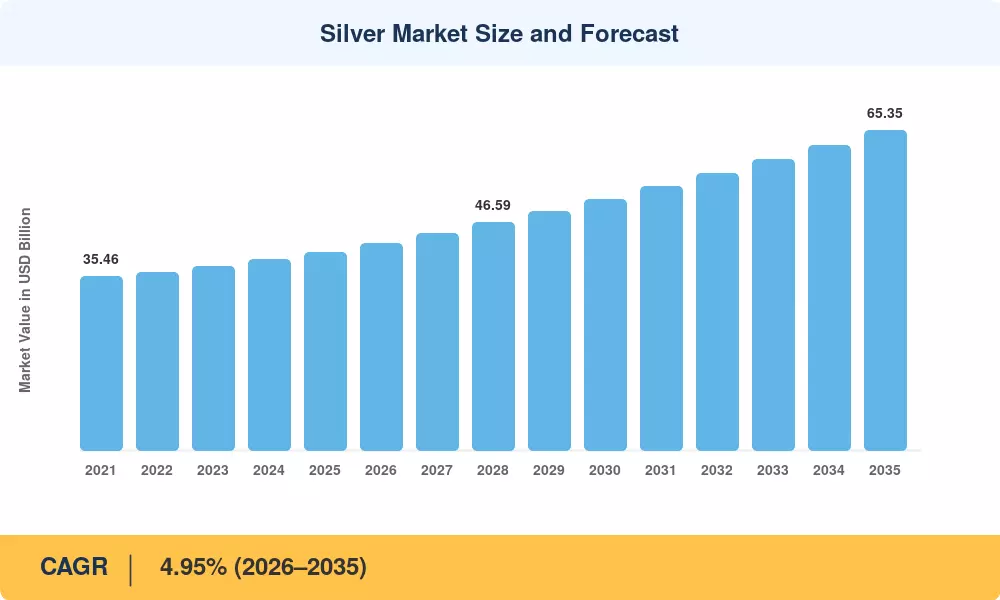

Silver Market Summary

The Silver Market reached an estimated 40.42 kilotons of global consumption in 2025, rising to a projected 42.30 kilotons in 2026 as photovoltaic cell metallization, 5G infrastructure build-outs, and high-voltage direct-current connector adoption accelerated draw on refined supply. Over the 2026–2035 forecast window, the Silver Market is expected to expand at a 4.95% CAGR, reaching approximately 65.35 kilotons by 2035. Two catalysts anchor this trajectory: India's Production Linked Incentive scheme for electronics manufacturing, which commits over USD 10 billion in subsidies through 2029 [1], and the IEA's revised Net Zero roadmap calling for a tripling of utility-scale solar capacity by 2035 [2] — both directly intensifying silver offtake.

A structural transformation is reshaping how the Silver Market absorbs refined metal. Legacy thick-film paste formulations that loaded 100–120 mg of silver per photovoltaic cell are giving way to heterojunction and TOPCon architectures that cut loading per cell yet multiply total cell counts, keeping aggregate silver demand elevated. The U.S. Department of Energy's Solar Futures Study projects cumulative U.S. solar installations to surpass 1,000 GW by 2035, implying sustained silver consumption even as per-cell thrifting intensifies [3]. Electronics miniaturization in automotive radar, millimeter-wave 5G antennas, and medical biosensors is simultaneously opening high-value, low-volume channels that carry premium pricing.

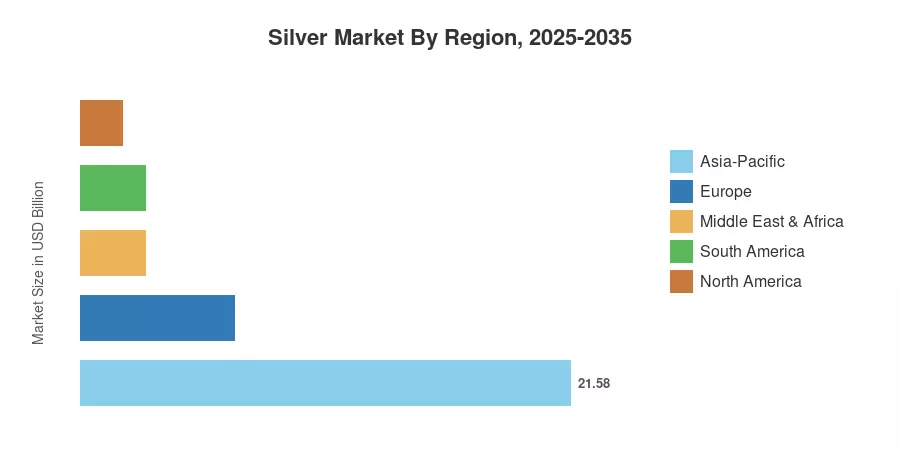

Asia-Pacific commands roughly 53.4% of global Silver Market consumption — driven by China's solar manufacturing dominance and India's fast-growing electronics assembly sector — and is forecast to post the fastest regional CAGR of 5.30% through 2035. North America accounts for about 18.2% of consumption, anchored by U.S. photovoltaic deployment targets and defense electronics procurement. Europe follows at 16.8%, where the REPowerEU plan and the Critical Raw Materials Act are channeling fresh investment into domestic silver refining. The decade ahead will test whether mine supply expansion and recycling innovation can keep pace with the Silver Market's broadening industrial appetite.

Key Report Takeaways

• By Type

- Fine silver held 66.6% of Silver Market volume in 2025, reflecting its dominance across industrial fabrication and investment-grade bar production.

- Argentium silver is forecast to register the fastest type-level CAGR of 5.10% through 2035, propelled by tarnish-resistant jewelry alloys and antimicrobial medical device coatings.

• By Application

- Jewelry and silverware captured approximately 28.0% of the Silver Market volume in 2025, supported by robust consumer demand in India and Southeast Asia.

- Electrical and electronics applications are projected to advance at a 5.15% CAGR between 2026 and 2035 as photovoltaic and 5G end-uses scale.

• By Region

- Asia-Pacific accounted for 53.4% of global Silver Market consumption in 2025, underpinned by China's solar module output and India's electronics expansion.

- North America is expected to grow at a 4.60% CAGR through 2035, with U.S. solar policy and defense procurement as primary demand levers.

Silver Market Size and Forecast (2021–2035)

Market Research Future's sizing model synthesizes mine production data from the World Bureau of Metal Statistics, refinery throughput from the Silver Institute, and downstream demand tracking across photovoltaic, electronics, and jewelry channels. Historical figures (2021–2024) reflect actuals; 2025 is the validated base year; 2026–2035 are forecast estimates applying a calibrated 4.95% CAGR with demand-weighted adjustments by end-use.

.webp?v=1784027855)