Small Hydropower Market Summary

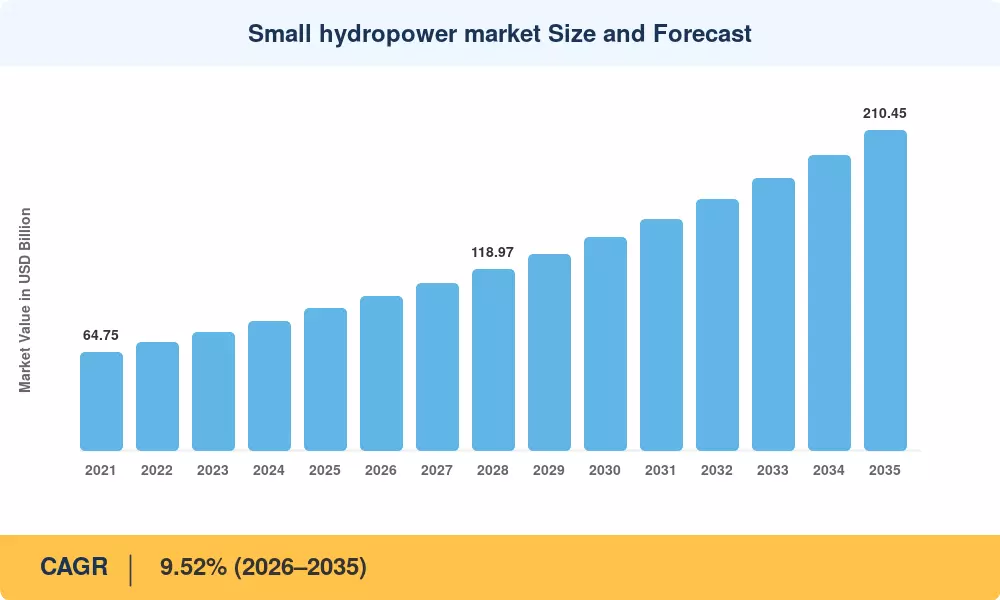

The Small Hydropower Market reached an installed capacity of 93.17 GW in 2025, positioning it as one of the most dependable pillars of distributed renewable generation worldwide. Starting from an estimated 101.38 GW in 2026, the Small Hydropower Market is projected to expand to 210.45 GW by 2035 at a CAGR of 9.52% during the forecast period (2026–2035). This trajectory is anchored in aggressive rural electrification mandates — India's Small Hydro Power Program alone targets 5 GW of new capacity by 2030, while the European Union's revised Renewable Energy Directive channels preferential feed-in tariff structures toward run-of-river small hydro plant installations below 10 MW[2].

A generational technology revolution is changing how small hydropower assets are constructed and operated. Advanced micro hydro turbine off-grid architectures are replacing conventional fixed speed turbine systems with variable speed permanent magnet generators. Examples of fish-friendly turbine designs opening up hitherto limited streams in Scandinavia and the Pacific Northwest include minimum-gap runner technology and downstream bypass systems. The International Renewable Energy Agency (IRENA) forecasts that in 2024, global investment in small hydropower was above USD 5.8 billion and that digital twin platforms and IoT-enabled predictive maintenance have reduced levelized costs by 12–18% over the last five years [3][4].

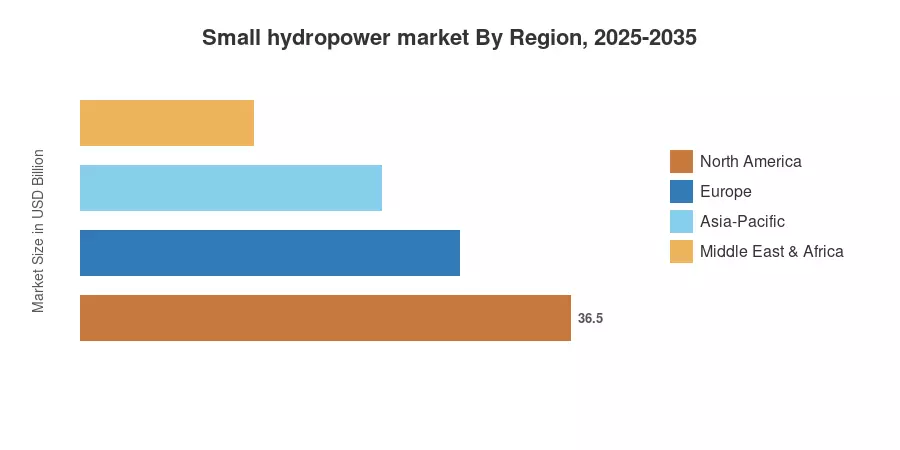

The Asia-Pacific region hosts an estimated 58.90% of the global installed capacity in the Small Hydropower Market, thanks to China’s pioneering work on rural electrification with pico hydro generators and India’s rapid development of mini-grids. The Middle East & Africa is the fastest growing geography, with a 15.47% CAGR through 2035 as countries like Ethiopia and Kenya tap into untapped river basins. Europe ranks second with a proportion of around 19.25%, thanks to grid-connected feed-in mechanisms in Germany, France and the Nordic countries. Within the next decade, low-head small hydropower weir designs and hybrid solar-hydro arrangements will reshape baseload generation across emerging and established grids [5][6].

Key Report Takeaways

• By Capacity

- The 1–10 MW segment accounted for 62.15% of the Small Hydropower Market in 2025, reflecting utility-scale project pipelines across Asia-Pacific and Europe

- Micro and pico systems (Up To 1 MW) are expanding at an 11.13% CAGR through 2035, led by off-grid rural electrification demand

• By Technology

- Run-of-river installations retained a 55.72% share of installed capacity in the Small Hydropower Market during 2025

- In-stream and micro-conduit projects record the fastest technology-segment growth at 11.58% CAGR to 2035

- Reservoir-based systems continue to serve baseload grid-connected feed-in applications in mountainous terrains

• By End-User

- Utilities captured 62.85% of end-user capacity in 2025, anchoring grid stability with small hydro turbine Francis Kaplan configurations

- Independent power producers exhibit the highest growth momentum at 11.92% CAGR through 2035

• By Geography

Small Hydropower Market Size and Forecast (2021–2035)

The market sizing approach of Market Research Future (MRFR) combines bottom-up capacity tracking from national hydropower registries with top-down validation from IRENA’s Renewable Capacity Statistics database. Historical statistics (2021–2024) are commissioned and grid-synchronized capacity published by FERC, the European Small Hydropower Association (ESHA) and China’s National Energy Administration. Market Forecast Projections (2026 – 2035): Permitted project backlog, Policy pipeline analysis, Technology learning curves for the Small Hydropower Market.

.webp?v=1784802862)