Small Satellite Market Summary

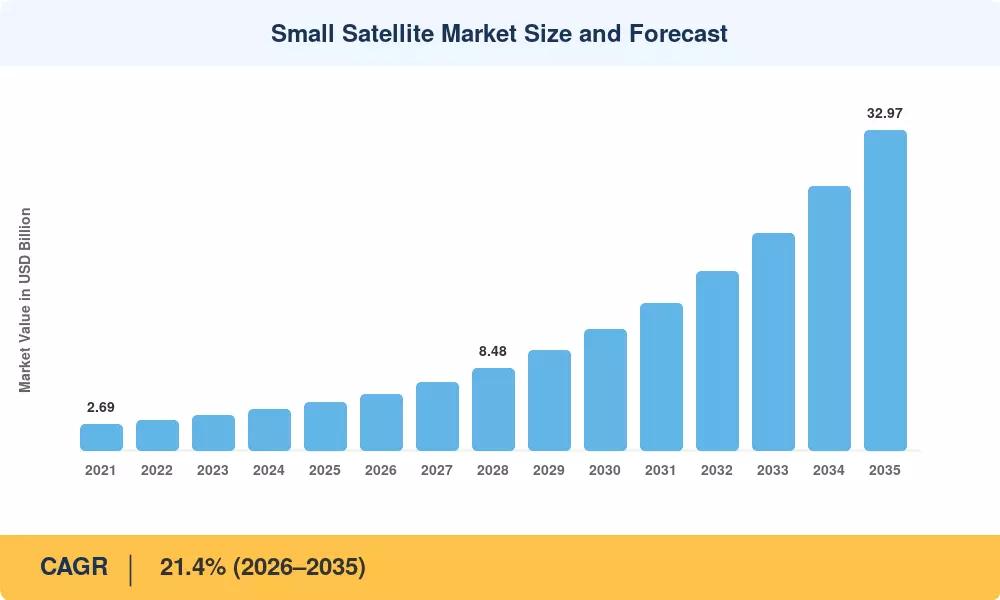

The Small Satellite Market was valued at USD 4.95 billion in 2025 and is projected to reach USD 5.75 billion by 2026, expanding to USD 32.97 billion by 2035 at a compound annual growth rate of 21.4% during the 2026–2035 forecast period. This acceleration reflects a structural shift in how governments and enterprises access space — moving away from a handful of multi-billion-dollar flagship programs toward distributed architectures that deploy dozens or hundreds of spacecraft operating in coordinated fleets. Policy catalysts such as the U.S. Space Development Agency's Proliferated Warfighter Space Architecture, which allocated over USD 4.6 billion across its Tranche 2 procurement cycles, have created sustained procurement pipelines for platform builders and payload integrators alike [1].

Legacy satellite programs that depended on decade-long development timeframes and single-point-of-failure designs are losing ground to rapid production lines that churn out flight-ready spacecraft in weeks, not years. The economics of reusable launch – led by SpaceX’s Falcon 9 program and Rocket Lab’s Electron recovery efforts – have reduced per-kilogram launch costs down to about USD 3,000 for rideshare missions, a reduction of roughly 85% from 2015 baselines [2]. The price drop requires operators to upgrade technology every 18 to 24 months, integrating the latest processors, software-defined radios and sensor arrays right into production.

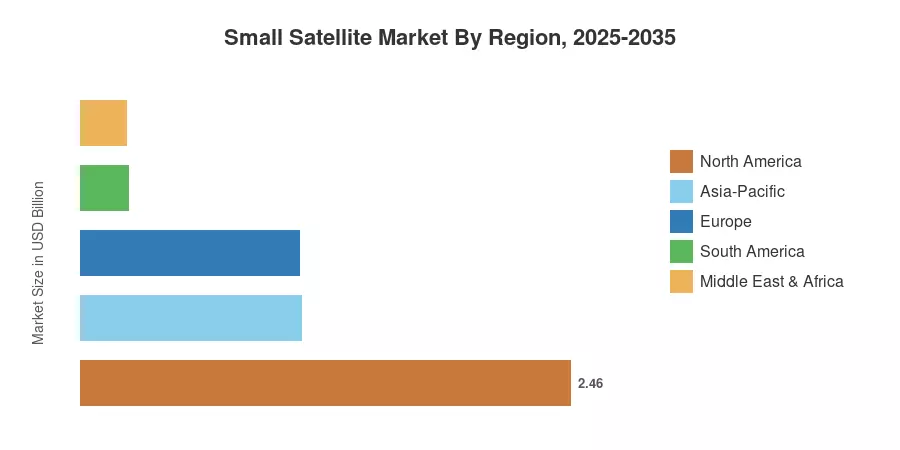

North America represented a ~49.7% share of the Small Satellite Market in 2025, owing to the high concentration of operators, launch providers, and defense programs in the United States. The Asia-Pacific area is the fastest expanding space economy, expected to develop at a CAGR of 22.4% by 2035, driven by ambitious national space projects in India, Japan and South Korea. Europe had the second-biggest proportion at about 22.3%, fueled by ESA’s Copernicus expansion and a growing pipeline of commercial constellation ventures. The next decade will be kind to companies that can blend manufacturing scale with flexible mission profiles.

Key Report Takeaways

• By Application

- Communication accounted for 48.5% of the Small Satellite Market in 2025, driven by broadband mega-constellation build-outs and direct-to-device connectivity trials.

- Earth Observation is forecast to grow at a 22.6% CAGR through 2035, propelled by insurance, agriculture, and defense analytics demand for sub-daily revisit imagery.

• By Satellite Mass

- Minisatellites (100–500 kg) captured 41.8% of the Small Satellite Market share in 2025, favored for their payload flexibility and extended mission life.

- Microsatellites are projected to expand at a 22.2% CAGR through 2035 as component miniaturization widens their operational envelope.

• By End User

- Commercial operators held 59.2% of the Small Satellite Market in 2025, underscoring the private sector's growing dominance in constellation deployment.

• By Geography

- North America led with a 49.7% share, while Asia-Pacific is expected to post the highest regional CAGR at 22.4% through 2035.

Small Satellite Market Size and Forecast (2021–2035)

Market Research Future (MRFR) cross-checks historical estimations against verified launch manifests, operator revenue declarations, and government procurement disclosures. Forecast projections are derived from contracted backlog data, announced constellation filings, and regulatory pipeline research.

.webp?v=1783341785)