Smart Contracts Market Summary

The Smart Contracts Market reached USD 2.78 billion in 2025 and is projected to grow from USD 3.38 billion in 2026 to USD 19.51 billion by 2035, registering a 21.5% CAGR during the 2026–2035 forecast period. Two catalysts are accelerating this trajectory: the European Union's Markets in Crypto-Assets (MiCA) regulation, which gives financial institutions a compliance template for deploying on-chain settlement workflows [1], and Wyoming's state-issued stable-token legislation, which creates a regulatory sandbox for programmable fiat instruments [2]. Together, these frameworks compress enterprise project timelines from years to months.

The technical transition underway is replacing legacy clearing and reconciliation layers, generally run by three or four intermediaries, with self-executing code that settles transactions in minutes instead of days. Large banks like JPMorgan and HSBC are already using blockchain payment rails for high-value cross-border transactions, while multinational retailers are trialing stablecoin payment channels to reduce card-processing fees by up to 70% [3]. Interoperability protocols connecting public and private ledgers have matured enough to enable multi-network orchestration, removing a big hurdle to adoption that plagued early roll-outs.

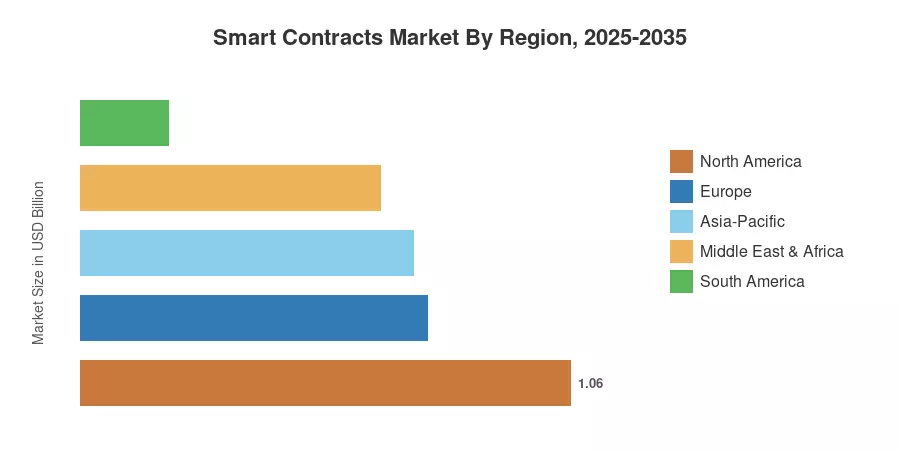

North America holds around 38% of the Smart Contracts Market share, backed by strong venture-capital support and regulatory clarity in important U.S. states. The Asia-Pacific area is the fastest expanding, led by government-sponsored digitalization efforts in India, South Korea and Singapore. Europe is second with about 27%, fuelled by MiCA uptake and the European Central Bank’s digital euro experimentation. Post-quantum encryption and green consensus methods are reducing perceived risk, and sectors such as healthcare and utilities are likely to be early adopters in the next wave through 2035, particularly conservative sectors.

Key Report Takeaways

• By Contract Type & Deployment Model

- Application Logic Contracts held 44.8% of revenue share in 2025, reflecting strong demand for programmable financial settlement and supply-chain automation.

- Decentralized Autonomous Organizations are set to expand at a 32.7% CAGR through 2035, fueled by community-governed treasury models in DeFi and gaming ecosystems.

- Layer-2 solutions are forecast to record the fastest deployment-model CAGR of 30.9% to 2035, as rollup architectures reduce transaction costs by over 90%.

• By Enterprise Size & End-User Industry

- Large organizations accounted for 63.2% of the Smart Contracts Market in 2025, led by banks and insurers embedding blockchain into core operations.

- Small and medium enterprises are adopting smart contracts at a 29.5% CAGR, enabled by low-code blockchain platforms that eliminate the need for Solidity expertise.

• By Geography

- North America leads the Smart Contracts Market with approximately 38% share, underpinned by U.S. fintech innovation corridors and Canadian blockchain sandbox programs.

- Asia-Pacific's 25.8% CAGR positions it as the fastest-growing region, with India's Digital India Stack and South Korea's CBDC pilots as primary accelerants.

Smart Contracts Market Size and Forecast (2021–2035)

MRFR’s forecasts integrate bottom-up income analysis of platform licensing, transaction-fee pools, and consulting-integration services with top-down validation against enterprise blockchain spending standards released by the World Economic Forum [4][5]. Historical figures are sourced from annual reports, SEC filings and venture-capital databases. Forecast years are based on a calibrated CAGR, guided by regulatory acceptance curves and protocol-level on-chain activity measures.