Smart PPE Market Summary

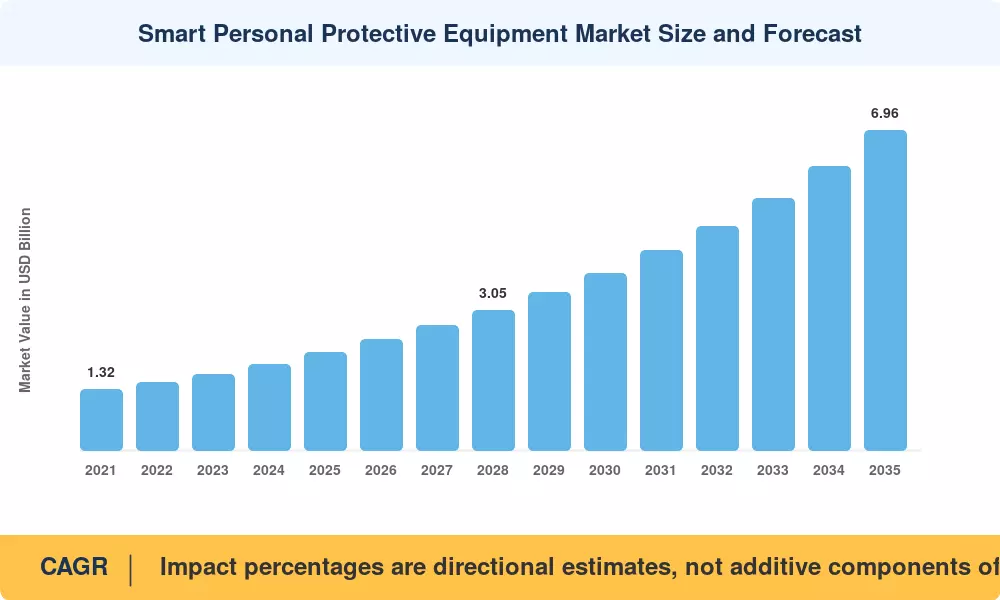

The Smart Personal Protective Equipment Market reached an estimated USD 2.14 billion in 2025 and is projected to grow from USD 2.41 billion in 2026 to USD 6.96 billion by 2035, registering a CAGR of 12.5% during the 2026–2035 forecast period. Two forces are reshaping workplace safety spending: OSHA's 2024 rulemaking on electronic logging of exposure incidents [1] and the European Commission's revision of Regulation (EU) 2016/425, which for the first time incorporates digital performance criteria for Category III PPE [2]. Together, these regulatory moves have catalyzed over USD 1.2 billion in cumulative corporate investment into sensor-enabled protective gear since 2022.

Traditional hard hats, gloves, and high-visibility vests are giving way to connected alternatives that embed inertial measurement units, environmental sensors, and low-power wide-area network (LPWAN) radios directly into the equipment. Major EPC contractors such as Bechtel and Fluor reported 18–22% reductions in recordable incident rates after deploying smart helmet programs across Gulf Coast refinery projects in 2023–2024 [3]. The European Agency for Safety and Health at Work (EU-OSHA) allocated EUR 12 million to its 2024–2027 Healthy Workplaces campaign, explicitly naming wearable hazard detection as a priority technology track [4].

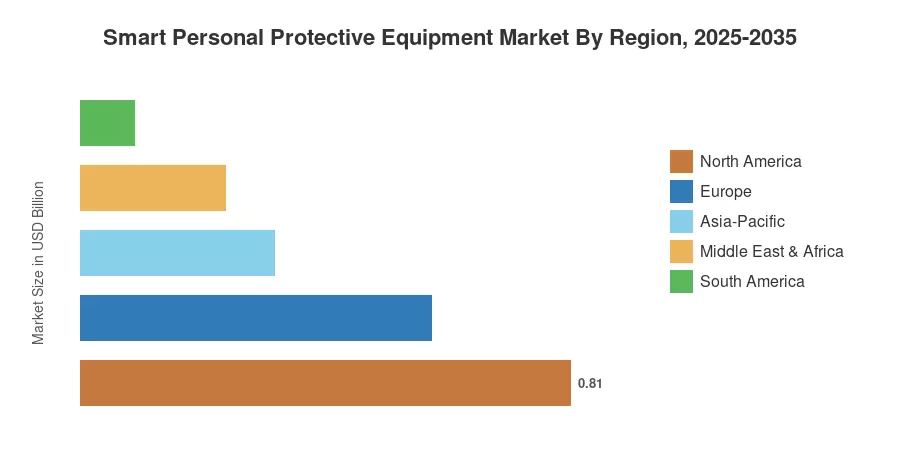

North America commands roughly 38% of the Smart Personal Protective Equipment Market, driven by mature regulatory enforcement and high per-worker safety budgets. Asia-Pacific is the fastest-growing region, with a projected CAGR of 14.8% as China, India, and Australia scale mine-safety and construction-site digitization programs. Europe holds the second-largest share at 27%, anchored by stringent EU harmonized standards and strong adoption across the automotive manufacturing sector. The decade ahead will reward vendors that pair hardware durability with cloud-based analytics platforms.

Key Report Takeaways

• By Product Type

- Smart helmets and hard hats dominate with approximately 31% share of the Smart Personal Protective Equipment Market, reflecting the head-protection segment's early integration of impact sensors and proximity alerts.

- Gas detection wearables are expanding at a CAGR of 14.2%, fueled by tightening exposure-limit regulations in petrochemical and mining verticals.

- Exoskeletons represent the highest-value segment per unit, with average selling prices above USD 5,000, targeting logistics and automotive assembly applications.

• By End-Use Industry

- Construction accounts for the largest revenue pool in the Smart Personal Protective Equipment Market, valued at approximately USD 620 million in 2025.

- Oil and gas end users register a projected CAGR of 13.6%, driven by confined-space monitoring mandates across North American midstream operations.

- Manufacturing is the third-largest vertical, holding roughly 18% share as Industry 4.0 retrofits incorporate wearable sensor networks into existing MES platforms.

• By Region

- North America leads the Smart Personal Protective Equipment Market with 38% revenue share, anchored by the U.S. and Canada.

- Asia-Pacific is forecast to grow at a 14.8% CAGR through 2035, with China accounting for over 40% of regional demand.

- Europe holds approximately 27% share, with Germany and the U.K. as the primary adoption centers.

Smart Personal Protective Equipment Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue modeling from 42 product SKU categories with top-down cross-validation against OSHA compliance spend databases, EU PPE trade data (Eurostat CN Code 6506), and company-reported revenues from 10 publicly listed participants. Historical figures (2021–2024) reflect actual shipment data; the base year (2025) blends Q1–Q3 actuals with Q4 estimates. Forecast values (2026–2035) apply segment-level growth assumptions triangulated against macroeconomic industrial output indices from the World Bank and ILO workplace-safety expenditure surveys [5][6].