Smart Toys Market Summary

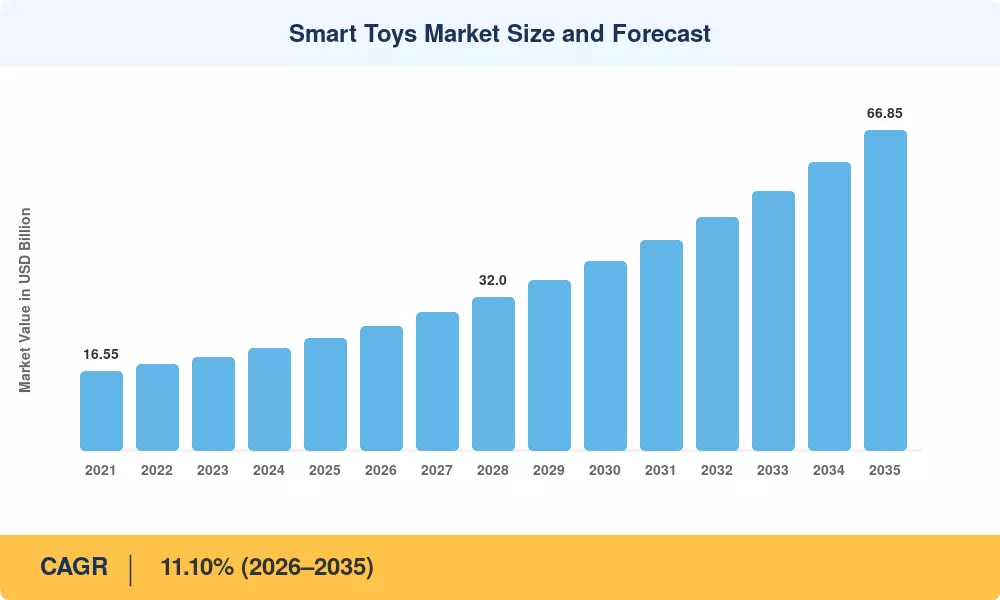

The Smart Toys Market reached a valuation of USD 23.33 Billion in 2025 and is projected to grow from USD 25.92 Billion in 2026 to USD 66.85 Billion by 2035, registering a CAGR of 11.10% over the forecast period (2026–2035). Parental appetite for play-based STEM education, coupled with strengthened children's data-privacy frameworks such as the U.S. COPPA 2.0 rulemaking and the EU's Age-Appropriate Design Code, is channeling investment into safe, scalable connected play platforms. Toy-industry venture funding surpassed USD 1.2 billion in 2024, a signal that capital markets view the Smart Toys Market as a durable growth story rather than a niche novelty [1].

Beyond these headline numbers, a technical change is changing product architectures. Old-fashioned battery-powered toys with set audio loops are being replaced by edge-AI-powered devices that change talks and difficulty levels in real time. Cloud agreements between incumbent toy makers and AI vendors have shortened development timelines from 18 months to less than nine, allowing brands to refresh content via subscription-based OTA updates rather than launching all new SKUs. Low-latency multiplayer robotics experiences are beginning to emerge in the Asia-Pacific, facilitated by 5G-enabled play venues that charge a 20–30% price premium over Wi-Fi-only equivalents [2].

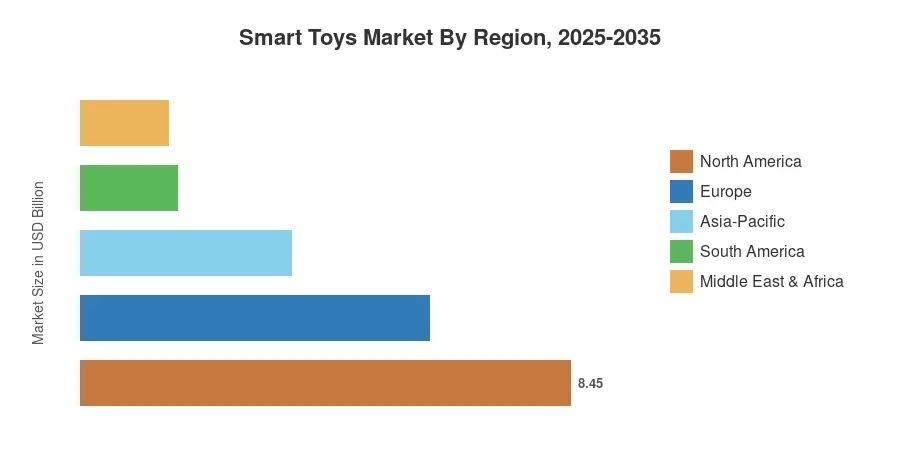

North America dominated the worldwide Smart Toys Market with a share of over 36.2% in 2025, driven by high family discretionary income and deep-rooted ed-tech adoption. Asia-Pacific is seeing the highest growth, with a projected regional CAGR of 15.60% through 2035, as hands-on robots are included in national STEM curricula in China, India, and South Korea. Europe, the second-largest region, is led by Germany and the UK, where strong product-safety regulations ironically boost consumer confidence in high-end connected toys. The Smart Toys Market is anticipated to shift from novelty gadgetry to a mainstream educational infrastructure category within the next decade.

Key Report Takeaways

• By Interfacing Device

- Smartphone-connected toys captured 40.8% of the global Smart Toys Market revenue in 2025, driven by ubiquitous companion-app ecosystems.

- Console-connected toys are forecast to expand at a CAGR of 23.4% through 2035 as gaming consoles integrate AR-toy peripherals.

• By Technology

- Wi-Fi-based solutions accounted for 47.2% of the Smart Toys Market share in 2025.

- NFC/RFID connectivity is advancing at a 21.1% CAGR, fueled by tap-and-play physical-digital convergence.

• By Distribution Channel

- Online stores represented 56.2% of Smart Toys Market sales in 2025, reflecting the dominance of D2C and marketplace channels.

- Specialty and convenience stores are gaining traction as experiential retail formats let children trial connected products before purchase.

• By Region

- North America commanded 36.2% of the 2025 Smart Toys Market, supported by mature e-commerce logistics and early-adopter demographics.

- Asia-Pacific is forecast to register the highest regional CAGR at 15.60% through 2035.

Smart Toys Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up revenue modeling from manufacturer sell-through data with top-down validation using import-export trade flows, retail panel audits, and publicly disclosed company revenues. Historical figures (2021–2024) are reconciled against industry association reports, while the forecast (2026–2035) applies regression-weighted demand drivers calibrated to macroeconomic and demographic indicators.