Smart Waste Management Market Summary

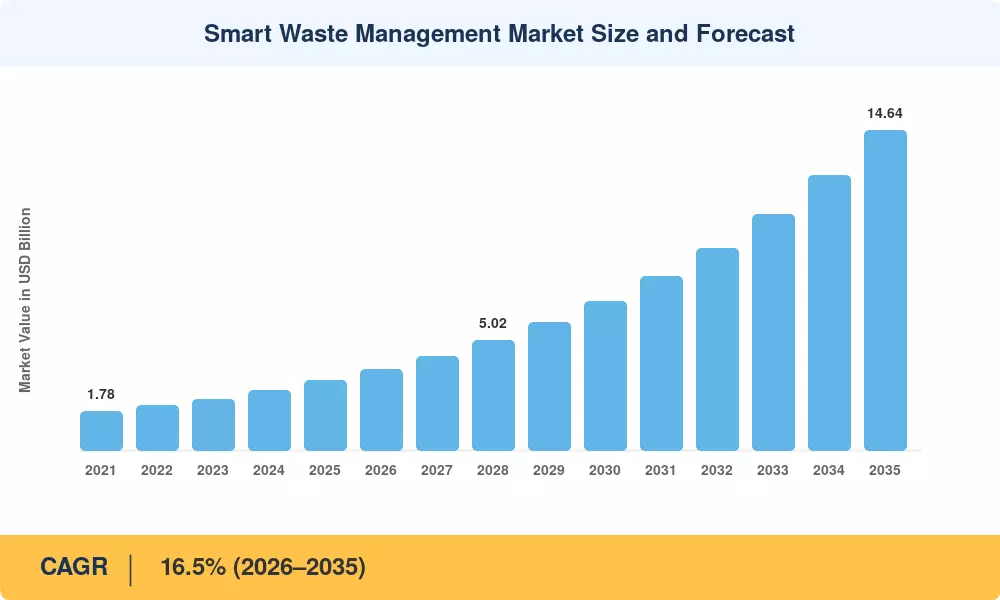

The Smart Waste Management Market reached an estimated USD 3.18 billion in 2025 and is projected to grow from USD 3.70 billion in 2026 to USD 14.64 billion by 2035, registering a CAGR of 16.5% during the forecast period (2026–2035). Two forces are accelerating this trajectory: the European Union's revised Waste Framework Directive mandating 65% municipal recycling rates by 2035, and the USD 3.5 billion allocated under the U.S. Infrastructure Investment and Jobs Act for solid-waste modernization [1][2]. Cities that once relied on fixed collection schedules and manual bin checks are now under regulatory and fiscal pressure to digitize operations.

The transition in technology is essential. Sensor-enabled containers, cloud-based analytics platforms and AI-powered collection scheduling are replacing older fleet dispatch systems that rely on static routing and paper manifests. The World Bank says global yearly trash generation will approach 3.4 billion tons by 2050, yet less than 30% of cities in high-income countries have linked waste infrastructure [3]. The Smart Waste Management Market’s main value proposition is to bridge that gap, accomplishing more with less, via real-time data and predictive logistics.

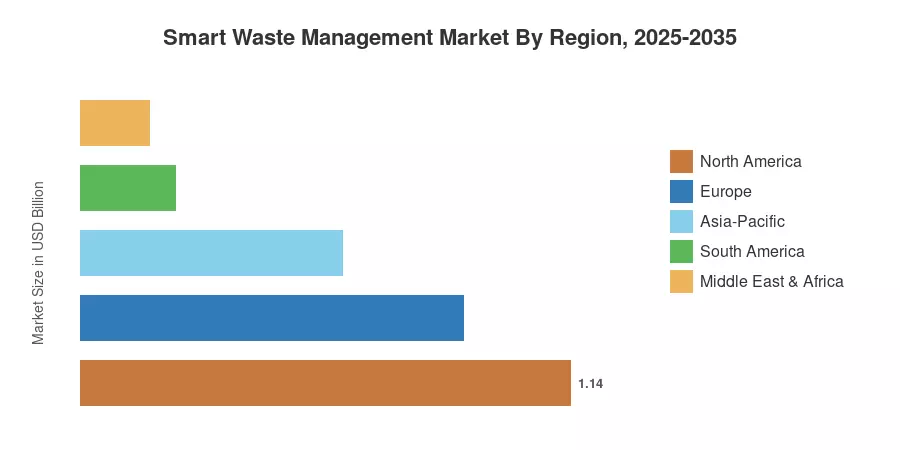

North America continues to lead the pack at about 36% market share, supported by early municipal IoT deployments in U.S. and Canadian metros. Asia Pacific is the fastest expanding area with a predicted CAGR of 19.2% fueled by rising urbanization in India, China and Southeast Asia. Europe holds the second-highest share with 28%, bolstered by tough circular economy legislation. As landfill taxes rise and ESG reporting requirements tighten, the Smart Waste Management Market is set to become an essential part of municipal infrastructure, not a discretionary update.

Key Report Takeaways

• By Solution

- Fleet management platforms dominate with approximately 32% share of the Smart Waste Management Market, reflecting demand for dynamic routing and fuel-cost reduction across municipal fleets.

- Analytics and reporting solutions are the fastest-growing solution segment at a 19.1% CAGR, as cities seek predictive fill-level insights and compliance dashboards.

• By End User

- Municipal and government agencies account for the largest share of the Smart Waste Management Market at roughly 42%, driven by regulatory mandates and public sustainability targets.

- Industrial and commercial end users are projected to reach USD 5.12 billion by 2035 as private enterprises integrate waste tracking into ESG reporting workflows.

• By Geography

- North America leads with a 36% share, supported by federal infrastructure spending and mature municipal procurement cycles.

- Asia-Pacific is expected to register the highest regional CAGR of 19.2% through 2035.

- Europe contributes 28% of global revenue, propelled by the EU Circular Economy Action Plan.

Smart Waste Management Market Size and Forecast (2021–2035)

Market sizing is based on a bottom-up model of municipal budgets, enterprise waste-management contracts and technology-vendor revenues in 42 countries. Historical figures (2021-2024) are based on data from public procurement databases, firm filings and validated industry surveys. Forecast forecasts (2026–2035) are derived from macroeconomic factors, regulatory delays, and adoption-curve benchmarks of similar municipal-tech categories.