Speaker Market Summary

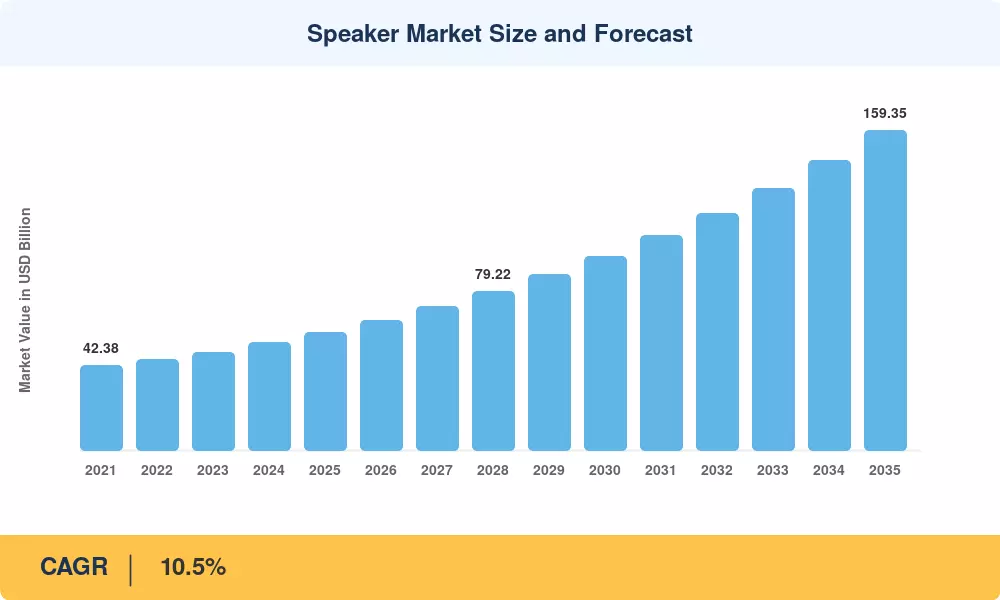

The global Speaker Market reached an estimated USD 58.72 Billion in 2025, positioning the industry for a forecast trajectory that begins at USD 64.88 Billion in 2026 and climbs to USD 159.35 Billion by 2035, registering a CAGR of 10.5% across the forecast window. Two catalysts anchor this expansion: the acceleration of voice-activated smart home ecosystems — with global smart speaker installed bases crossing 320 million units in 2024 [1] — and sustained consumer investment in premium audio driven by spatial-audio standards such as Dolby Atmos and Sony 360 Reality Audio [2].

A generational shift in audio hardware is underway. Legacy wired bookshelf and tower configurations are steadily giving way to compact wireless soundbar architectures, multi-room mesh systems, and AI-integrated smart speakers capable of acting as central hubs for IoT devices. The Bluetooth Special Interest Group reported that audio device shipments with LE Audio support grew 35% year-over-year in 2024, signaling a structural migration toward low-energy, high-resolution wireless codecs [3]. Manufacturers are responding with product lines that fuse voice assistant intelligence, adaptive room calibration, and lossless streaming into form factors designed for both portability and home installation.

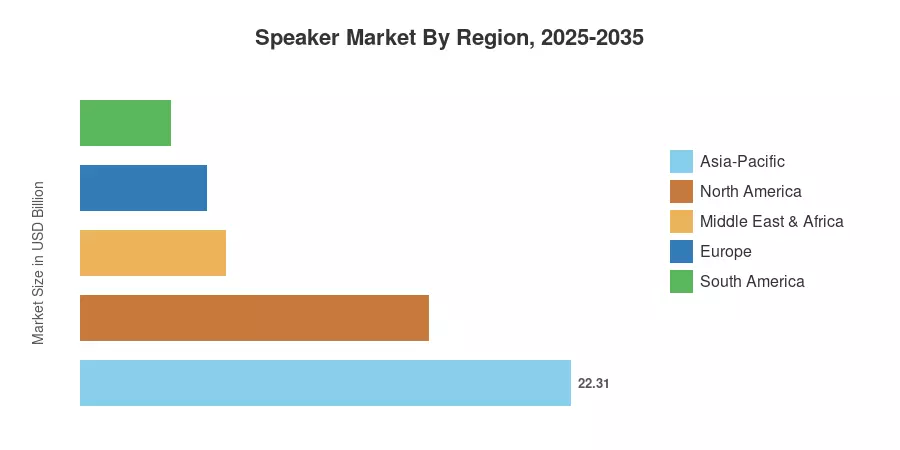

Asia-Pacific commands the largest share of the Speaker Market at approximately 38%, buoyed by high smartphone penetration in China and India, plus rising disposable incomes in Southeast Asian economies. The region is also the fastest-growing, projecting a CAGR of 12.1% through 2035. North America holds roughly a 27% share, anchored by mature smart-home adoption and premium audio spending. Europe accounts for about 22%, driven by automotive audio integration and home renovation cycles. As streaming content volumes continue to surge globally, the Speaker Market stands positioned for a decade of broad-based expansion across geographies and product categories.

Key Report Takeaways

• By Type

- Soundbars captured approximately 38% of the Speaker Market in 2025, driven by television audio replacement trends and slim-profile design advantages.

- The outdoor speaker segment is projected to grow at a CAGR of 12.8% through 2035, fueled by hospitality venue upgrades and residential outdoor living investments.

- Subwoofer demand continues to accelerate in the Speaker Market, with the segment valued at USD 12.92 Billion in 2025.

• By Application

- Home entertainment remains the dominant application in the Speaker Market, representing 42% of total revenues in 2025.

- Automotive audio applications are growing at a CAGR of 11.6%, reflecting the integration of premium audio suites into electric vehicle cabins.

• By Region

- Asia-Pacific leads the Speaker Market with a regional valuation of USD 22.31 Billion in 2025.

- North America's Speaker Market is characterized by a 10.3% CAGR, supported by smart speaker refresh cycles and premium soundbar adoption.

- Europe holds approximately 22% of the global Speaker Market share, with automotive OEM audio partnerships acting as a primary growth engine.

Speaker Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing model integrates primary interviews with OEM executives, distributor sell-through data, customs trade databases, and third-party shipment trackers. Historical figures (2021–2024) are validated against public financial disclosures from leading manufacturers, while forecast projections (2026–2035) incorporate regression-adjusted demand drivers including streaming subscriber growth, smart-home penetration curves, and construction-spending indices.