Specialty Silica Market Summary

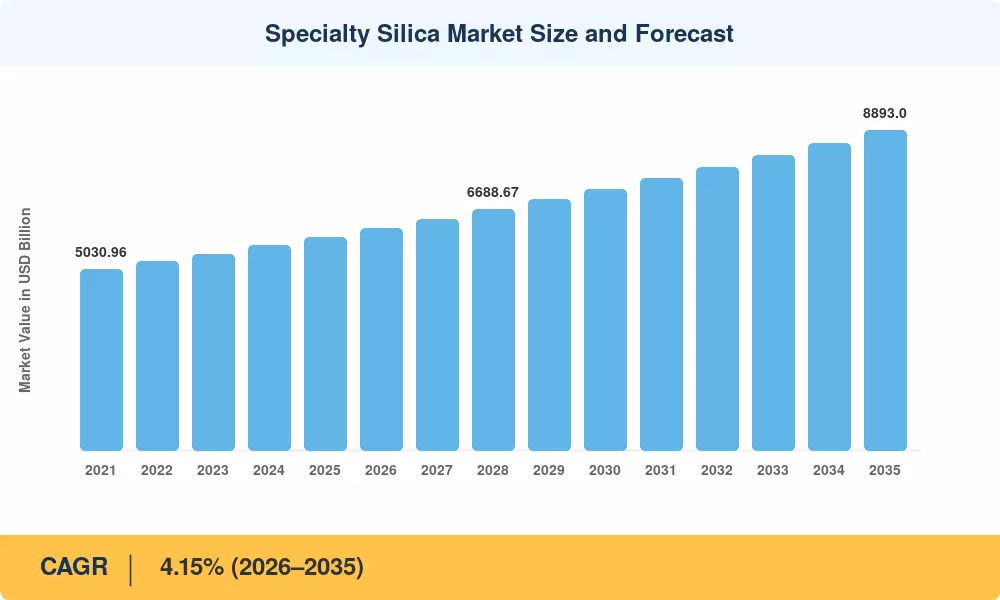

The global Specialty Silica Market reached an estimated valuation of USD 5,920 Million in 2025 and is projected to grow from USD 6,166 Million in 2026 to USD 8,893 Million by 2035, registering a CAGR of 4.15% during the forecast period. This trajectory reflects expanding regulatory mandates around green-tire labeling in Europe and Asia, alongside sustained capital commitments from automotive OEMs shifting toward low-rolling-resistance tire compounds that rely heavily on precipitated silica materials as reinforcing filler materials[2].

The way performance silica products are delivered to end-use markets is changing at the technological level. The carbon-intensive and energy-intensive legacy fumed-silica processing is gradually giving way to bio-derived extraction methods, especially rice-husk ash platforms that are becoming popular in Southeast Asia and India. High-purity silica grades with tailored particle morphologies are being pushed by the European Commission's REACH amendments (2024 revision cycle), which have increased exposure restrictions on crystalline silica dust. Through 2030, it is anticipated that global green tire investment alone will total more than USD 18 billion, serving as a structural demand anchor for specialty mineral fillers [3][4].

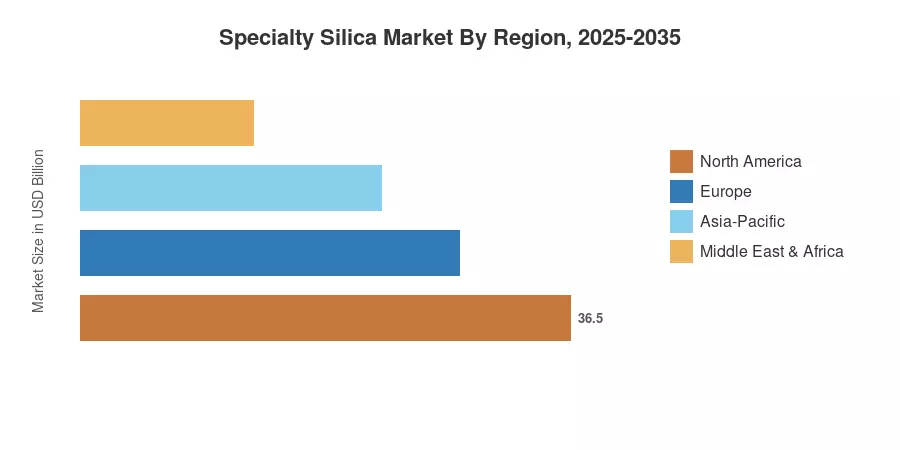

Asia-Pacific is the fastest-growing region and has about 49% of the Specialty Silica Market. It is expected to develop at a 4.92% CAGR through 2035 due to India's booming rubber reinforcement chemicals industry and China's mandated tire-labeling program. Due to the demand for semiconductor-grade silica additives in advanced chip packaging, North America has the second-largest share at around 22.5%. The usage of industrial silica compounds in food-grade and medicinal applications is being accelerated by sustainability standards in Europe. Margin pools will significantly shift in favor of high-value specialty grades during the next ten years [5][6].

Region

Key Report Takeaways

• By Type

- Precipitated silica accounted for approximately 46.1% of the Specialty Silica Market share in 2025, anchored by tire-industry demand for reinforcing filler materials.

- Silica gel segments are projected to expand at a 3.85% CAGR through 2035, driven by desiccant and chromatography applications requiring high-purity silica.

• By Production Process

- Wet/precipitated production routes held an estimated 70.2% share of the Specialty Silica Market in 2025.

- Bio-silica from rice-husk ash is the fastest-growing production route, forecast to register a 5.49% CAGR as circular-economy models gain traction in emerging economies.

• By Application

- Rubber and tires represented the largest application at roughly 35.1% of revenue in the Specialty Silica Market during 2025.

- Electronics and semiconductors are forecast to grow at a 5.04% CAGR, fueled by demand for ultra high-purity silica additives in wafer-polishing slurries.

• By Region

- Asia-Pacific captured approximately 49.0% of the Specialty Silica Market in 2025, with China and India together accounting for over two-thirds of regional volume.

- North America and Europe collectively represent about 42.3% of global demand, with growth underpinned by semiconductor-grade and pharmaceutical-grade industrial silica compounds.

Region

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) 's market-sizing methodology integrates bottom-up revenue modeling from producer shipment data, trade-flow analysis, and end-use consumption patterns verified through primary interviews with over 45 industry participants. Historical values (2021–2024) are calibrated against audited company filings and customs databases; forecast projections (2026–2035) apply segment-level demand elasticities against macro indicators, including automotive production, construction spend, and semiconductor capital expenditure[7].

.webp?v=1783930677)