Spinal Implants Market Summary

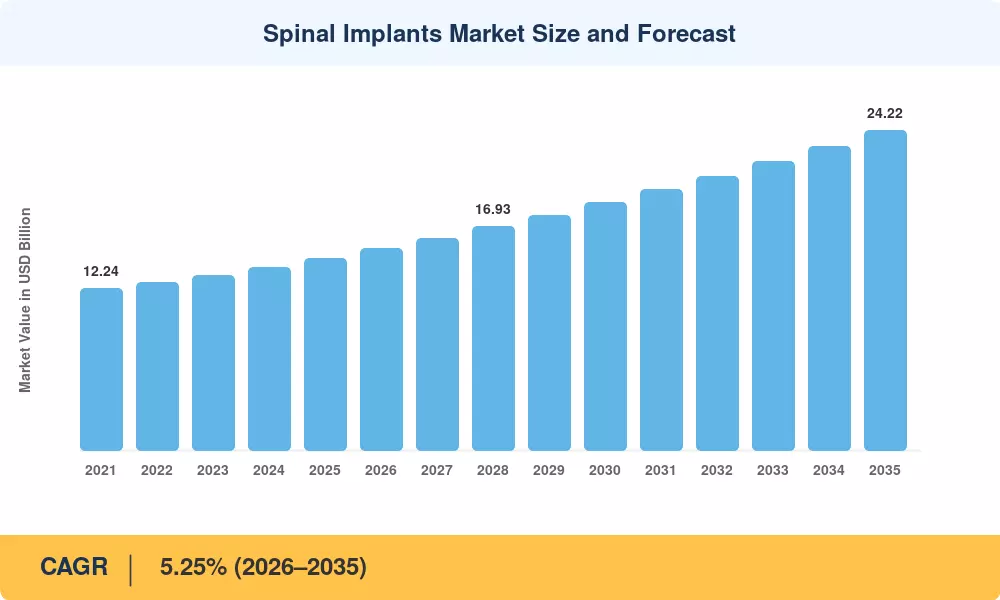

The Spinal Implants Market size was valued at USD 14.52 Billion in 2025, and the market is projected to grow from USD 15.28 Billion in 2026 to USD 24.22 Billion by 2035, registering a CAGR of 5.25% during the forecast period 2026–2035. Two converging forces propel this trajectory: rapidly aging global populations — the WHO projects 2.1 billion people aged 60+ by 2030 — and escalating spinal disorder prevalence tied to sedentary work cultures [2]. Government reimbursement reforms, particularly CMS bundled-payment expansions in the United States, are reshaping procedural economics and broadening patient access to surgical intervention.

Technology is changing the way we plan and perform spine procedures. Intraoperative 3D imaging and AI-guided robotic navigation platforms are replacing legacy open fusion procedures, with patient-specific 3D-printed titanium implants reducing operative time by 18–25% [3]. Mazor X Stealth Edition of Medtronic and the ExcelsiusGPS platform of Globus Medical are the two leading robotic spine systems, with more than USD 1.2 billion in cumulative robotic spine installations worldwide, and this installed base continues to grow [4].

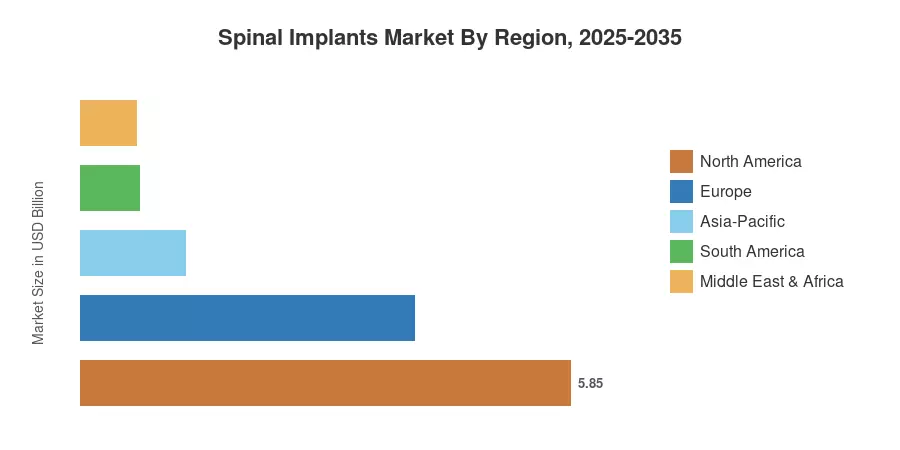

North America dominated the Spinal Implants Market in 2025, accounting for almost 40.3% share, owing to favorable FDA breakthrough-device routes and robust ASC infrastructure. The Asia-Pacific is expected to have the highest CAGR of 8.6% throughout the forecast period due to the rising number of procedures in China and Japan. Europe had the second-highest share at around 27.5%, supported by the medtech cluster in Germany and NHS commissioning reforms in the UK. The Spinal Implants Market is set for steady growth as minimally invasive adoption, outpatient treatment models, and emerging-market hospital development all ramp up simultaneously.

Key Report Takeaways

• By Technology

- Spinal fusion and fixation technologies accounted for approximately 50.2% of the Spinal Implants Market in 2025, driven by high-acuity degenerative disc disease caseloads.

- Motion-preservation solutions are projected to expand at a 9.1% CAGR through 2035, reflecting surgeon preference for adjacent-segment disease reduction.

• By Product & Surgery Type

- Thoracic and lumbar fusion devices represented the largest product category at roughly 37.3% share in 2025.

- Minimally invasive surgery techniques are forecast to grow at a 9.6% CAGR, outpacing open procedures as patient and payer demand for shorter recovery accelerates.

• By Geography

- North America led the Spinal Implants Market with a 40.3% revenue share in 2025, reinforced by CMS reimbursement stability.

- Asia-Pacific is expected to register the highest CAGR of 8.6% through 2035, with China and Japan contributing the majority of incremental volume.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on bottom-up procedural volume modeling, implant ASP tracking across 42 countries, and triangulation against FDA 510(k)/PMA clearance databases and hospital purchasing data [5].