Sterility Testing Market Summary

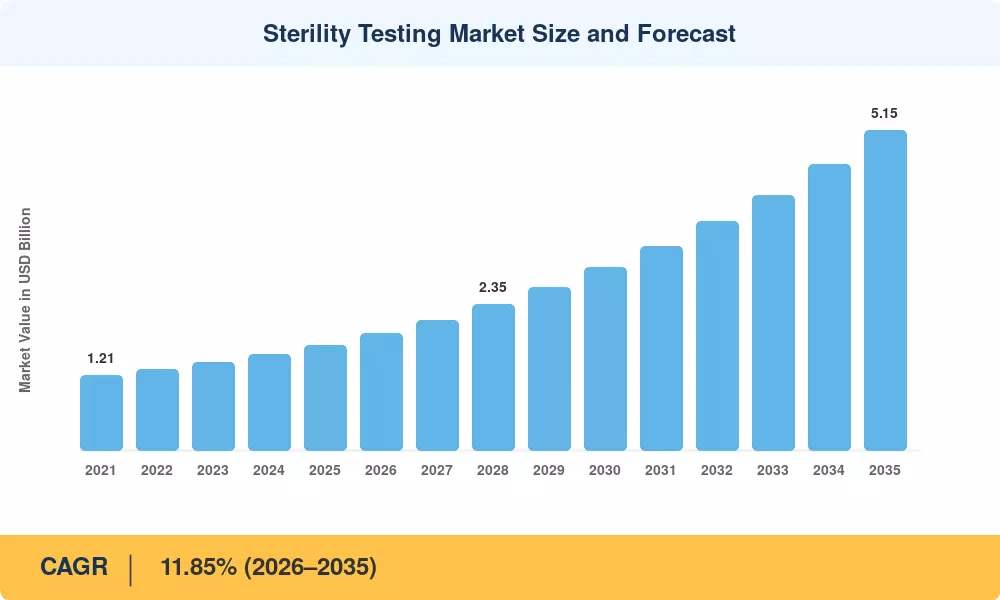

The Global Sterility Testing Market size was valued at USD 1.69 Billion in 2025, and the market is projected to grow from USD 1.88 Billion in 2026 to USD 5.15 Billion by 2035, registering a CAGR of 11.85% during the forecast period 2026–2035. This expansion is propelled by the enforcement of the EU GMP Annex 1 revision — which mandates near-zero colony-forming-unit thresholds for aseptic manufacturing lines — and by the FDA's accelerated approval pathway for cell and gene therapies, which has increased batch-level sterility verification demand by over 40% since 2022 [1][2]. Global biopharmaceutical R&D spending surpassed USD 260 billion in 2024 [3], and each new biologic, biosimilar, or advanced therapy medicinal product adds recurring testing volume to laboratories worldwide.

The technology landscape is shifting away from the legacy 14-day compendial sterility test toward rapid detection platforms that deliver results in under 24 hours. Bioluminescence-based ATP detection, nucleic acid amplification, and flow cytometry systems are gaining traction as regulatory agencies — including the EMA, PMDA, and FDA — publish guidance documents encouraging alternative microbiological methods [4][5]. Sartorius, bioMérieux, and Charles River Laboratories have collectively invested more than USD 450 million in next-generation rapid microbial platforms since 2021, reflecting industry confidence in method modernization [6].

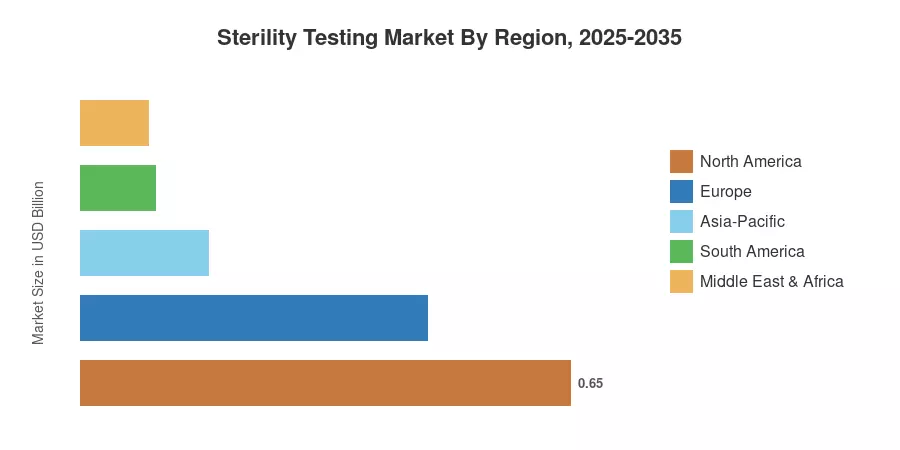

North America accounted for approximately 38.5% of the Sterility Testing Market in 2025, anchored by the concentration of large-molecule fill-finish facilities across the U.S. eastern seaboard and a robust FDA post-market surveillance framework. Asia-Pacific is the fastest-growing region at a 10.34% CAGR through 2035, fueled by China's Pharma 2025 initiative, India's Production-Linked Incentive scheme for biologics, and South Korea's biosimilar export corridor [7]. Europe holds the second-largest share at roughly 27.5%, driven by EMA's zero-tolerance approach to contamination in sterile injectables. As contract development and manufacturing organizations absorb a greater share of global sterile production, the Sterility Testing Market is entering a structurally higher-growth regime.

Key Report Takeaways

• By Product Type

- Kits and reagents captured approximately 46.4% of the Sterility Testing Market in 2025, underpinned by single-use consumable adoption in high-throughput fill-finish operations.

- The services segment is forecast to expand at an 11.38% CAGR through 2035, driven by outsourcing trends among mid-size biopharma companies.

• By Test Type

- Membrane filtration held a 65.5% share of the Sterility Testing Market in 2025, reflecting deep pharmacopeial entrenchment in USP <71> and EP 2.6.1 protocols.

- Rapid sterility tests are projected to grow at a 15.49% CAGR through 2035 as real-time release testing gains regulatory endorsement.

• By Application

- Pharmaceutical and biologics manufacturing contributed 59.6% of the Sterility Testing Market in 2025, with outsourced CDMO testing accelerating at a 13.08% CAGR.

• By Region

- North America generated 38.5% of the global Sterility Testing Market revenue in 2025.

- Asia-Pacific is projected to grow at a 10.34% CAGR from 2026 to 2035, the highest among all regions.

Market Size and Forecast (2021–2035)

Market sizing draws on primary surveys of 120+ pharmaceutical QC directors and procurement heads, validated against published pharmacopeial body data, contract testing laboratory financials, and reagent supplier shipment records. Historical figures (2021–2024) use audited revenue disclosures; the forecast applies a bottom-up demand model segmented by product, test type, application, mode, and region.