Sterilization Equipment Market Summary

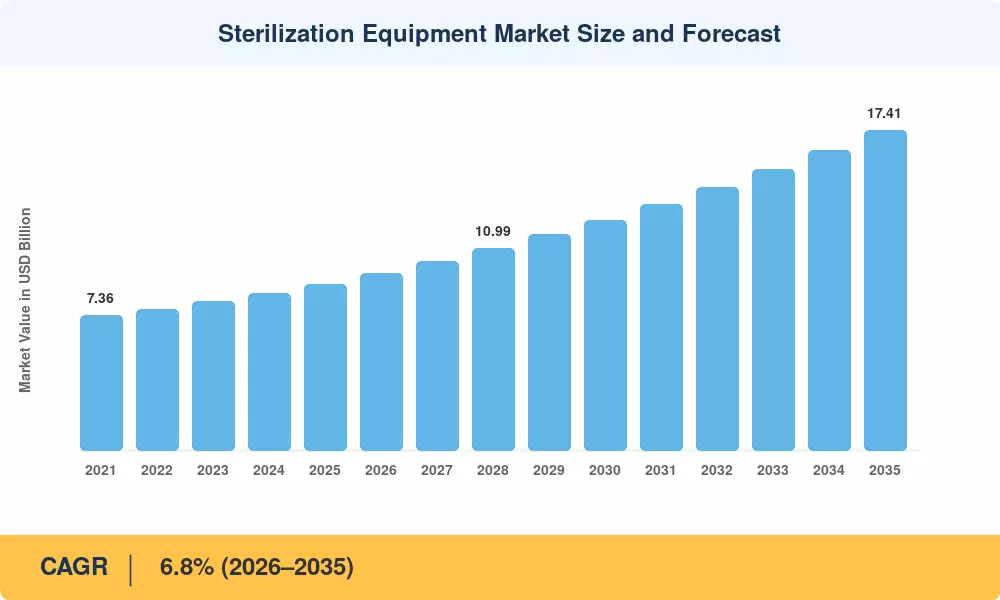

The Global Sterilization Equipment Market size was valued at USD 9.02 Billion in 2025, and the market is projected to grow to USD 17.41 Billion by 2035, registering a CAGR of 6.8% during the forecast period 2026–2035. Two converging forces are accelerating this trajectory: the World Health Organization's updated decontamination protocols for surgical instruments across 194 member states [1], and a post-pandemic wave of central sterile services department (CSSD) capital upgrades worth an estimated USD 4.3 billion across OECD hospital systems between 2023 and 2026 [2]. These catalysts have moved sterilization from a back-of-house cost center to a front-line patient-safety investment. The Sterilization Equipment Market is benefiting from this shift in institutional priorities.

A technology transformation is reshaping the installed base. Legacy gravity-displacement steam units—some two decades old—are being retired in favor of pre-vacuum autoclave sterilizers with integrated digital documentation. Simultaneously, hydrogen-peroxide gas-plasma and vaporized systems are gaining traction for heat-sensitive robotic instruments and flexible endoscopes, a device category growing at roughly 9% annually [4]. The European Union's revised Medical Device Regulation (EU MDR 2017/745), fully enforced since 2024, has mandated traceability from decontamination through to the point of use, driving software-enabled sterilizer demand across the continent [5].

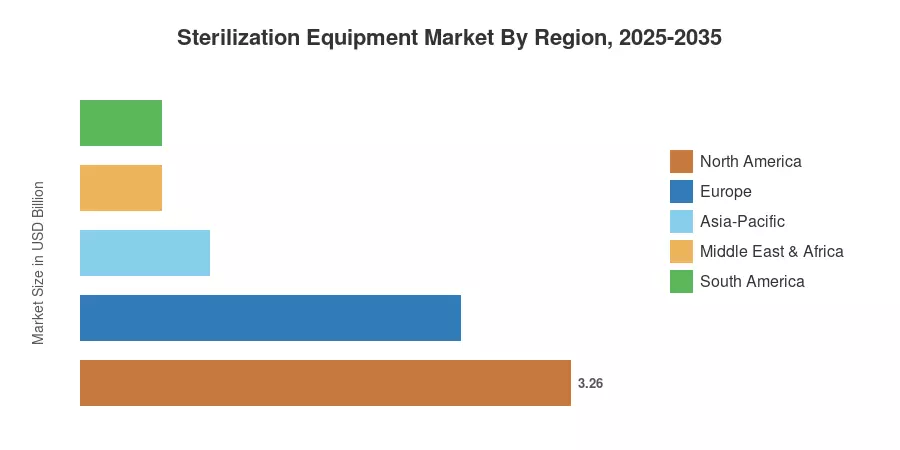

North America commands roughly 36.1% of the Sterilization Equipment Market, anchored by strict FDA reprocessing guidance and large hospital group purchasing organizations [6]. Asia-Pacific is the fastest-growing region, projected at a 9.5% CAGR through 2035, fueled by India's Ayushman Bharat hospital-expansion program and China's county-hospital upgrade initiative [7]. Europe holds the second-largest share at approximately 28%, with Germany and the U.K. leading procurement cycles. Over the coming decade, contract sterilization service demand, single-use device scrutiny, and sustainability pressures will continue to reshape competitive dynamics across the Sterilization Equipment Market.

Key Report Takeaways

• By Equipment

- High-temperature sterilization held approximately 42.1% of the Sterilization Equipment Market in 2025, reflecting the enduring role of steam-based systems in high-volume surgical settings.

- Low-temperature sterilization is forecast to expand at a 10.2% CAGR through 2035, driven by the proliferation of heat-sensitive robotic and endoscopic instruments.

- Ionizing radiation sterilization is projected to grow at a 7.3% CAGR, supported by rising contract sterilization outsourcing among device manufacturers.

• By End User

- Hospitals and clinics accounted for 51.2% of the Sterilization Equipment Market in 2025, the largest end-user category by a wide margin.

- Ambulatory surgery centers represent the fastest-growing end-user segment, advancing at a 9.1% CAGR as outpatient procedure volumes climb.

• By Region

- North America contributed 36.1% of global revenue in 2025, led by U.S. hospital capital expenditure cycles.

- Asia-Pacific is set to outpace all regions at a 9.5% CAGR between 2026 and 2035, reflecting government healthcare infrastructure programs across China and India.

Market Size and Forecast (2021–2035)

Market Research Future's estimates combine primary surveys of 280+ CSSD managers, procurement directors, and sterilization service providers with secondary analysis from regulatory filings, trade association data, and company financials. Historical figures (2021–2024) are calibrated against import–export databases and installed-base audits; forecast values (2026–2035) reflect a bottom-up build from equipment shipment projections, replacement cycles, and new-facility pipeline analysis.