Stone Paper Market Summary

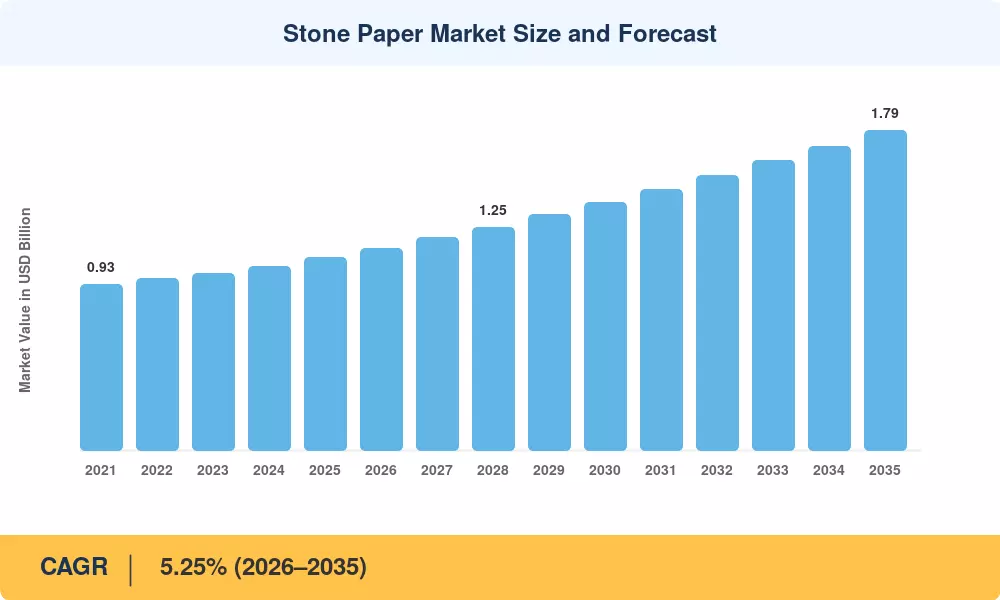

The Stone Paper Market was valued at USD 1.08 Billion in 2025 and is projected to grow from USD 1.13 Billion in 2026 to USD 1.79 Billion by 2035, registering a CAGR of 5.25% during the forecast period (2026–2035). Government bans on single-use plastics across more than 90 nations, combined with binding corporate sustainability targets from major consumer brands, are creating a structural pull toward limestone-based substrates. The European Union's Single-Use Plastics Directive and India's 2022 ban on identified single-use plastic items have accelerated procurement shifts worth an estimated USD 400 million in redirected packaging spend through 2024 alone [1][2].

A generational transition is underway in the substrates industry. Legacy wood-pulp and petroleum-based films are ceding ground to calcium carbonate–polyethylene composites that require zero water, zero tree fiber, and significantly less energy to produce. TBM's LIMEX technology, which raised over USD 100 million in cumulative funding by early 2025, exemplifies how process innovation is unlocking food-contact approval, high-resolution printing compatibility, and barrier performance previously reserved for coated plastics [3][4].

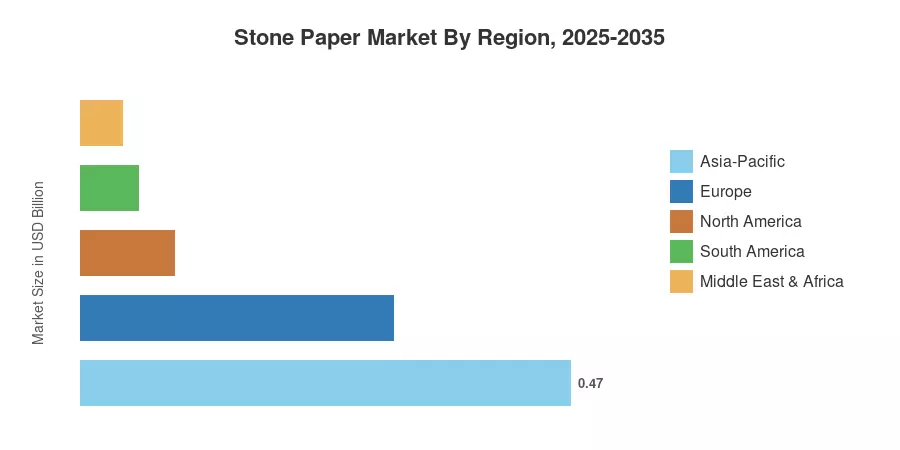

Asia-Pacific commands the dominant position in the Stone Paper Market with a 43.1% revenue share in 2025, driven by integrated limestone supply chains in China, Japan, and Taiwan. North America is the fastest-growing region at an 8.35% CAGR through 2035, propelled by retailer mandates for plastic-free packaging and federal procurement guidelines favoring recycled-content substrates. Europe holds the second-largest share at 27.5%, anchored by circular-economy regulations and brand-led packaging redesign programs. As production capacity scales across emerging markets and brand conversion timelines compress, the Stone Paper Market is positioned for sustained expansion well into the next decade.

Key Report Takeaways

• By Type

- Rich Mineral Paper Double Coated (RPD) accounted for 43.0% of Stone Paper Market share in 2025, driven by superior printability and moisture resistance for consumer packaging.

- Rich Mineral Paper Single Coated is projected to grow at a 7.2% CAGR through 2035, gaining traction in label and tag applications.

• By Application

- Packaging held 41.0% of the Stone Paper Market in 2025, reflecting brand-level commitments to eliminate conventional plastic wraps.

- Industrial labels and tags are forecast to achieve the fastest application-level CAGR at 8.2% through 2035.

• By End-User Industry

- Food and beverage represented 30.1% of the Stone Paper Market in 2025, underpinned by food-contact certifications for limestone composites.

- Retail and e-commerce is the fastest-growing end-user segment at a 9.4% CAGR, as direct-to-consumer brands adopt plastic-free mailer solutions.

• By Region

- Asia-Pacific held a 43.1% revenue share of the Stone Paper Market in 2025.

- North America is projected to grow at an 8.35% CAGR over 2026–2035.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework integrates primary interviews with over 120 industry stakeholders, trade-level shipment data, regulatory filings, and bottom-up capacity modeling across 28 countries. Historical figures reflect confirmed production volumes; forecast values apply the calibrated 5.25% CAGR alongside scenario adjustments for policy shifts and capacity ramp-ups in the Stone Paper Market.