Structural Adhesives Market Summary

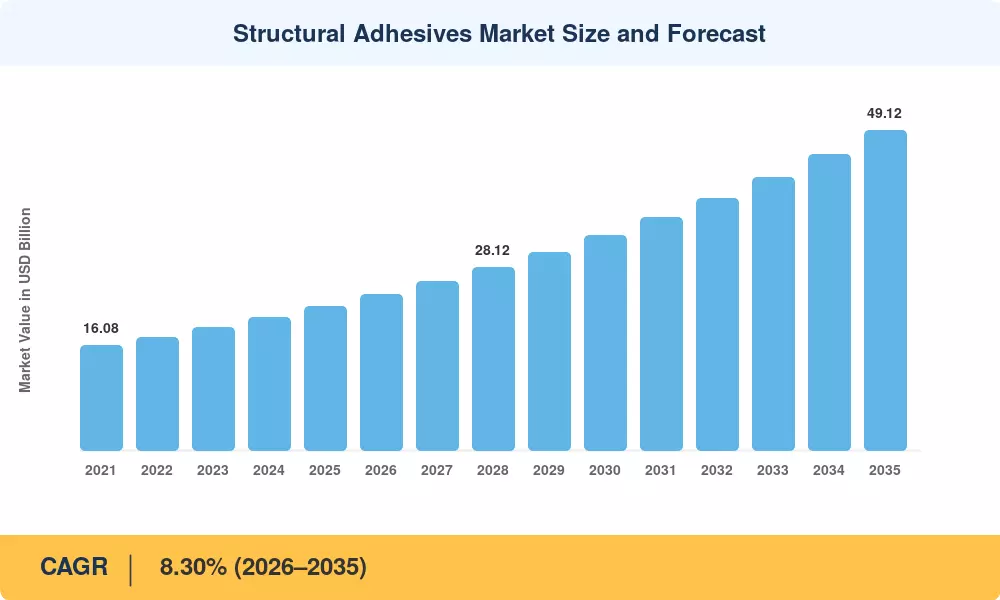

The Structural Adhesives Market reached an estimated USD 22.14 billion in 2025 and is projected to grow from USD 23.98 Billion in 2026 to USD 49.12 billion by 2035, registering a CAGR of 8.30% during the forecast period (2026–2035). This expansion is anchored in aggressive lightweighting mandates across automotive and aerospace sectors, where high-strength adhesives are replacing traditional mechanical fasteners to reduce vehicle and aircraft weight by 15–25%. The European Union's CO₂ emission targets for passenger vehicles — capped at 93.6 g/km by 2025 — have accelerated OEM adoption of epoxy structural adhesives and polyurethane adhesives for body-in-white assemblies [2].

The structural adhesives market is undergoing a significant technological transition. Engineering adhesive methods that attach incompatible materials—such as carbon fiber to aluminum and composites to steel—without thermal distortion are replacing outdated riveting, welding, and bolted-joint technologies. Between 2022 and 2024, Boeing and Airbus combined invested more than USD 4.2 billion in research and development for composite bonding materials, demonstrating the industry's dedication to next-generation airframes [3]. The capabilities of industrial bonding materials in high-stress applications are being further pushed by self-healing adhesive chemistries and UV-curable formulations.

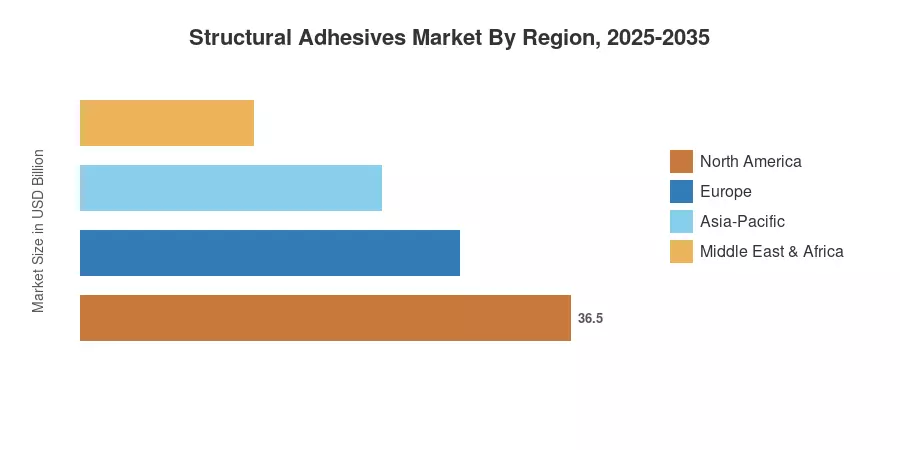

Due to China's construction boom and India's growing automobile production, the Asia-Pacific accounts for around 43% of the world's structural adhesives market revenue. At roughly 9.4%, the region also has the fastest CAGR. With a 23% stake, North America is the second-largest area, helped by the US aerospace industry and infrastructure restoration initiatives. Due to strict environmental rules that prioritize long-lasting adhesive compounds over mechanical attachment, Europe accounts for about 22% of the total. Automotive bonding adhesives and construction adhesive solutions will change the competitive landscape in every region over the course of the next ten years.

Key Report Takeaways

• By Resin Type

- Epoxy resin adhesives dominate the Structural Adhesives Market with approximately 38% revenue share in 2025, benefiting from unmatched load-bearing adhesives performance in aerospace and wind energy applications.

- Polyurethane adhesives represent the fastest-growing resin segment at an estimated 9.1% CAGR through 2035, fueled by demand for flexible industrial bonding materials in automotive assembly.

- Acrylic-based formulations hold a Structural Adhesives Market value of approximately USD 3.76 Billion in 2025, gaining traction in electronics and marine applications.

• By End-User Industry

- The construction sector accounts for the largest end-user share at roughly 32%, as urbanization drives the adoption of construction adhesive solutions globally.

- Automotive bonding adhesives are projected to grow at 9.3% CAGR, the fastest among all end-user verticals, as EV platforms demand lightweight composite bonding materials.

• By Region

- Asia-Pacific leads the Structural Adhesives Market with a 43% share, anchored by infrastructure spending exceeding USD 1.3 billion annually across China and India.

- North America holds approximately USD 5.09 billion in 2025 market value, driven by defense aerospace and wind energy expansion.

- The Middle East & Africa region registers a projected CAGR of 7.8%, supported by mega construction projects in Saudi Arabia and the UAE.

Market Size and Forecast (2021–2035)

MRFR's market sizing methodology integrates bottom-up revenue estimation from manufacturer filings and distributor data with top-down cross-validation using end-user industry consumption volumes. Historical figures (2021–2024) are derived from audited company reports, trade association data, and customs records. Forecast values (2026–2035) apply a calibrated compound growth model validated against downstream demand indicators, including automotive production volumes, construction permits, and wind turbine installation rates[4].

.webp?v=1783930316)