Structured Cabling Market Summary

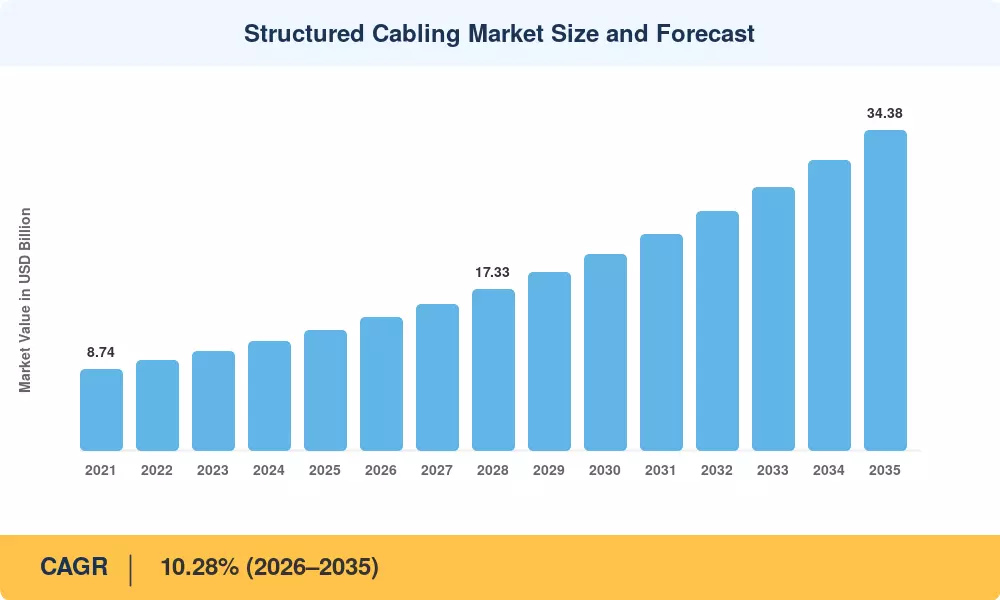

The Structured Cabling Market reached a valuation of USD 12.92 Billion in 2025 and is projected to climb from USD 14.25 Billion in 2026 to USD 34.38 Billion by 2035, registering a CAGR of 10.28% across the forecast window. Hyperscale data center construction programs — backed by over USD 220 Billion in announced AI infrastructure commitments through 2028 [2] — are pushing demand for high-density network cabling infrastructure and fiber optic cabling solutions to levels the industry has not seen before. Government broadband initiatives in Europe, India, and sub-Saharan Africa add a second policy-backed demand layer that reinforces long-range growth.

A generational technology shift is remaking the Structured Cabling Market from the inside. Legacy Cat 5e copper backbones installed during the 2010s expansion cycle are being ripped out and replaced with Cat 6A and single-mode fiber trunks capable of supporting 400G and 800G switch fabrics. Power over Ethernet delivery now extends to lighting, access control, and building-automation endpoints, turning passive patch panel cabling into active infrastructure. The U.S. CHIPS and Science Act and the EU Digital Decade program together funnel more than USD 85 billion toward digital infrastructure modernization [3], creating sustained procurement pipelines for data center cabling systems.

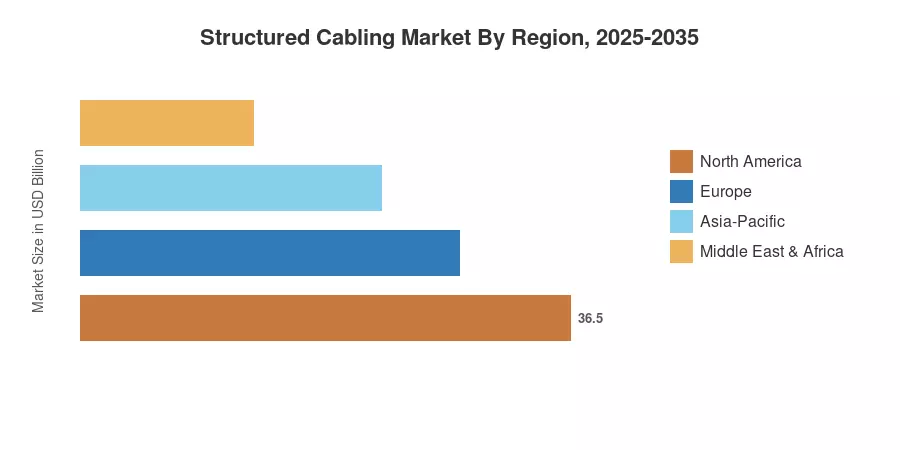

North America commands roughly 33.8% of the Structured Cabling Market, underpinned by cloud hyperscaler campuses in Virginia, Texas, and Oregon. Asia-Pacific follows with a 28.4% share, driven by aggressive fiber-to-the-room rollouts across China and India. The Middle East & Africa region, although smaller in absolute terms, registers the fastest CAGR of 11.32% as smart-city megaprojects in Saudi Arabia and the UAE accelerate demand for LAN wiring standards upgrades. Europe rounds out the picture at 23.6%, with sustainability-linked retrofit mandates boosting cable management systems spending.

Key Report Takeaways

• By Offering

- Hardware holds a 61.2% revenue share of the Structured Cabling Market in 2025, propelled by rack, panel, and fiber trunk purchases.

- Software solutions are expanding at a 10.74% CAGR through 2035, driven by AI-powered network cabling infrastructure monitoring platforms.

• By Cable Type

- Fiber optic cabling solutions captured 68.5% of revenue in 2025, reflecting the copper-to-fiber migration across enterprise and data center verticals.

• By Category

- Cat 8 cabling is projected to grow at an 11.52% CAGR from 2026 to 2035, the fastest among cable category standards, as 25G/40G server-to-switch links proliferate.

• By Application

- Data center cabling systems represent 48.2% of the Structured Cabling Market demand in 2025.

• By End User

- Manufacturing end users post the highest CAGR of 11.73%, fueled by Industry 4.0 and deterministic Ethernet deployments.

• By Region

- North America leads the Structured Cabling Market with 33.8% share, followed by Asia-Pacific at 28.4%.

- The Middle East & Africa region grows at an 11.32% CAGR, outpacing all other geographies through 2035.

Market Size and Forecast (2021–2035)

Market sizing combines bottom-up component shipment analysis with top-down macroeconomic modeling. Market Research Future (MRFR) triangulates vendor revenues, import/export databases, and end-user procurement disclosures to produce the forecasts below.