Sulfuric Acid Market Summary

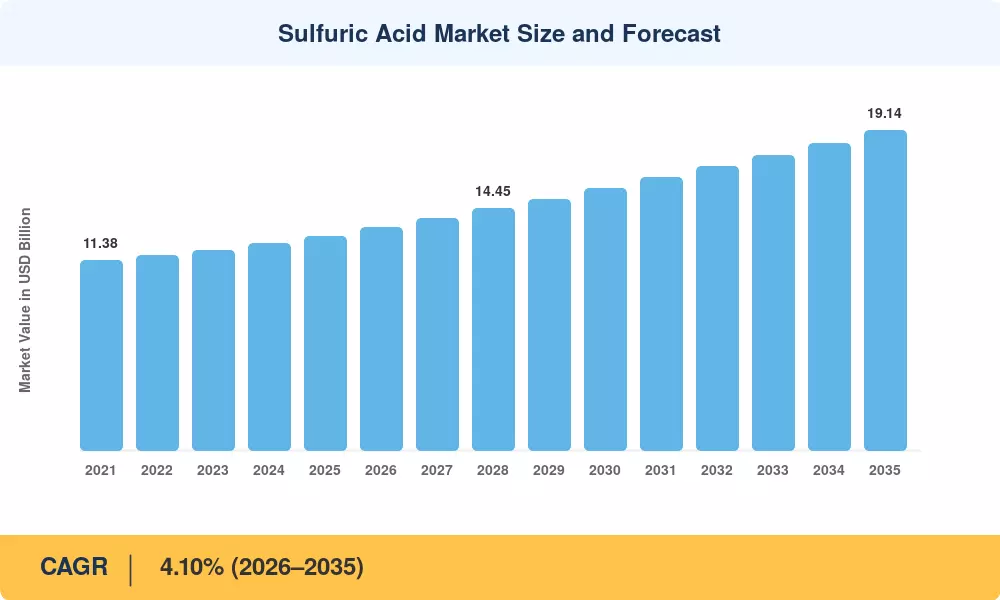

The Sulfuric Acid Market reached an estimated USD 12.80 billion in 2025 and is projected to grow from USD 13.33 billion in 2026 to USD 19.14 billion by 2035, registering a CAGR of 4.10% during the forecast period. Global food-security mandates and aggressive phosphate fertilizer expansion programs across South Asia and North Africa underpin this trajectory, with India's National Mission for Sustainable Agriculture and Morocco's OCP capacity-doubling initiative channeling billions into fertilizer production chemicals that rely on a steady sulfuric acid supply[2].

A structural transformation is reshaping the Sulfuric Acid Market as legacy single-contact acid plants give way to advanced double-contact double-absorption (DCDA) units equipped with real-time digital process controls. Capital commitments exceeding USD 4.2 billion in DCDA retrofit projects between 2023 and 2028 reflect tightening SO₂ emission limits under the EU Industrial Emissions Directive and China's Ultra-Low Emission Standards [3][4]. These upgrades cut tail-gas sulfur dioxide by over 99.7%, simultaneously lowering energy intensity and improving acid-grade consistency for downstream chemical processing acids and battery acid materials.

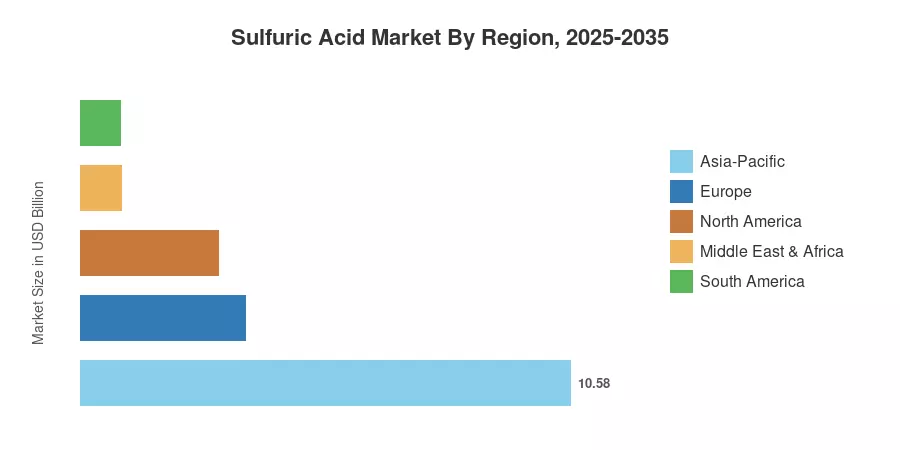

Asia-Pacific commands roughly 55.3% of the Sulfuric Acid Market, driven by China's integrated smelter-acid complexes and India's expanding fertilizer corridors. The region also posts the fastest CAGR at 4.35% through 2035. Europe holds the second-largest share at approximately 18.6%, bolstered by circular-economy mandates that incentivize acid recovery from metal processing chemicals and spent refinery chemical products. North America's shale-linked sulfur recovery keeps supply competitive, while emerging capacity in the Middle East and Africa positions the Sulfuric Acid Market for accelerating geographic diversification through the early 2030s.

Key Report Takeaways

• By Raw Material

- Elemental sulfur accounted for 72.9% of the Sulfuric Acid Market in 2025, reflecting integrated supply chains between oil refinery desulfurization units and downstream acid plants.

- Pyrite ore feedstock is forecast to register a 4.52% CAGR through 2035, supported by renewed interest in polymetallic mining chemical solutions across Central Asia.

• By Production Process

- The DCDA route captured 83.1% share of the Sulfuric Acid Market in 2025, driven by stringent environmental regulations and superior conversion efficiency.

- Single-contact plants remain relevant in cost-sensitive emerging markets, contributing USD 2.24 billion in 2025.

• By End-User Industry

- Fertilizer applications dominated with 61.2% of the Sulfuric Acid Market revenue in 2025, anchored by phosphoric acid production for DAP and MAP fertilizers.

- Chemical and pharmaceutical end users are projected to advance at the highest CAGR of 4.67% through 2035.

• By Region

- Asia-Pacific led with 55.3% of the global Sulfuric Acid Market share in 2025.

- North America is forecast to reach USD 2.98 billion by 2035, propelled by recovered sulfur streams from shale-gas processing and growing demand for battery acid materials.

Market Size and Forecast (2021–2035)

MRFR employs a bottom-up estimation methodology combining production-capacity utilization data from national chemical associations, trade-flow analysis from UN Comtrade, and company-level revenue disclosures. Historical figures (2021–2024) reflect actual industry outcomes adjusted for inventory swings, while forecast values (2026–2035) are derived from segment-level demand modeling calibrated against macroeconomic and regulatory scenarios[5].