Surge Arrester Market Summary

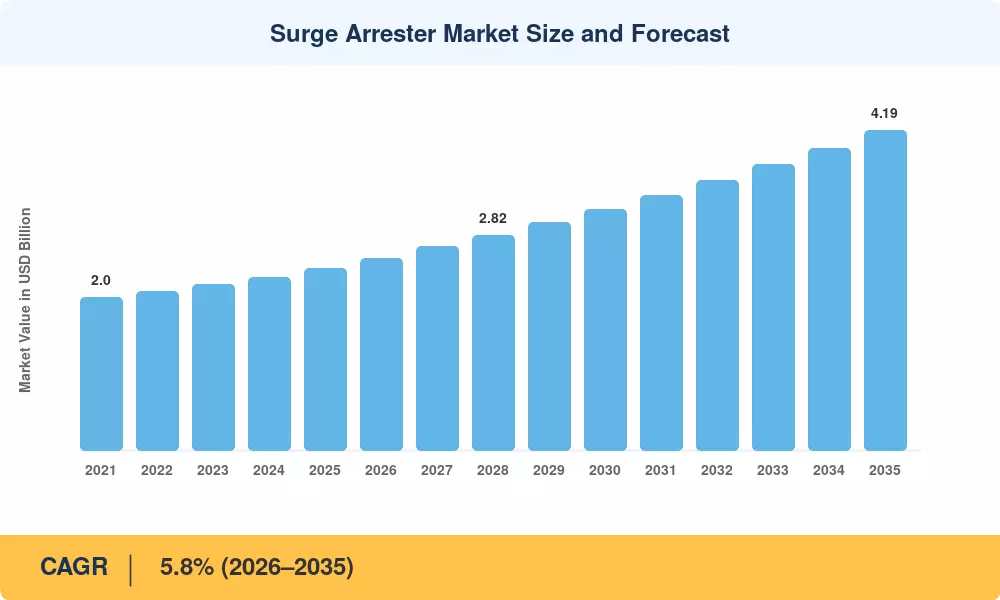

The global Surge Arrester Market reached an estimated USD 2.38 billion in 2025 and is projected to grow from USD 2.52 billion in 2026 to USD 4.19 billion by 2035, registering a CAGR of 5.8% during the forecast period (2026–2035). Two forces are pulling investment into this space simultaneously: grid modernization mandates in mature economies and electrification buildouts across developing nations. The U.S. Department of Energy's Grid Resilience and Innovation Partnerships (GRIP) program alone has committed over USD 10.5 billion toward hardening transmission and distribution infrastructure, a significant share of which flows directly into overvoltage protection equipment [1].

A generational technology shift is reshaping the Surge Arrester Market. Legacy porcelain-housed arresters — long the default across utility substations — are steadily giving way to polymeric-housed units that weigh less, resist vandalism, and survive seismic events better. Metal oxide varistor MOV surge arrester technology has become the de facto standard across voltage classes, displacing older silicon carbide designs. China's State Grid Corporation invested roughly USD 40 billion in ultra-high-voltage corridors during 2022–2024, each corridor requiring thousands of station-class and line-class arresters rated at 500 kV and above [2].

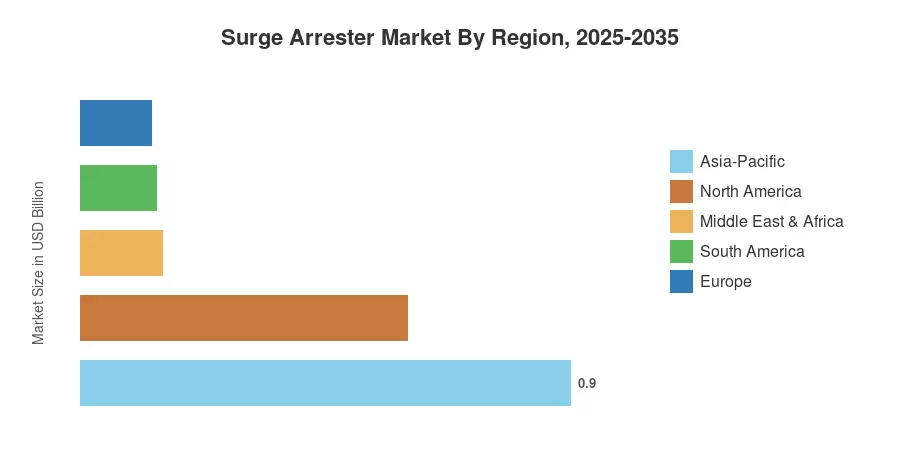

Asia-Pacific commands approximately 38% of the Surge Arrester Market, driven by massive grid expansion in China, India, and Southeast Asia. The region also posts the fastest growth at a CAGR of 6.9% through 2035. North America holds the second-largest share at roughly 25%, underpinned by utility replacement cycles and renewable interconnection projects. Europe accounts for about 22%, where offshore wind farm connections and cross-border HVDC links are catalyzing fresh arrester procurement. As grids become more complex and weather-related outages intensify, surge protection spending will remain structurally elevated well into the 2030s.

Key Report Takeaways

• By Type

- Polymeric-housed arresters dominate the Surge Arrester Market with approximately 58% revenue share, reflecting utility preference for lighter, explosion-resistant designs.

- Porcelain-housed arresters are growing at a CAGR of 3.2%, sustained by replacement demand in legacy substation fleets across North America and Europe.

• By Voltage Class

- High-voltage (72.5 kV–245 kV) arresters represent approximately USD 0.78 billion in 2025, anchored by transmission-line protection programs.

- Medium-voltage (1 kV–72.5 kV) arresters are expanding at a CAGR of 6.4%, fueled by urban distribution network upgrades.

• By Region

- Asia-Pacific leads the Surge Arrester Market with a 38% share, propelled by State Grid, Power Grid Corporation of India, and ASEAN electrification plans.

- Middle East & Africa is the second-fastest-growing region at a CAGR of 6.3%, driven by Gulf Cooperation Council grid interconnection projects.

Surge Arrester Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining top-down revenue analysis from publicly listed surge arrester manufacturers, bottom-up capacity and shipment tracking across voltage classes, and cross-validation against utility capital expenditure disclosures from FERC, CERC, and ENTSO-E filings. Historical figures (2021–2024) reflect reported revenues; the base year (2025) incorporates preliminary shipment data and backlog estimates.