Surgical Stapler Market Summary

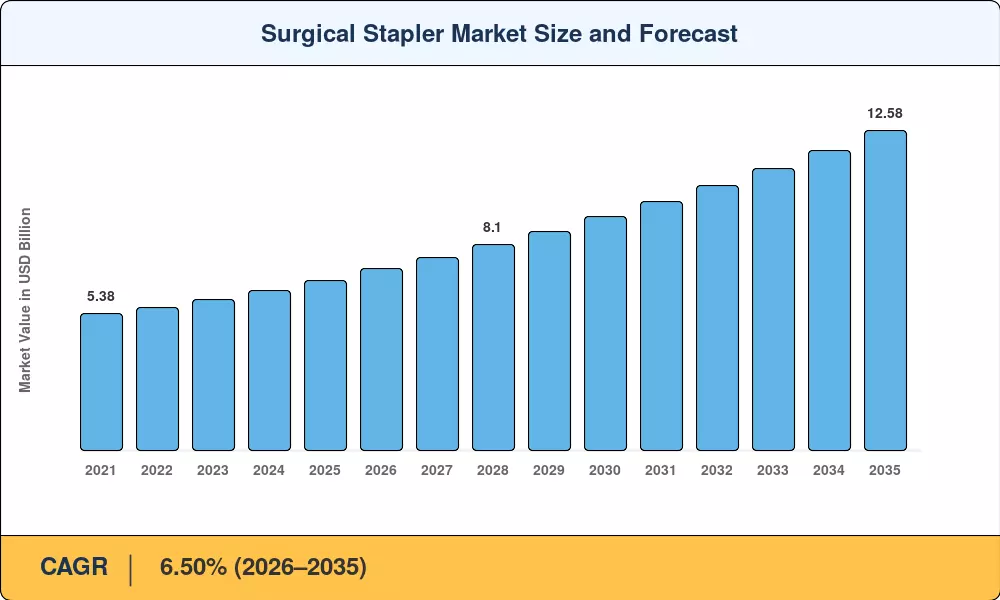

The Global Surgical Staplers Market size was valued at USD 6.68 Billion in 2025, and the market is projected to grow from USD 7.14 Billion in 2026 to USD 12.58 Billion by 2035, registering a CAGR of 6.50% during the forecast period 2026–2035. Robotic surgery platform adoption across major hospital networks and the conversion of manual stapling devices to sensor-equipped powered formats are the twin engines driving this expansion [1]. Multi-year capital contracts that bundle staplers with robotic consoles have reshaped procurement cycles, pushing hospitals toward higher-value device ecosystems.

The Surgical Staplers Market is transitioning from old mechanical firing mechanisms to powered platforms that incorporate real-time tissue-sensing algorithms. Intuitive Surgical said that its robotic platform stapling sales exceeded $1.8 Billion in fiscal 2024 with double-digit procedure growth [1]. ESG rules are dragging reusable handle systems into competitive tenders, as infection-control specialists defend single-use operations.

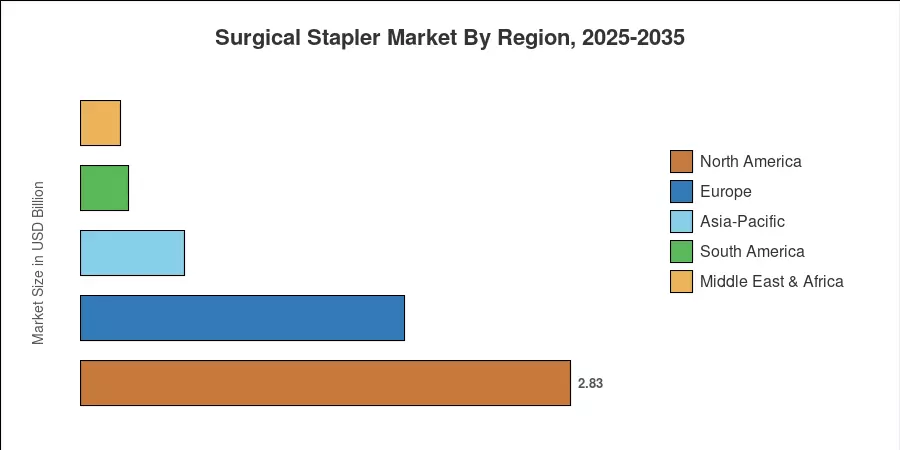

North America held a share of 42.3% of the Surgical Staplers Market in 2025, due to the increasing prevalence of robotic surgery and supportive reimbursement policies. The Asia-Pacific region is expected to experience the fastest CAGR of 8.97% by 2035, driven by the growing hospital infrastructure in China and India. Europe captured the second-highest market share at over 28.0% on account of centralized procurement programs in Germany, France, and the UK. The next decade will reward companies that marry device performance with data traceability and sustainability credentials.

Key Report Takeaways — Surgical Staplers Market

By Product

- Linear staplers led the Surgical Staplers Market with a 42.5% revenue share in 2025, supported by broad adoption in open and thoracic procedures.

- Laparoscopic staplers are forecast to expand at a 9.52% CAGR through 2035, accelerated by minimally invasive surgery trends.

By Application

- Abdominal and gastrointestinal surgery accounted for a 43.1% revenue share in 2025 across the Surgical Staplers Market.

- Ambulatory surgical centers (ASCs) are recording the fastest end-user CAGR of 8.91% through 2035, absorbing high-volume orthopedic and bariatric cases.

By Geography

- North America captured 42.3% of the Surgical Staplers Market in 2025.

- Asia-Pacific is projected to record the highest regional CAGR of 8.97% through 2035.

Surgical Staplers Market Size and Forecast (2021–2035)

Market sizing is based on bottom-up revenue modeling across product categories and evaluated against business disclosures, hospital procurement databases and third-party benchmarks. The historical data (2021-2024) are actual distributor shipments, and the forecast period (2026-2035) is based on segment-weighted compound growth assumptions derived from surgical procedure volume projections [2].

.webp?v=1781875474)