Synthetic Biology Market Summary

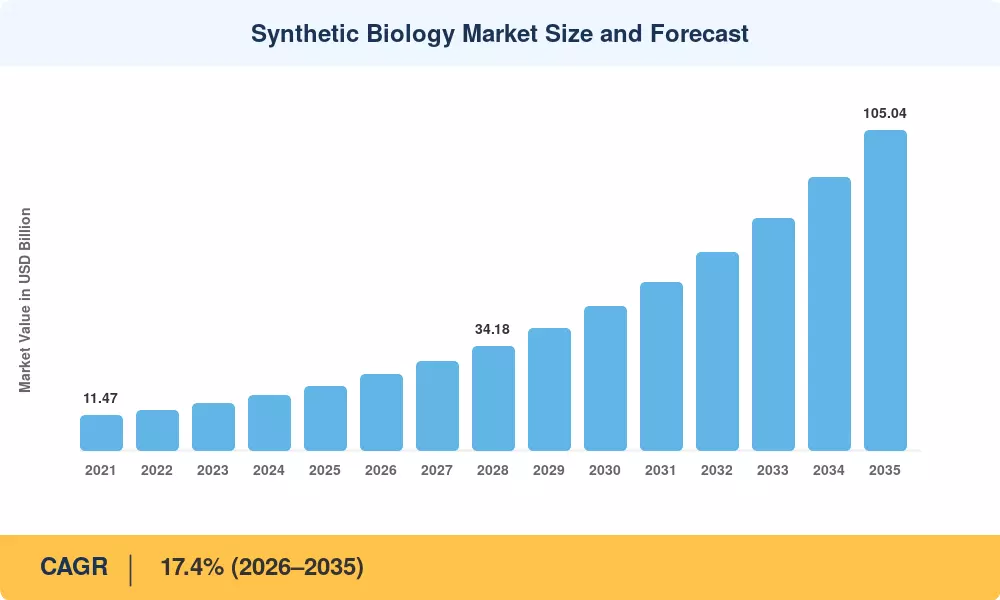

The global Synthetic Biology Market reached USD 21.12 Billion in 2025 and is projected to grow from USD 24.80 Billion in 2026 to USD 105.04 Billion by 2035, registering a CAGR of 17.4% over the forecast period (2026–2035). This trajectory reflects two powerful catalysts: the U.S. Executive Order on Advancing Biotechnology and Biomanufacturing Innovation, which earmarked over USD 2 billion in federal funding for bio-based production capacity [1], and the European Union's updated Horizon Europe work program directing EUR 1.8 billion toward sustainable bio-economy initiatives through 2027 [2]. Taken together, these policy commitments have transformed the Synthetic Biology Market from a research-intensive niche into a scalable industrial platform.

The technology landscape is undergoing a generational shift. Legacy cloning workflows and manual strain-optimization cycles are giving way to AI-guided protein design, automated DNA assembly, and cloud-connected bioreactor networks. Corporate investments in cell-free systems and high-throughput screening have compressed development timelines from years to months. Illumina and partners have driven gene-synthesis costs below USD 0.05 per base pair as of mid-2024, removing a longstanding bottleneck for commercial-scale applications [3]. This cost deflation has opened addressable markets in precision fermentation, bio-based materials, and next-generation therapeutics that were previously uneconomical.

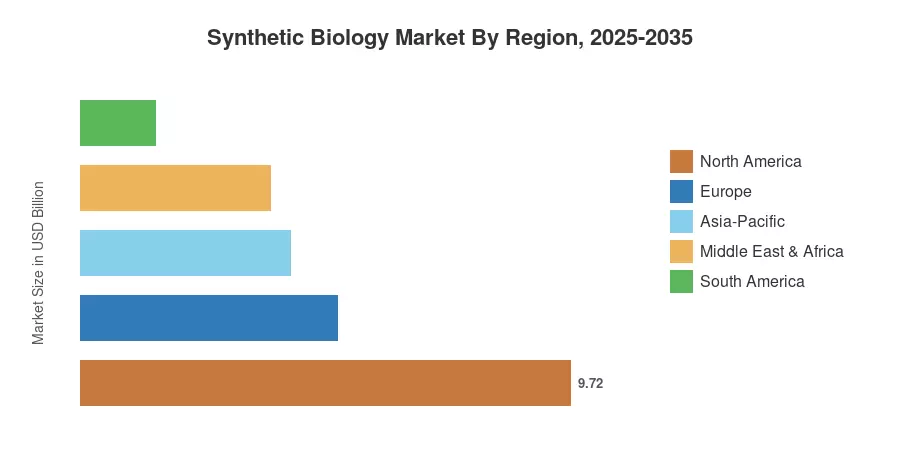

North America commands approximately 46.0% of the Synthetic Biology Market, anchored by a dense cluster of biofoundries and venture-backed startups across Boston, the San Francisco Bay Area, and Research Triangle Park. Asia-Pacific is the fastest-growing region at a projected 19.7% CAGR, driven by aggressive government bio-economy roadmaps in China, India, and South Korea. Europe holds the second-largest share at roughly 24.1%, with strong regulatory frameworks accelerating approval pathways for bio-based chemicals and food ingredients. As public and private capital continue to converge, the Synthetic Biology Market is poised for sustained double-digit expansion through the mid-2030s.

Key Report Takeaways

• By Product

- Core Products held a dominant revenue share of 51.2% in the Synthetic Biology Market in 2025, driven by sustained demand for oligonucleotides, synthetic genes, and chassis organisms across pharmaceutical R&D pipelines.

- Enabling Products are forecast to expand at an 18.1% CAGR through 2035, as automated DNA assembly platforms and next-generation sequencing kits lower barriers for mid-size biotech firms.

• By Technology

- Genome Engineering captured 35.4% of market share in 2025, reflecting the widespread commercial deployment of CRISPR-Cas9 and base-editing platforms across therapeutic and agricultural applications.

- Bioinformatics & CAD Tools are advancing at a 17.8% CAGR, fueled by the integration of machine-learning algorithms into pathway design and strain optimization workflows.

• By Application

- Healthcare accounted for 57.1% of the Synthetic Biology Market in 2025, with cell and gene therapies, mRNA vaccine platforms, and engineered probiotics as the primary growth vectors.

- Food & Agriculture is set to rise at a 16.9% CAGR between 2026 and 2035, as precision fermentation and alternative protein platforms gain regulatory clearance in major markets.

• By End User

- Industrial Biotech Companies commanded a 41.4% share of the Synthetic Biology Market in 2025, reflecting their role as the primary buyers of synthetic DNA, enzymes, and bio-process optimization services.

- Defense & Government Labs are growing fastest at a 17.5% CAGR, propelled by biosecurity mandates and government-funded biomanufacturing programs.

• By Region

- North America led with 46.0% market share in 2025, supported by deep venture capital pools and a mature regulatory infrastructure for genetically modified organisms.

- Asia-Pacific is expanding most rapidly at a 19.7% CAGR, with China's 14th Five-Year Plan for Bio-Economy and India's BioE3 policy initiative serving as primary accelerants.

Synthetic Biology Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from audited financial disclosures of leading synthetic biology companies, patent filings, and government R&D expenditure databases. Forecast projections incorporate bottom-up revenue modeling across product, technology, and application segments, cross-validated against macroeconomic indicators and primary interviews with over 120 industry executives and academic researchers.