Tattoo Removal Market Summary

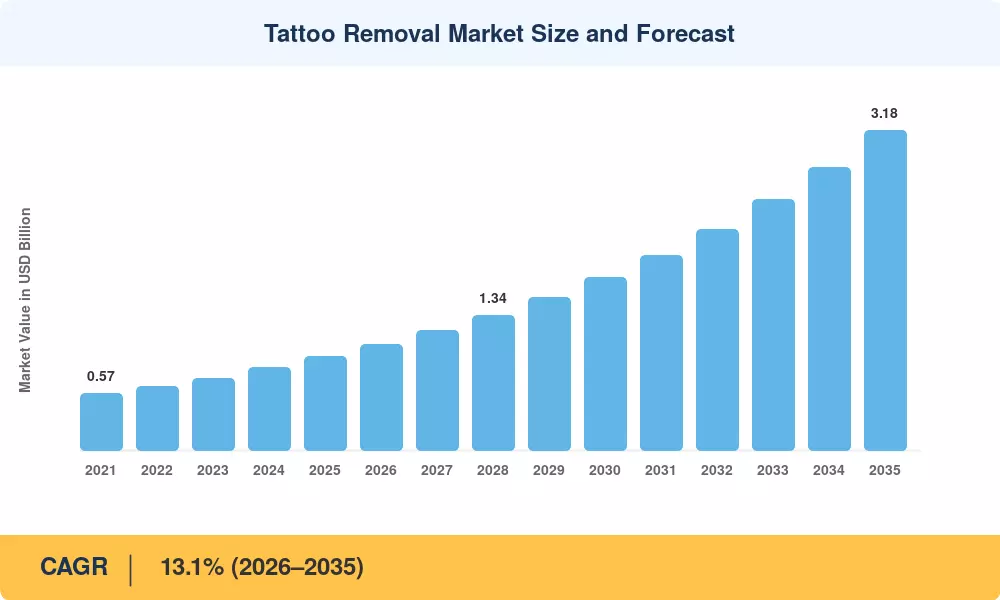

The Global Tattoo Removal Market size was valued at USD 0.93 Billion in 2025, and the market is projected to grow from USD 1.05 Billion in 2026 to USD 3.18 Billion by 2035, registering a CAGR of 13.1% during the forecast period 2026–2035. Shifting consumer preferences toward reversible body art, stricter corporate appearance policies across finance and healthcare sectors, and rising medical-aesthetic expenditures are converging to fuel this expansion. The US FDA's ongoing scrutiny of tattoo ink formulations under the Modernization of Cosmetics Regulation Act (MoCRA) has redirected consumers toward professional clinic-based removal rather than unregulated at-home solutions [2].

The market for tattoo removal is undergoing a technological revolution as cutting-edge picosecond laser dermatology platforms replace outdated Q-switched laser treatment systems. By delivering ultra-short pulse durations that break down ink pigment into tiny particles, these more recent devices reduce the average number of treatment sessions from ten to five or fewer. Over USD 280 million was invested globally in laser tattoo eradication hardware in 2024, with venture-backed clinic chains contributing over 35% of that total. An estimated 12% of Europeans with tattoos are being forced to undergo skin tattoo fading procedures as a result of EU regulatory agencies tightening ink-ingredient limitations under REACH Annex XVII, which went into effect in January 2022 and was expanded in 2024 [4].

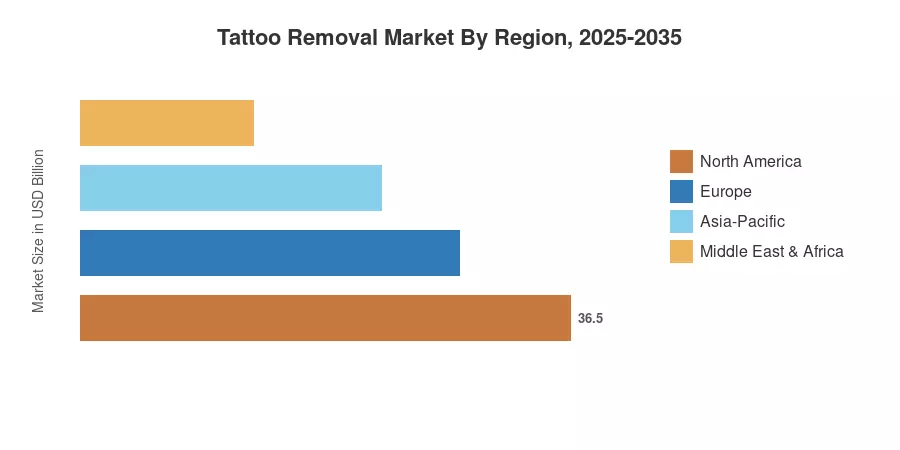

Due to broad insurance-adjacent financing alternatives and high per-capita spending on cosmetic procedures, North America holds the greatest share of the tattoo removal market, accounting for about 43.2% of 2025 revenue. With a predicted CAGR of 14.8% through 2035, Asia-Pacific is the fastest-growing area, driven by rising disposable incomes in China, South Korea, and India. Europe has the second-largest proportion, at about 28%, thanks to a developing network of dermatology clinics and stricter ink safety laws Continued advancements in picosecond laser dermatology and growing clinic footprints throughout emerging nations should help the tattoo removal market in the coming ten years.

Key Report Takeaways

• By Device

- Laser devices accounted for 68.5% of the Tattoo Removal Market revenue in 2025, reflecting the dominance of Q-switched laser treatment and newer picosecond platforms in clinical practice

- High-intensity focused ultrasound (HIFU) devices are forecast to grow at a 14.4% CAGR through 2035, driven by demand for non-invasive skin tattoo fading procedures

- Radio-frequency devices contributed USD 0.08 Billion in 2025, gaining traction in combination therapy protocols alongside laser tattoo erasure systems

• By End User

- Dermatology and aesthetic clinics led the Tattoo Removal Market with 43.5% revenue share in 2025

- Medical spas are projected to expand at a 14.9% CAGR to 2035, capitalizing on the consumer shift toward lifestyle-oriented ink pigment breakdown treatments

• By Geography

- North America held 43.2% of the global Tattoo Removal Market share in 2025

- Asia-Pacific is anticipated to register the fastest CAGR of 14.8% between 2026 and 2035, with picosecond laser dermatology adoption surging across South Korea and China

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from device manufacturers, clinic-level billing data, and proprietary primary surveys of dermatologists and medical-spa operators across 32 countries. Historical figures (2021–2024) are validated against company filings and insurance reimbursement databases, while forecast estimates apply a compound growth model calibrated to procedure-volume trends and technology replacement cycles.