Textile Dyes Market Summary

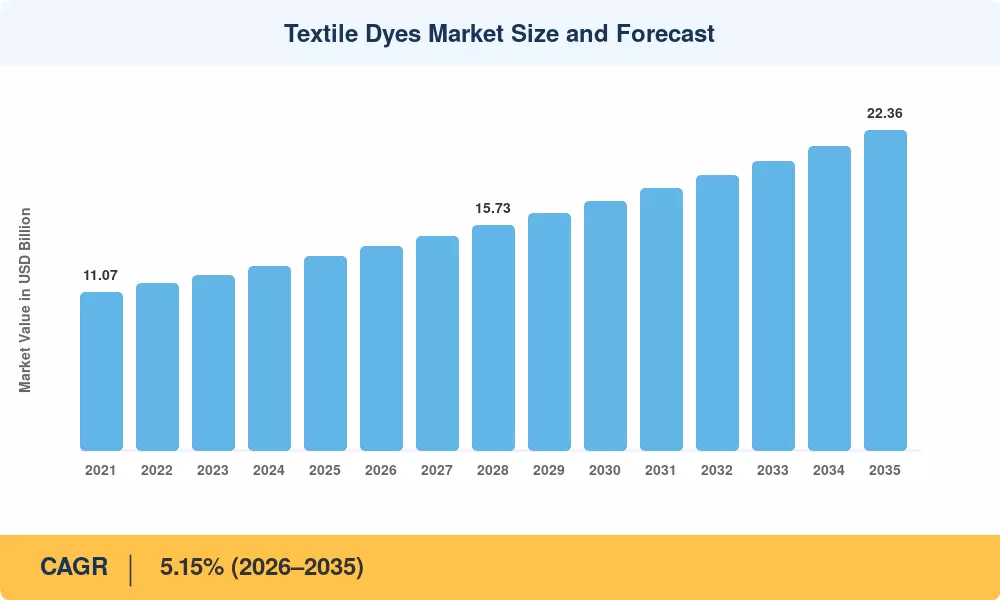

The Textile Dyes Market reached USD 13.53 Billion in 2025 and is projected to grow from USD 14.23 Billion in 2026 to USD 22.36 Billion by 2035, registering a compound annual growth rate of 5.15% during the 2026–2035 forecast window. Two structural forces anchor this trajectory: the European Union's revised Industrial Emissions Directive, which mandates a 30% reduction in textile-process effluent loads by 2030 [1], and cumulative FDI of over USD 4.2 billion flowing into dyeing-and-finishing capacity across Vietnam and India since 2022 [2]. Together, these policy and investment signals are pulling the Textile Dyes Market toward higher-value chemistries and cleaner processing pathways.

The world of technology is changing quickly. Digital inkjet platforms, which save water consumption by up to 60% per meter of fabric, are displacing conventional exhaust-dyeing systems, which have long been the industry's mainstay [3]. The demand for inkjet-compatible dispersive and reactive formulations has increased as a result of brands like Inditex and H&M Group committing over USD 1.8 billion in total to digital-ready supply chains through 2028 [4]. The competitive landscape of the textile dyes market is changing as a result of this shift, favoring manufacturers with robust R&D pipelines in high-purity, low-salt dye chemistries.

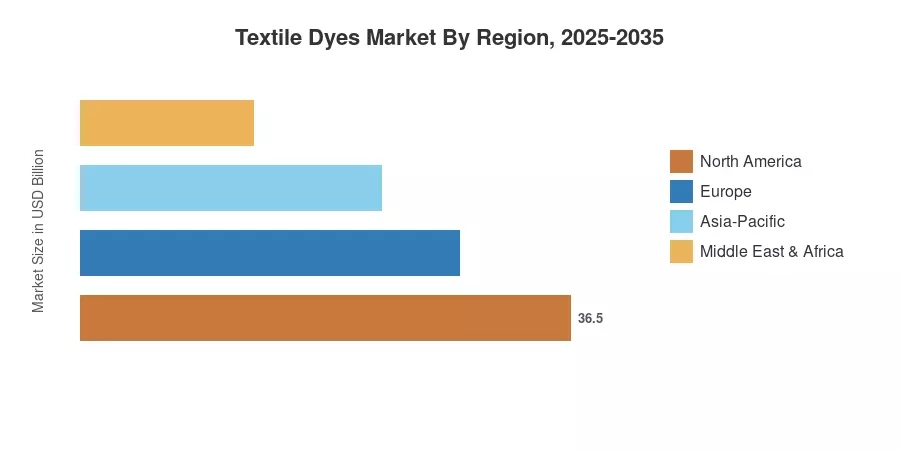

With the world's highest concentration of polyester fiber spinning and fabric finishing capacity in China and India, the Asia-Pacific region commands around 53.3% of the textile dyes market. Due to the need for high-end performance textiles and strict REACH compliance regulations, Europe is the second-largest source of revenue. With greenfield investments in Bangladesh, Indonesia, and southern Vietnam expected to extend the region's lead over the next ten years, the Asia-Pacific also has the fastest CAGR, 6.15% through 2035.

Key Report Takeaways

• By Dye Type

- Dispersive dyes hold a 34.4% revenue share in 2025, benefiting from polyester's dominance across fast-fashion and athleisure supply chains.

- Reactive dyes are expanding at a 5.08% CAGR through 2035, propelled by cellulosic-fiber blending trends in sustainable apparel.

• By Fiber Type

- Polyester accounts for 46.6% of the Textile Dyes Market in 2025, reflecting the fiber's cost advantage and lower water-to-dye ratios.

- Cotton-directed dyes reached USD 3.78 billion in 2025, driven by organic-cotton adoption across premium brands.

• By Application

- Apparel leads with 51.4% of the Textile Dyes Market share in 2025.

- Industrial fabrics record a 5.72% CAGR through 2035, fuelled by automotive-interior and protective-clothing specifications.

• By Region

- Asia-Pacific captures 53.3% of the Textile Dyes Market in 2025.

- North America contributes USD 1.96 billion, with regulatory compliance standards sustaining demand for low-impact dye systems.

Textile Dyes Market Size and Forecast (2021–2035)

Market Research Future's size estimates blend bottom-up plant-level production audits, import-export customs data from ITC Trademap, company filings, and proprietary demand modeling calibrated against third-party benchmarks. Historical figures (2021–2024) are actuals; 2025 is the base-year estimate; 2026–2035 values are projections applying a 5.15% CAGR with annual adjustments for demand cyclicality.