Thin Client Market Summary

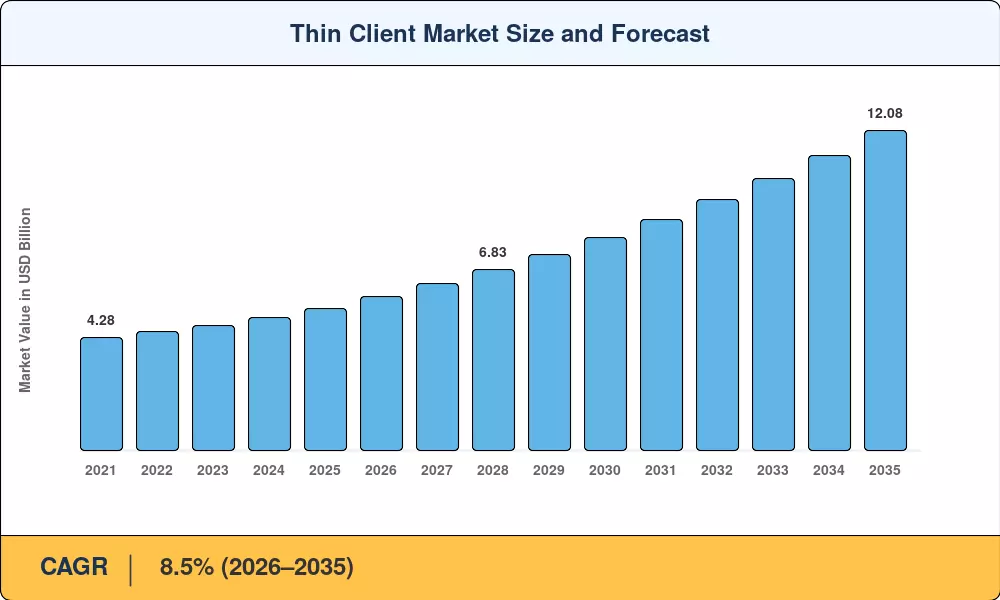

The Thin Client Market was valued at USD 5.35 Billion in 2025 and is projected to expand from USD 5.80 Billion in 2026 to USD 12.08 Billion by 2035, registering a CAGR of 8.5% during the forecast period (2026–2035). Federal Executive Order 14028 and the Cybersecurity and Infrastructure Security Agency's zero-trust maturity model have accelerated secure endpoint procurement across U.S. government agencies and their private-sector supply chains [3][4]. Enterprises reallocating IT budgets under rising cyber-insurance premiums find centrally managed endpoints a pragmatic path to compliance and cost control.

Traditional fat-client desktops are being replaced by lightweight terminals that stream virtual desktop thin clients from public cloud platforms and centralized data centers. The rate at which businesses are shifting workloads away from local hardware is reflected in forecasts that global investment in virtual desktop infrastructure will surpass USD 9 billion in 2024 [6]. In order to reduce firmware attack surfaces and lower per-seat license costs, suppliers now incorporate hardware-agnostic operating systems, such as Linux-based and Chrome OS.

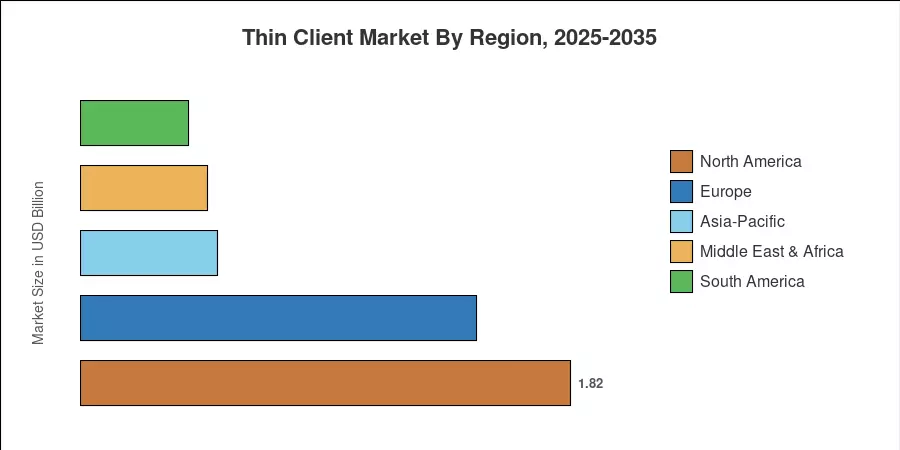

Due to corporate hybrid work budgets and federal zero-trust procurement, North America held the highest share of the thin client market in 2025. With a CAGR of 9.5% through 2035, Asia-Pacific is the fastest-growing market thanks to government digitalization initiatives in China, India, and ASEAN countries [12]. Due to the EU Cyber Resilience Act and scope-2 carbon reporting requirements that prioritize low-power endpoint devices, Europe is the second-largest area. The Thin Client Market's trajectory through 2035 is still steadily rising as global compliance demands and electricity prices rise.

Key Report Takeaways

• By Type

- Hardware commanded 57.6% of the Thin Client Market revenue in 2025, reflecting persistent demand for purpose-built endpoint terminals across enterprise and government estates.

- Software and services are forecast to grow at a 9.0% CAGR through 2035, fueled by subscription-based endpoint management platforms and managed desktop-as-a-service offerings.

• By End-User Industry

- IT and telecom held 26.5% of the Thin Client Market share in 2025, led by service-provider network operations centers and call-center deployments.

- Healthcare is advancing at a 9.8% CAGR through 2035, driven by HIPAA-compliant workstation mandates and electronic health-record modernization.

• By Geography

- North America generated 34.0% of global revenue in 2025, supported by federal zero-trust procurement timelines and corporate IT refresh cycles.

- Asia-Pacific exhibits the fastest trajectory at a 9.5% CAGR to 2035, with India's Digital India program and China's enterprise cloud push as primary catalysts.

Thin Client Market Size and Forecast (2021–2035)

Market sizing integrates primary research across 45+ enterprise IT procurement leaders, validated against vendor shipment data. Historical figures draw on public financial disclosures of leading hardware OEMs and channel distribution data. At the same time, forecast projections apply regression modeling anchored to enterprise endpoint refresh cycles, cloud adoption curves, and regulatory compliance timelines.