Topical Drug Delivery Market Summary

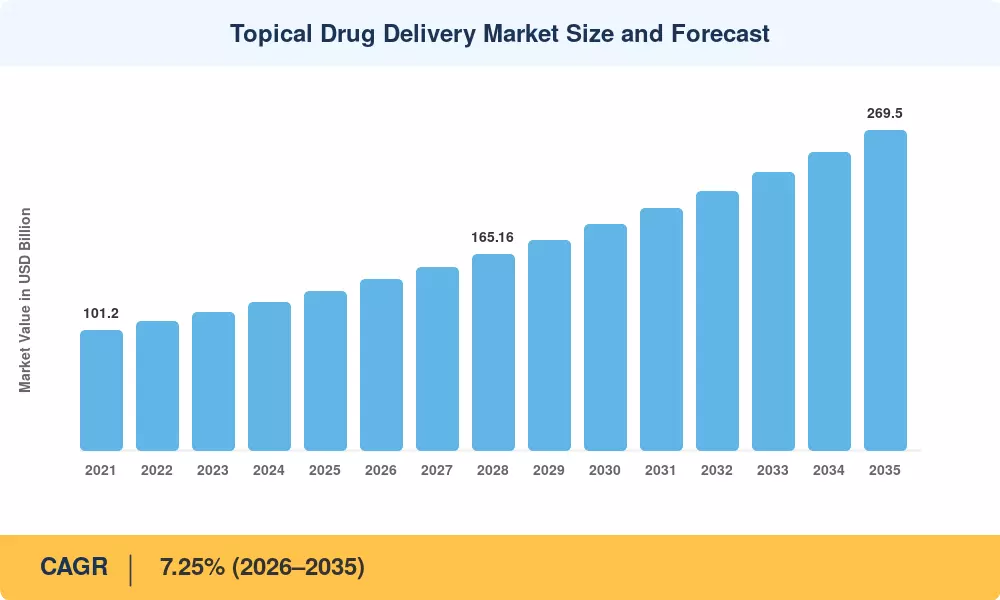

The Global Topical Drug Delivery Market size was valued at USD 133.90 Billion in 2025, and the market is projected to grow from USD 143.60 Billion in 2026 to USD 269.50 Billion by 2035, registering a CAGR of 7.25% during the forecast period 2026–2035. This trajectory is anchored in two mutually reinforcing catalysts: the U.S. FDA's expanded guidance on non-opioid analgesic approvals (finalized Q3 2024), which accelerated clearance timelines for transdermal drug absorption platforms, and the European Commission's EUR 1.2 Billion Horizon Europe cluster earmarked for advanced skin patch medication delivery technologies through 2027 [2][3]. Together, these policy signals have pulled forward corporate R&D timelines and attracted fresh venture capital into the sector.

A pronounced technology shift is reshaping the topical drug delivery market as conventional ointments and generic creams yield ground to precision-engineered delivery architectures. Microneedle arrays, nano-emulsion carriers, and sensor-enabled wearable patches are displacing first-generation topical cream formulation approaches that rely on passive diffusion alone. The global dermal permeation enhancement technology pipeline saw USD 4.8 Billion in cumulative private investment between 2022 and 2024, a figure that underscores the industry's confidence in next-generation platforms [4].

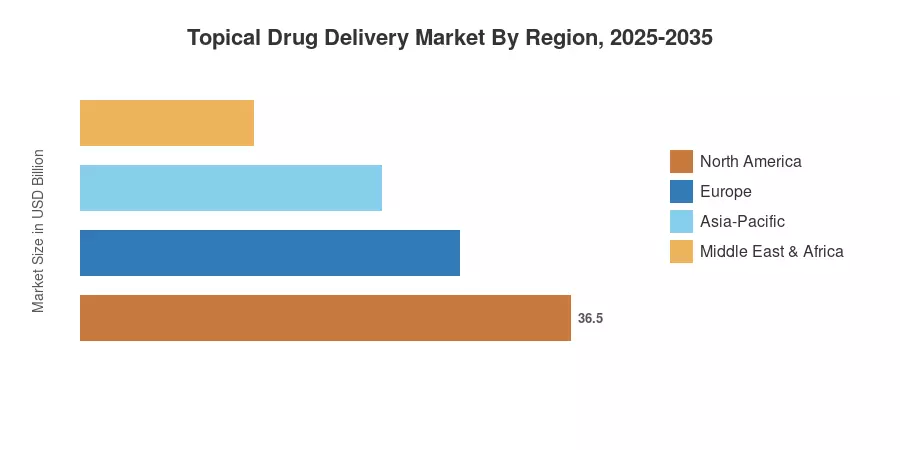

North America commands roughly 41.3% of the topical drug delivery market, buoyed by robust payer coverage for localized skin drug therapy and a dense clinical-trial infrastructure Asia-Pacific is the fastest-growing region at a projected CAGR near 9.90%, driven by expanding insurance pools in India, China, and Southeast Asia. Europe holds the second-largest share at approximately 27.5%, supported by harmonized EMA regulations that reward bioequivalence studies for topical generics [5]. As biologics and biosimilars increasingly enter topical pipelines, the next decade promises even sharper innovation cycles.

Key Report Takeaways

• By Route of Administration

- Dermal delivery held 48.2% of topical drug delivery market revenue in 2025, reflecting the dominance of creams, gels, and ointments in chronic dermatological care

- Nasal delivery is projected to advance at a 9.85% CAGR through 2035, fueled by migraine and CNS drug pipelines that leverage transdermal drug absorption pathways

• By Product

- Traditional formulations accounted for 75.6% of the topical drug delivery market in 2025, though their share is gradually contracting as device-based platforms gain traction

- The devices segment — including advanced skin patch medication delivery systems — is expanding at an 8.72% CAGR to 2035

• By Indication & End User

- Dermatology represented 45.4% of revenue in 2025, reinforcing its role as the primary therapeutic arena for topical cream formulation innovation

- Home-care settings are growing at a 9.68% CAGR, the fastest among end-user channels, as patients increasingly manage localized skin drug therapy outside hospital walls

• By Region

- North America dominated with 41.3% share; Asia-Pacific is set for the highest regional CAGR of 9.90% through 2035

Market Size and Forecast (2021–2035)

MRFR's market-sizing model triangulates top-down pharmaceutical revenue disclosures with bottom-up prescriber-volume data across 42 countries, validated against third-party syndicated databases and primary interviews with formulators, dermatologists, and supply-chain executives.

.webp?v=1782976095)