Transparent Conductive Films Market Summary

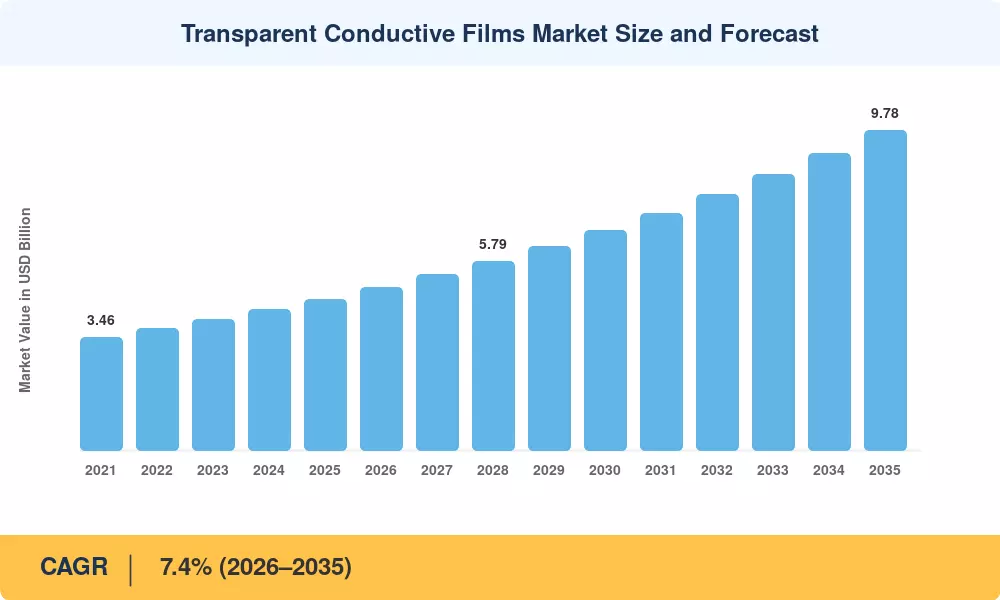

The Transparent Conductive Films Market reached an estimated USD 4.62 billion in 2025 and is projected to grow from USD 4.96 billion in 2026 to USD 9.78 billion by 2035, registering a CAGR of 7.4% during the forecast period (2026–2035). This expansion is anchored by accelerating consumer electronics demand and a global push toward renewable energy installations, with photovoltaic capacity additions surpassing 350 GW annually by 2024, according to the International Energy Agency [2]. Government incentives for solar manufacturing — including the U.S. Inflation Reduction Act's USD 7.5 billion in clean energy manufacturing credits — are pulling transparent electrode films into mainstream energy infrastructure at an unprecedented scale.

A significant technology transformation is reshaping the Transparent Conductive Films Market as legacy indium tin oxide (ITO) on glass substrates faces growing competition from flexible electronic materials such as silver nanowires and carbon nanotubes. These next-generation conductive coating films deliver comparable optical transmittance at lower costs and with superior mechanical flexibility, enabling applications in foldable smartphones, rollable displays, and wearable biosensors. BloombergNEF estimates that investment in advanced display technologies exceeded USD 28 billion in 2024 alone [3], driving rapid iteration across the conductive polymer films value chain.

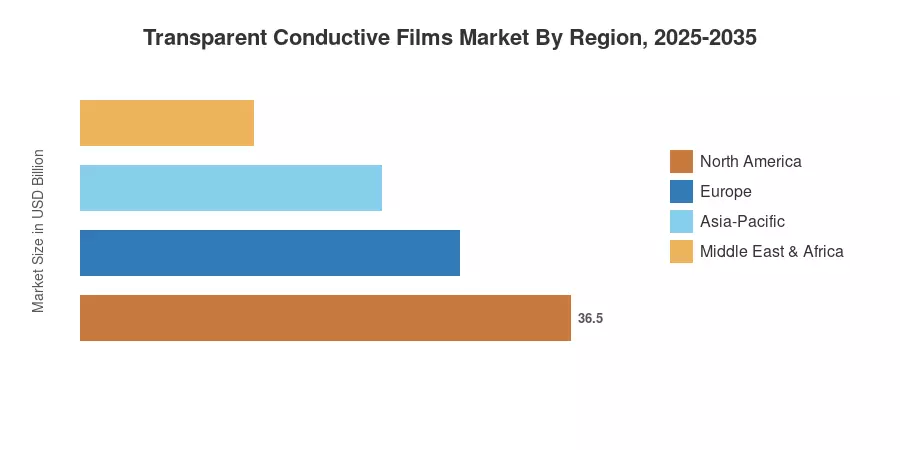

Asia-Pacific commands roughly 46% of the global Transparent Conductive Films Market, fueled by manufacturing density in China, South Korea, and Japan. The region also registers the fastest growth trajectory with a CAGR exceeding 8.1%, driven by the demand for touch screen films in consumer electronics hubs. North America holds approximately 22% share, propelled by photovoltaic expansion and smart display films adoption in automotive head-up displays. Europe accounts for about 19% of revenue, with optoelectronic materials demand rising steadily across automotive and building-integrated photovoltaic (BIPV) segments

Key Report Takeaways

• By Material Type

- Indium Tin Oxide (ITO) on PET holds approximately 34% share of the Transparent Conductive Films Market, sustained by high-volume touch screen films production for smartphones and tablets

- Silver nanowire films are growing at a CAGR of 11.2%, the fastest among all material segments, driven by demand for flexible electronic materials in foldable and rollable device architectures

- Conductive polymer films are projected to reach USD 0.74 billion by 2035, gaining traction in low-cost sensor and OLED lighting applications

• By Application

- Smartphones represent the largest application, valued at approximately USD 1.67 billion in 2025, reflecting sustained global handset production volumes

- The LCD and LED monitors and TVs segment is expanding at a 6.8% CAGR through 2035, supported by rising panel sizes and 8K resolution adoption requiring advanced conductive display materials

• By Region

- Asia-Pacific dominates the Transparent Conductive Films Market with 46% revenue share, reinforced by China's electronic conductive coatings manufacturing ecosystem

- North America is projected to grow at 7.0% CAGR, underpinned by photovoltaic installations and automotive transparent electrode films integration

- Europe accounts for approximately USD 0.88 billion in 2025, with Germany and France leading in BIPV and automotive smart display films deployment

Market Size and Forecast (2021–2035)

The market sizing methodology combines bottom-up revenue aggregation from manufacturer filings with top-down validation against industry shipment data from the Display Supply Chain Consultants (DSCC) and IEA photovoltaic deployment statistics. Historical figures (2021–2024) reflect actual revenues; 2025 represents the base-year estimate; and 2026–2035 projections apply the calibrated 7.4% CAGR with adjustments for anticipated demand inflections in foldable devices (2027–2029) and next-generation solar cells (2030–2033).