Ultra High Molecular Weight Polyethylene Market Summary

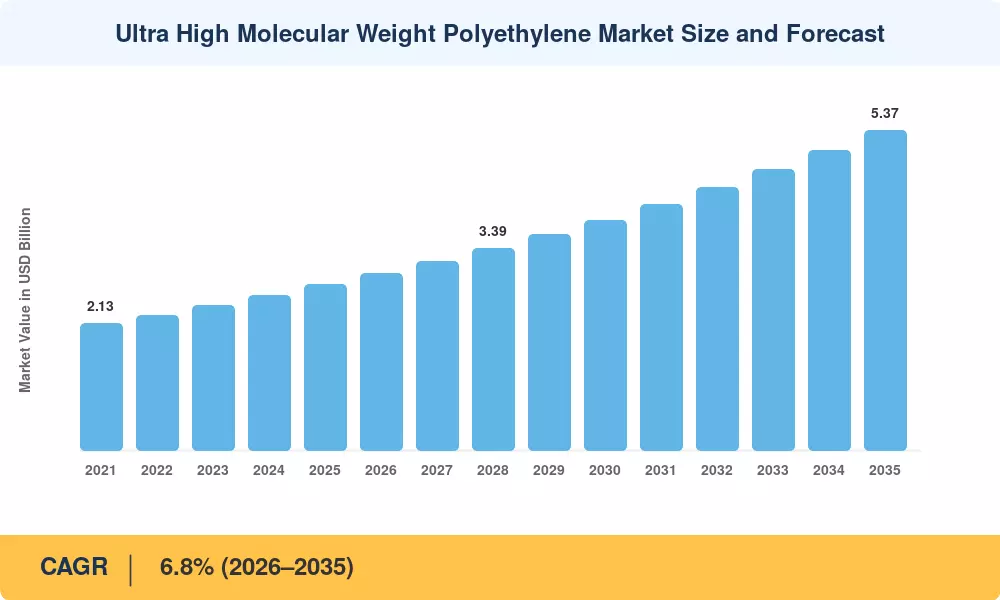

The Ultra High Molecular Weight Polyethylene Market reached USD 2.78 billion in 2025 and is projected to grow from USD 2.97 billion in 2026 to USD 5.37 billion by 2035, registering a CAGR of 6.8% during the forecast period (2026–2035). Two forces anchor this trajectory: a global wave of joint replacement surgeries — the American Academy of Orthopedic Surgeons projects over 3.5 million knee replacements annually in the U.S. by 2030 [2] — and tightening industrial safety mandates that favor wear-resistant plastics in mining and bulk-material handling equipment [3].

What was once the domain of conveyor liners and cutting boards has become the cornerstone of improved ballistic protection, prosthetic bearings and lightweight polymer composites for electric-vehicle battery separators. The U.S. Department of Defense budgeted around USD 1.2 billion in FY 2024 for next-generation body armor, with a large portion of it using UHMWPE materials rather than conventional aramid fiber systems [4]. Continued European REACH modifications are pushing processors to develop engineering thermoplastics with lower particle generation, further boosting the adoption of high-performance polyethylene grades.

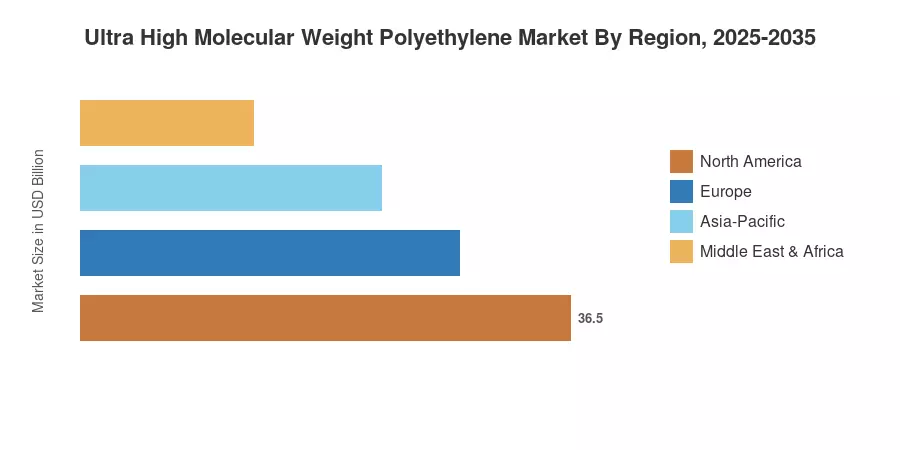

North America has the greatest revenue share of about 32% due to its outsized orthopedic device industry and defense investment. The Asia-Pacific is the fastest-growing area with an estimated CAGR of 8.3%, driven by developing healthcare infrastructure in China and India. Europe is the second largest with around 27% market, where automobile lightweighting and strict occupational safety norms keep the demand buoyant. The Ultra High Molecular Weight Polyethylene Market is ready for structural acceleration as medical, defense and industrial end-users coalesce around a single high-performance resin platform.

Key Report Takeaways

• By Form

- Sheets & panels dominate at roughly 38% of the Ultra High Molecular Weight Polyethylene Market, serving conveyor liners and orthopedic bearing surfaces.

- Fibers represent the fastest-growing form segment with a CAGR of 9.1%, propelled by ballistic protection and cut-resistant apparel demand.

- Rods & profiles account for approximately USD 0.56 billion in 2025, anchored by machined industrial components.

• By Application

- Medical & orthopedic applications hold a 34% value share in the Ultra High Molecular Weight Polyethylene Market, underpinned by growing joint-replacement volumes worldwide.

- Defense & security applications register the highest CAGR at 8.7%, reflecting sustained body armor modernization.

• By Region

- North America leads with USD 0.89 billion in 2025 revenue, anchored by medical-grade polymers demand.

- Asia-Pacific grows fastest at 8.3% CAGR through 2035, with China alone accounting for 42% of regional consumption.

- Europe maintains a 27% global share, driven by automotive and food-processing applications of impact-resistant plastics.

Market Size and Forecast (2021–2035)

Market sizing has been built on a bottom-up basis across four form segments and five end-use sectors, cross-checked using top-down trade data from UN Comtrade, databases of polymer manufacturing capacity, and revenues published by publicly listed makers of UHMWPE materials. Historical figures (2021-2024) are based on actual shipment and import/export data; 2025 is the base-year projection; 2026-2035 values are based on forecast modeling at a 6.8% CAGR.